On July 18, 2019, Internal Revenue Service (IRS) Notice 2019-45 added a range of preventive care benefits for chronic conditions that may be provided by an HSA-qualified high deductible health plan (HDHP) before the statutory minimum deductible is met. These additional services and items are treated as preventive only when prescribed to treat an individual diagnosed with the specified chronic condition, and only when prescribed for the purpose of preventing the exacerbation of the chronic condition or the development of a secondary condition.

Background

IRS Code Section 223 permits eligible individuals to establish and contribute to Health Savings Accounts (HSAs). Among the requirements to qualify as an eligible individual for an HSA is that the individual be covered under an HDHP and have no other disqualifying health coverage. An HDHP is a health plan that satisfies certain requirements with respect to minimum deductibles and maximum out-of-pocket expenses.

Generally, an HDHP may not provide benefits for any year until the minimum deductible for that year is satisfied. However, there is a safe harbor for preventive care that allows certain preventive care procedures and items to be paid prior to meeting the statutory minimum deductible amount for any calendar year.

Previous guidance provided in Notice 2004-23 and Q&As 26 and 27 of Notice 2004-50 gives direction on preventive care benefits allowed to be provided by an HDHP without regard to the minimum deductible requirements. Notice 2018-12 further clarified that benefits for male sterilization or male contraceptives are not considered preventive care.

Preventive Care and Chronic Conditions

On June 24, 2019, President Trump issued Executive Order 13877. Among other issues, the order included a mandate to issue guidance to expand the availability of coverage under HDHPs for low-cost preventive care, paid before the deductible is met, to help maintain the health status for individuals with chronic conditions.

In prior guidance the Treasury Department and the IRS stated that preventive care generally does not include any service or benefit intended to treat an existing illness, injury, or condition. However, cost barriers for some individuals with certain chronic conditions exist for those who cannot afford necessary care to prevent exacerbation of the chronic condition.

The Treasury Department and the IRS, in consultation with the Department of Health and Human Services, have determined that certain medical care services and products, including prescription drugs, should be classified as preventive care for those with certain chronic conditions.

As documented in the Notice, each medical service or item, when prescribed for an individual with the related chronic condition, evidences the following characteristics:

- The service or item is low-cost;

- There is medical evidence supporting high cost efficiency (a large expected impact) of preventing exacerbation of the chronic condition or the development of a secondary condition; and,

- There is a strong likelihood, documented by clinical evidence, that with respect to the class of individuals prescribed the item or service, the specific service or use of the item will prevent the exacerbation of the chronic condition or the development of a secondary condition that requires significantly higher cost treatments.

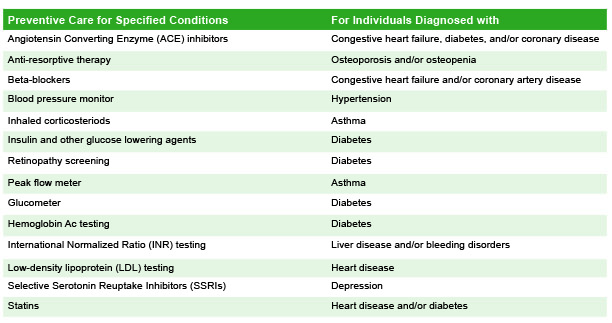

Medical services and items that can be covered by the health plan before the deductible is satisfied are limited to the specific medical care services or items listed in the chart below. These specified services and items are treated as preventive care only when prescribed to treat an individual diagnosed with the associated chronic condition and only when prescribed for the purpose of preventing the exacerbation of the chronic condition.

In other words, first confirm the diagnosis in the right-hand column and then ensure that the prescription or item purchased is specified in the left-hand column. For instance, a diagnosis of hypertension would not warrant an ACE inhibitor to be covered before the deductible is met, although a doctor may prescribe it for hypertension.

This is a significant step forward for the industry and those with chronic conditions.