The 2022 Milliman Long Term Care Insurance Survey is the 24th consecutive annual review of stand-alone long-term care insurance (LTCI) published by Broker World magazine. It analyzes the marketplace, reports sales distributions, and describes available products.

More discussion of worksite sales, including a comparison of worksite sales distributions vs. non-worksite sales distributions will be in Broker World magazine’s August issue.

Unless otherwise indicated, references are solely to U.S. stand-alone LTCI sales, excluding exercised future purchase options (FPOs) or other changes to existing coverage. “Stand-alone” refers to LTCI policies that do not include death benefits (other than returning premiums upon death or waiving a surviving spouse’s premiums) or annuity or disability income benefits. Where referenced, “combo” products provide LTCI combined with life insurance or annuity coverage. “Linked benefit” policies are combo policies which can allow more than the death benefit or annuity account value to be used as LTCI.

All references to sales in terms of “premium” refer to “annualized” premium (1 x annual; 2 x semi-annual; 4 x quarterly; 12 x monthly), even if only one monthly premium was received before year-end. All references to “Washington” or “WA” refer to the state of Washington. “WCF” refers to the “WA Cares Fund,” explained in the Market Perspective section.

Highlights from this year’s survey

Participants

Seven insurers (Bankers Life, Knights of Columbus, Mutual of Omaha, National Guardian Life, New York Life, Northwestern, and Thrivent) contributed broadly to the stand-alone sales distributions reported herein. Total industry sales include, for seven additional companies, either reported sales (without sales distribution data) or the authors’ estimates of sales.

Our statistical distributions reflect non-worksite LTCI sales well. However, our worksite sales distributions do not reflect low-price worksite programs. Carriers that provided 2021 distributions had an average worksite annual premium of $2,077, whereas the insurers that provided sales, but not distributions, had an average worksite premium of $674 annually.

Auto-Owners, MassMutual and Transamerica all stopped selling stand-alone LTCI in 2021.

The following ten insurers contributed to our combination sales data: AFLAC, John Hancock, Mass Mutual, New York Life, Nationwide, Northwestern Mutual (Northwestern), OneAmerica, Pacific Life, Securian, and Trustmark.

Sales Summary

- We estimate total stand-alone LTCI annualized new premium sales of nearly $200 million1 in 2021 (including exercised FPOs, except FPOs for insurers no longer selling LTCI), almost 1/3 more than our 2020 estimate of $150 million.1 However, premium outside the state of Washington decreased 6.0 percent, based on the insurers that reported sales.

- We estimate that 140,000 to 150,000 people purchased stand-alone LTCI coverage in 2021, more than triple the 2020 numbers. Outside of WA, the number of new insureds dropped 9.4 percent based on the insurers that reported sales.

- Worksite sales soared. We estimate that new annualized premium from worksite sales tripled in 2021, while non-work-site premium increased by 6.0 percent. We estimate that there were about 9.3 times as many worksite sales in 2021 compared to 2020, while non-worksite sales increased 47 percent.

- Insurers providing sales information to this survey reported approximately $155 million1 in 2021 annualized new premium sales (including exercised FPOs) and 75,162 new policies, 25 percent more premium and 2.18 times more policies than the same insurers sold in 2020. The balance of the new premium sales in the previous bullets reflects our estimates for insurers not providing sales information.

- For the first time ever in our survey, more males purchased LTCI than females, which appears to have been driven by the WCF exemption.

- As noted in the Market Perspective section, the number of policies sold combining life insurance with LTCI or Chronic Illness benefits soared. Premium increased significantly as well, but because WA sales had a young average age and a small average face amount, the second half of 2021 average size combination life premium was only about one-quarter of the corresponding 2020 average premium.

- Among carriers currently issuing LTCI, Northwestern had a large lead in annualized new premium including FPO elections, selling slightly more than the #2 and #3 insurers combined (Mutual of Omaha and New York Life, respectively). However, similar to last year’s survey, Mutual of Omaha led Northwestern in annualized premium from new policies sold.

Reflecting nine companies’ data, the inforce number of cases increased for the first time since 2014, by 3.6 percent, because of WA sales. Annualized premium rose 6.7 percent. Inforce premium rises due to sales, price increases, and benefit increases (including FPOs), and falls from lapses, reductions in coverage, deaths, and shifts to paid-up status.

Collectively, seven participants paid about one percent less in claims in 2021 than in 2020, despite having about 15 percent more claimants.

Overall, the stand-alone LTCI industry incurred $12.9 billion in claims in 2020 (essentially the same as 2019) based on companies’ statutory annual filings, raising total incurred claims from 1991 through 2020 to $167.3 billion. (Note: 2020 was the most recent year available from statutory filings when this article was written.) Most of these claims were incurred by insurers that no longer sell LTCI.

About the Survey

This article is arranged in the following sections:

- Highlights provides a high-level view of results.

- Market Perspective provides insights into the LTCI market.

- Claims presents industry-level claims data.

- Sales Statistical Analysis presents industry-level sales distributions reflecting data from 8 insurers.

- Partnership Programs discusses the impact of the state partnerships for LTCI.

Available only online:

- Product Exhibit shows, for 6 insurers: financial ratings, LTCI sales and inforce business, and product details.

- Product Exhibit Details, a row-by-row definition of the product exhibit entries, with some commentary.

- Premium Exhibit shows lifetime annual premiums for each insurer’s most common underwriting class, for issue ages 40, 50, 60, and 70 for single females, single males, and female/male couples (assuming both buy at the same age), based on $100 per day (or closest equivalent weekly or monthly) benefit, 90-day facility and most common home care elimination period, three-year and five-year benefit periods or $100,000 and $200,000 maximum lifetime buckets, with and without Shared Care and with flat benefits or automatic three or five percent annual compound benefit increases for life. Worksite premiums do not reflect any worksite-specific discount, though some carriers offer this.

- Premium Adjustments (from our Premium Exhibit prices) by underwriting class for each participant.

- Distribution by underwriting class for each participant. Depending upon the product shown for an insurer in the Product Exhibit, we sometimes adjust that insurer’s underwriting distribution to provide readers a better expectation of likely results if they submit an application in the coming year and to line up with the prices we display. For example, if the Product Exhibit shows only a new product which has only one underwriting class (hence one price), but the insurer’s data partly or solely reflect an older product with three underwriting classifications, we might choose to show “100 percent” in their best (only) underwriting class.

- State-by-state results show the percentage of sales by state, average premium by state and percentage of policies qualifying for Partnership by state.

MARKET PERSPECTIVE (more detail in subsequent parts of the article)

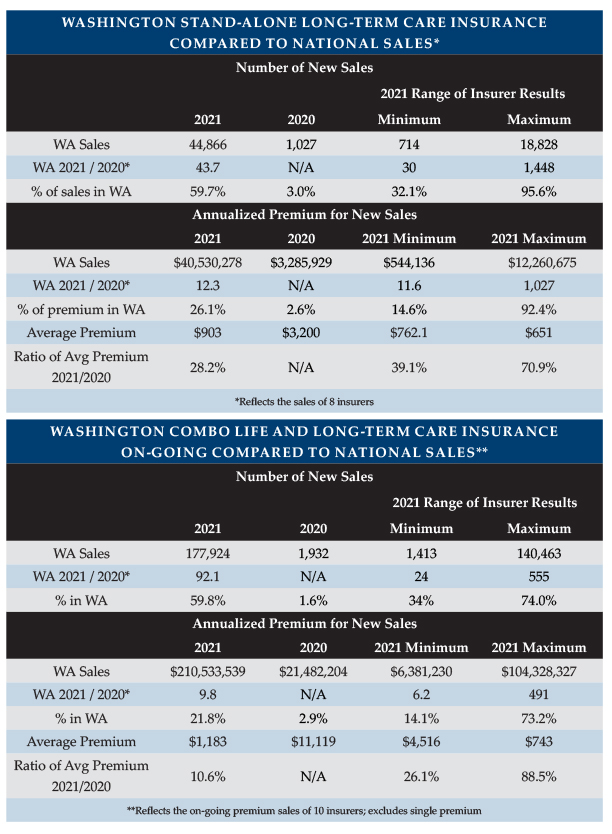

Washington State’s “Washington Cares Fund” (WCF) stimulated a tremendous demand for private LTCI from individuals and businesses within WA. WCF imposes a 0.58 percent payroll tax to fund a $36,500 lifetime pool (intended to inflate according to the Washington consumer price index) for care received in WA as defined in the Revised Code of Washington 50B.04. However, people who purchased qualifying private stand-alone or combination LTCI by November 1, 2021 could file to be exempt from the tax. Partly because the tax applies to all earned income, LTCI sales in Washington soared to unprecedented levels. Insurers quickly became backlogged with applications and were concerned about early lapses as the law provided a permanent WCF exemption based on only a one-time attestation. Insurers reduced design flexibility, and then discontinued sales in WA before the November 1 deadline. Nonetheless, as shown in the WA table, WA accounted for 60 percent of reported stand-alone LTCI policies sold and 60 percent of combination life/LTCI on-going premium (i.e., excluding single premium) policies sold in 2021 after having accounted for 3.0 percent of stand-alone LTCI sales in 2020 and only 1.6 percent of combination life/LTCI sales in 2020. Including estimated sales, we think more than 70 percent of the stand-alone policies sold in 2021 were sold in WA. (Note: WA had received 470,000 applications for exemption as of March 2022.)

As shown in the WA Table, insurers reported 44 times as many stand-alone policies sold in WA in 2021 as in 2020 but only 12 times as much new annualized premium. The WA table also shows the highest and lowest insurer results for the statistics in this and following bullets. Outside WA, insurers reported 6.0 percent less premium and 9.4 percent fewer policies in 2021 than in 2020. As mentioned earlier, our participants sold 2.18 times as many policies but only 25 percent more premium in 2021 than the same insurers sold in 2020. Total industry growth was higher than participant growth because the worksite market is substantially under-represented in the sales reported in the survey.

As shown in the WA Table, insurers reported 92 times as many combination on-going premium policies sold in WA in 2021 as in 2020 but only 9.8 times as much new annualized premium. Outside WA, insurers reported 0.6 percent more policies and 18 percent more premium in 2021 than in 2020. As a result, our national data for such combination policies shows 2.5 times as many new policies and 1.4 times as much annualized new premium. We collected single premium information as well, but we are reporting only the on-going premium results as WA sales had a much smaller impact in the single premium market.

As reflected in the table, reported data suggested that combination policies grew much faster in WA than stand-alone LTCI. However, including our estimates, the stand-alone sales grew a little more than the reported combination sales, and full-market combination sales may have grown less than 92 times as our data may reflect a higher percentage of the worksite combination market than of the individual combination market.

The bottom row in the combination portion of the table reflects a statistical “anomaly.” Combining data for the 10 combination insurers, the 2021 average premium was 10.6 percent of the 2020 average premium. However, the insurer with the minimum ratio had a 2021 average premium equal to 26.1 percent of its 2020 average premium. That is, the overall ratio was 10.6 percent but no insurer had a ratio less than 26.1 percent. That happened because the distribution of the business among insurers shifted significantly between 2020 and 2021. The company with the 88.5 percent ratio had low average premiums in both 2020 and 2021 and had a much bigger market share in 2021, driving down the average premium. If that company is removed from the data, the combined ratio of 2021 average size to 2020 average size would increase from 10.6 to 22.4 percent which would fall within the range of the minimum (26.1 percent) and the revised maximum (48.5 percent).

LIMRA’s U.S. Life Combination Products Sale Survey, 2020 (above we cited 2021 results) saw seven percent fewer policies and 23 percent less annualized new premium combined across whole life, universal life, variable universal life and term, with variable life performing the best (four percent more policies than in 2019 but two percent less new premium). The stand-alone LTCI industry performed better during that time period, as we estimated last year, with 13 percent less premium than in 2019.

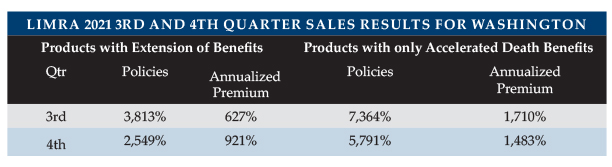

However, LIMRA reports that the combination market rebounded in the first six months of 2021, enjoying 10 percent growth in policies and nine percent growth in premium, before significant increases driven largely by the WCF exemption. Based on 17 insurers’ contributions, LIMRA reports the following quarterly nationwide gains in 2021 over 2020. Note that a growth of 3,813 percent means that 39.13 times as many policies were sold. It is hard to compare LIMRA data to our survey data. LIMRA had more contributors than we did and a different representation of the individual market vs. worksite. We reported year-over-year results compared to LIMRA’s quarterly results below. Our data seems to show more growth but lower average premium, probably due to different data contributors and our inclusion of more worksite business in the estimates.

WA sales distorted the characteristics of sales significantly, as will be explained throughout this report. Given the observed sales in WA, it appears likely consumers generally sought the least expensive way to opt out of WCF.

The national placement rate increased from 57.8 percent in 2020 to 61.7 percent in 2021 (as shown in Table 24), driven by WA sales. WA had a 72.7 percent placement rate, which appears to be influenced by healthy and young applicants. Outside WA, the placement rate was 54.1 percent. Only 13.3 percent of WA business was declined (27.4 percent elsewhere) and declines were lower in WA for all age bands. Only 14.1 percent of WA business was incomplete, suspended, not taken out or returned during the free look period (18.5 percent elsewhere). Our surveys have never found placement rates parallel to 2021 WA experience. (Note: One survey participant sold a short-term care policy that they stated qualified for WCF exemption. Had we included it in this paragraph’s statistics, the WA placement ratio would have been even higher)

Higher placement ratios are critical to encourage more financial advisors to mention LTCI to clients. The following opportunities can improve placement rates.

- E-applications speed submission and reduce processing time, thus generally increasing placement.

- Health pre-qualification effectively and efficiently decreases decline rates.

- Education of distributors, such as drill-down questions in on-line underwriting guides, tends to improves placement.

- Requiring cash with the application (CWA) led to about five percent more of the apps being placed according to our 2019 survey.

- Improved messaging regarding the value of LTCI and of buying now (rather than in the future) typically improves the placement rate by attracting younger and healthier applicants.

Future private LTCI sales in WA will be watched closely to determine the impact of WCF. For example:

- Will WCF cause consumers to become more attentive to their potential LTC needs?

- Will consumers feel a need to supplement WCF coverage? If so, what products and designs will consumers favor to supplement WCF?

- Will WCF messaging promote private LTCI purchases?

- How will explaining WCF and its differences from private LTCI (such as different claim triggers, lack of portability outside WA, and/or lack of Partnership qualification) impact the sales process and attitudes regarding selling and buying LTCI?

- Will the insurance industry develop new products to fit a market with WCF coverage?

- Will the rush of 2021 private LTCI sales dry up future demand for private LTCI in WA?

- Will future legislation modify WCF? If so, how will that impact private LTCI sales?

- Will consumer, insurance agent, and/or insurer attitudes be affected by the possible perception that WCF benefits will be made more generous in the future?

Other states are considering state-run LTCI programs. For example, California has completed an initial feasibility study and established a task force to explore the possibility of a state LTCI program.

- Will insurers be interested in complementing state programs if those programs vary by jurisdiction?

- Will brokers consider such complexity worth their effort?

- Will employers and employee benefit advisors consider LTCI programs if they must vary by employee resident state?

- What will happen to individuals who move from one state to another?

- Will inconsistencies increase pressure for a uniform national program?

- Will consumers, employers, brokers and insurers sit on the sidelines in what they might view as a turbulent short-term market?

- How might reactions parallel or contrast with reactions to the original Robert Woods Johnson Partnerships and the partnership provisions of the Deficit Reduction Act of 2005?

The COVID-19 (COVID) pandemic may have driven increased consumer interest in life insurance. LIMRA reported a five percent increase in life insurance policies sold in 2021 over 2020 with a 20 percent increase in annualized premium and projects a 10 percent premium increase for whole life policies in 2022, with an additional increase in 2023.2 Thirty percent of survey responders say they are more likely to buy life insurance as a result of the pandemic2.

Above, we reported much larger increases because we focused on LTC-related policies, whereas these results include life insurance policies that lack LTC-related features.

Last year, we published (in a separate article in the June issue of Broker World) our survey participants’ reaction to the pandemic. This year, we asked for updated responses.

Insurers still do not anticipate any change in LTCI pricing due to the pandemic. It remains to be seen whether having had COVID will impact the future incidence, length, or severity of LTCI claims.

Insurers also do not anticipate permanent changes to procedures due to the COVID pandemic. Some insurers temporarily liberalized claims adjudication (e.g., waiving face-to-face assessments, broadening alternative plan of care) and underwriting (e.g., waiving face-to-face assessments, less insistence on current medical records) but anticipate restoration of previous protocols.

Having had COVID without being hospitalized generally seems to require a 30-to-60 day wait after full recovery before an application will be considered. With hospitalization, a 180-day wait is typically imposed from the date of recovery. Having been in contact with someone who had COVID or having travelled abroad is generally a non-issue, although one insurer mentioned a 14-day wait for contact (without having to supply a new application) and one insurer mentioned a 30-day wait for having traveled abroad.

The FPO (future purchase option, a guaranteed, or a non-guaranteed board-approved, option, under specified conditions, to purchase additional coverage without demonstrating good health) election rate dipped from 81.8 to 78.2 percent in 2021. As both the additional coverage and unit price increase for FPOs as policies age, FPOs become increasingly expensive, even more so with inforce price increases. The high election rate may reflect the importance of LTCI to policyholders and the effectiveness of annual (as opposed to triennial) negative-election FPOs. Negative-election FPOs activate automatically unless the client rejects them. Positive-election FPOs activate only if the client initiates a timely request. Considering such FPOs and other increased coverage provisions, we project a maximum benefit at age 80 of $292/day for an average 51-year-old purchaser in 2021, which is equivalent to an average 2.7 percent compounded benefit increase between 2021 and 2050. In 2020, the average 58-year-old purchaser anticipated an age 80 benefit (in 2042) of $305. So, the average 2021 purchaser will have four percent less coverage, despite facing eight more years of inflation in the cost of care. WA sales’ lower initial monthly maximum benefit and less robust compounding contributed to this reduction in estimated coverage. This is the lowest effective rate of compounding that we’ve seen in the survey, yet inflation appears to be an increasing threat now. As noted in the initial monthly maximum and benefit increase feature discussions below, 2021 WA sales might be more exposed to voluntary reductions, which could drop future coverage from 2021 sales even lower. Purchasers may be disappointed if the purchasing power of their LTCI policies deteriorates over time.

Current premiums are much more stable than past premiums, partly because today’s premiums reflect much more conservative assumptions based on far more credible data3 and lower assumed investment yields. Three participants have never increased premiums on policies issued under “rate stabilization” laws, one of whom has had no increases on policies issued since 2003. Four other participating insurance companies have not raised rates on policies issued since 2015 (going back to 2013 for a couple of them). A financial advisor who is not aware of the price stability of new policies may be reluctant to encourage clients to consider LTCI.

Stand-alone LTCI without a return of premium feature can be sold for a lower premium than a linked-benefit product that adds a death benefit. However, that price advantage of stand-alone LTCI has reduced for partnered individuals. Not long ago, partnered people buying alone typically got a 15 percent discount compared to the single-person price of stand-alone LTCI, which was a bigger percentage discount than the typical linked-benefit product savings for partnered individuals. Now, partnered people buying alone typically get only a five percent discount with stand-alone LTCI, which is lower than the typical linked-benefit savings. Both-buy couples’ discounts typically provide more of an advantage for stand-alone LTCI as the linked-benefit price saving for married people is often the same whether or not the spouse purchases. However, that advantage has also reduced because both-buy discounts for stand-alone LTCI have dropped.

Linked benefit products tend to be attractive to consumers because if the insured never has a LTC claim, their beneficiary will receive a death benefit and because they often have guaranteed premiums and benefits. As noted above, stand-alone LTCI’s price advantage for couples has reduced. Furthermore, in an increasing interest rate environment, products with the ability to reflect higher non-guaranteed interest rates are likely to have a cost advantage.

However, it is important to remember that typical stand-alone and linked-benefit products provide much more significant LTC protection than combination policies which provide LTCI only through an accelerated death benefit.

- Accelerated Death Benefit (ADB) provisions do not increase over time. By the time claim payments are made, stand-alone and linked-benefit policies’ maximum monthly benefit (on policies with benefit increase features) will have risen significantly.

- Stand-alone and linked-benefit policies have lower renewal termination rates than policies with ADB. Thus, they are much more likely to pay LTCI benefits.

- Because stand-alone policies are usually “use-it-or-lose it,” stand-alone policies might be more likely to be used to pay for care, whereas policies with ADB features might be held for the death benefit. On the other hand, ADB features are more likely to be cash benefits and fully paid.

Four participants offer coverage in all U.S. jurisdictions, but only two participants issued in all 50 states plus the District of Columbia. Insurers are reluctant to sell in jurisdictions which have unfavorable legislation or regulations, restrict rate increases, or are slow to approve new products. Lack of product availability in a jurisdiction can complicate or thwart a worksite case.

Life insurers generally have a retention limit (i.e., how much risk they’ll retain for a particular individual), an issue limit (i.e., their retention limit plus the amount of reinsurance they have arranged) and a participation limit. Even if an application requests coverage below their issue limit, insurers don’t typically issue coverage that causes a client’s total coverage to exceed their participation limit. Insurers are concerned when total coverage exceeds the apparent need for insurance.

A large death claim hits earnings soon after the insurer learns about the death. In contrast, a LTCI claim is often large because it lasts a long time. In the year of death, a typical LTCI claim reserve is established, so there is not a sudden “hit” to earnings. Over time, the claim reserve may turn out to be insufficient, which can result in spreading the impact of the large claim over multiple years. Thus, LTCI carriers may be less concerned about the impact of a single claim on current earnings. However, LTCI carriers have strong reasons to be concerned about over-insurance, especially if clients can profit from being on claim. So, we queried about participation limits this year and got seven responses.

Three insurers lower their LTCI issue limit to offset other inforce or applied-for stand-alone LTCI, considering current coverage not future increases. Two of those insurers adjust for LTCI that is issued as part of a combination product and one of them lowers its issue limit if other coverage including Chronic Illness riders exceeds $50,000/month or $2,000,000/lifetime. The other four respondents have no participation limit.

CLAIMS

Independent Third-Party Review (IR) is intended to help assure that LTCI claims are paid appropriately.

Since 2009 (in some jurisdictions), if an insurer concludes that a claimant is not chronically ill as defined in the LTCI policy, the insurer must inform the claimant of his/her right to appeal to IR, which is binding on insurers. As shown in our Product Exhibit, most participants have extended IR beyond statutory requirements, most commonly to policies issued prior to the effective date of IR.

In some states, regulators have not set up the required panel of independent reviewer organizations (IROs), and there has been no consumer pressure for those states to do so, which may suggest that insurers are doing a good job.

Indeed, of seven insurers which provided claims information this year, three have never had a request for IR and a fourth does not seem to track IR.

We are not aware of regulators who track IR results, but Steve LaPierre, President of LTCI Independent Eligibility Review Specialists, LLC (LTCIIERS), the largest IR organization, reports a moderate volume of IRs in 2021, with fewer than three percent of insurer denials being partially or fully reversed. LTCIIERS’ data, which include information from insurers that no longer sell LTCI and insurers that offer IR even in the absence of an implemented state IR requirement, appears to demonstrate that insurers are not inappropriately denying claims.

Seven participants reported 2021 claims. As some companies are not able to provide detailed data, some statistics are more robust than others.

Those seven insurers’ combined claim payments were about one percent lower in 2021 than in 2020. However, insurers reported 15 percent more claimants, so the average number of dollars paid per claimant in 2021 dropped about 16 percent from the previous year. This drop could reflect:

- A shift from facility claims to less expensive home care claims (or family care), perhaps triggered by the pandemic.

- An unusually high number of claim terminations, possibly due to the pandemic.

- An unusual distribution of new claims weighted toward the end of the year and/or terminated claims weighted more toward the beginning of the year, either of which would cause fewer claim payments to be made on average in a particular year.

The LTCI industry has paid out benefits to policyholders far greater than indicated in the results of our survey, because many claims are paid by insurers that do not currently sell LTCI or did not submit claims data to us.

LTCI claims paid by insurers no longer selling LTCI may differ significantly from the following statistics as their claimants are more likely to have facility-only coverage, be older, and/or have other different policy or demographic characteristics.

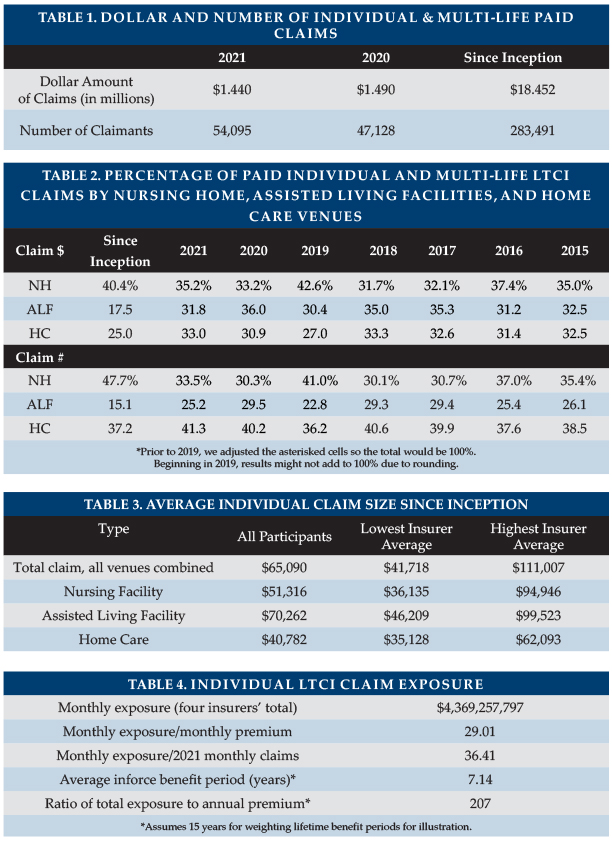

Table 1 shows the total dollar and number of reported individual and multi-life (not group) LTCI claims. It reflects the same carriers for both years. As noted above, total paid claims were down one percent, although the number of claimants rose 15 percent.

The pandemic likely contributed to the lower average 2021 expenditure per claim by reducing the number of facility claims. A reduced payout per claim could also result from new claims being more weighted toward the end of the year or claim terminations being more weighted toward the beginning of the year.

As mentioned above, Table 2 shows that, for insurers reporting claims data, claims shifted away from assisted living facilities (ALFs) and to a lesser degree away from home care, dramatically so on an inception-to-date basis. Different insurers contributing data from one year to another and/or contributing differently makes it harder to identify trends. The Table 2 dollars of claims data include one additional company this year. Another insurer previously assigned all of a claimant’s benefits based on the venue in the claimant’s first month of claim. This year, they reported based on the venue for each claim payment, pushing Table 2 toward nursing homes. “Since inception” means since the insurer first started selling LTCI or as far back as they can report these results (for example, they may have changed claims administration systems and not be able to go all the way back to inception easily).

In the distribution based on number of claims, a person who received care in more than one venue is counted once for each venue, but not double-counted in the total line.

Four carriers reported open individual claims at year-end ranging between 53 percent and 81 percent of the number of claims paid during the year, averaging 70 percent overall.

Table 3 shows average size individual claims since inception: that is, including older claims and reflecting all years of payment. Assisted Living Facility (ALF) claims and Home Care claims showed lower average sizes this year, related to the change in reporting mentioned above. Because 40 percent of claimants since inception have submitted claims from more than one type of venue, the average total claim might be expected to exceed the average claim paid for any particular venue. Individual Assisted Living Facility (ALF) claims stand out as high each year (albeit not as much this year), probably because:

a) ALF claims appear to have a longer duration compared with other venues.

b) Nursing home costs are most likely to exceed the policy daily/monthly maximum, hence nursing home claims are most likely to understate the cost of care.

c) People who maximize the use of their maximum monthly benefits can generally spend as much in an ALF as in a nursing home.

d) Although some surveys report that ALFs cost about half as much as nursing homes on average, ALFs may charge more for a memory unit or for levels of assistance that align more closely with nursing home care.

Several insurers extend ALF coverage to policies which originally did not include ALF coverage, providing policyholders with significant flexibility at the time of claim but contributing to the insurers’ need for rate increases.

The following factors contribute to a large range of average claim by insurer (see Table 3):

- Different markets (by affluence; worksite vs. individual; geography; etc.)

- Demographic differences (distribution by gender and age)

- Distribution by benefit period, benefit increase feature, shared care, and elimination period. For example, one carrier has a higher average home care claim than its average facility claims because home care was a rider and people who added the home care rider were more likely to add compound inflation also.

- Distribution by facility-only policies vs. 50 percent home care vs. 100 percent home care vs. home care only.

- Different lengths of time in the business.

- Differences in the ways insurers report claims.

The following factors cause our average claim sizes to be understated.

- For insurers reporting claims this year, 16.0 percent of inception-to-date individual claims are still open. Our data does not include reserve estimates for future payments on open claims.

- People who recover, then claim again, are counted as multiple insureds, rather than adding their various claims together.

Besides being understated, average claim data does not reflect the value of LTCI benefits from some purchasers’ perspectives, because the many small claims drive down the average claim. LTCI provides significant financial yield for most people who need care one year or longer. A primary purpose of insurance is to protect against adverse results, so the amount of protection, as well as average claim, is important.

Four insurers provided their current individual (excludes group) monthly LTCI claim exposure, which increased by nine percent in 2021 (note: reflects only initial monthly maximum for one insurer). As shown in Table 4, this figure is 29 times their corresponding monthly LTCI premium income and 37 times their 2021 LTCI monthly paid claims. Seven insurers contributed data regarding their inforce distribution by benefit period. Treating endless (lifetime benefit periods) as a 15-year benefit period, we found that their average inforce benefit period is 7.14 years. Changing the assigned value of the endless benefit period by one year has an impact of approximately 0.27 years on the average inforce benefit period. With annual exposure 29 times annual premium and assuming an average benefit period of 7.14 years, we estimate that total exposure is 206 times annual premium.

Four insurers reported their current average individual maximum monthly maximum benefit for claimants, with results ranging from $5,928 to $7,982.

Nursing home (NH) claims are more likely to use the policy’s maximum daily/monthly benefit than ALF claims because ALF daily/monthly costs are generally lower and because policies sometimes have lower maximums for ALFs. ALF claims correspondingly are more likely to use the policy maximum than are adult day care and home care claims.

SALES STATISTICAL ANALYSIS

Bankers Life, Knights of Columbus, Mutual of Omaha, National Guardian, New York Life, Northwestern and Thrivent contributed significant background statistical data, but some were unable to contribute some data.

Sales characteristics vary significantly among insurers based on market differences (individual vs. worksite, affluence, gender distribution, etc.) and this year, with the concentration of LTCI sales in WA. Year-to-year variations in policy feature distributions may reflect industry trends but may also reflect changes in participants, participant practices and designs, participant or worksite market shares, etc. and this year, the WCF. The statistical differences between the worksite and non-worksite sales will be reported in the August issue of Broker World.

Market Share

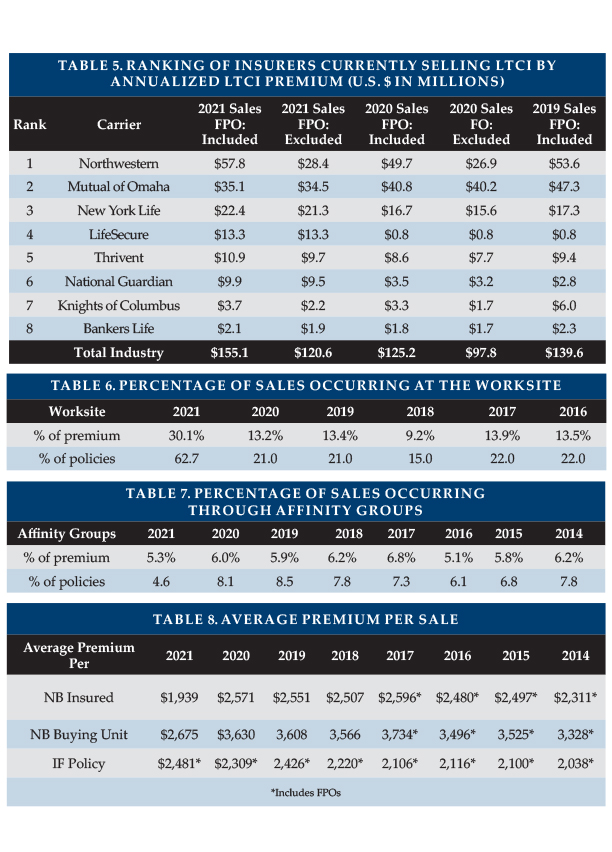

We include purchased increases on existing policies as new premium because new coverage is being issued. Table 5 lists the eight insurers that reported the most 2021 new premium, both including and excluding FPOs. Seven of the eight insurers had increases in annualized premium of 12 percent or more due to WA sales. Northwestern ranks #1 including FPOs and Mutual of Omaha ranks #1 when looking only at new policies, but Northwestern has reduced Mutual of Omaha’s lead. Together, they account for 60 percent of the market, which, when paired with New York Life’s strong growth, resulted in a 74 percent market share for the top three insurers. The premium below includes 100 percent of recurring premiums plus 10 percent of single premiums.

Worksite Market Share

As demonstrated by LifeSecure (see Table 5), worksite sales soared in 2021 due to WA sales. Overall, we estimate that worksite annualized premium tripled in 2021, contributing 30 percent of total new annualized premium. Worksite sales were approximately 9.3 times those recorded in 2020, accounting for more than 60 percent of coverages sold.

Worksite sales normally consist of three different markets as outlined below, the first two of which produce a higher percentage of new insureds than of new premiums. Worksite 2021 sales were largely voluntary but had the age and premium characteristics of core/buy-up due to WA sales.

- Voluntary group coverage generally is less robust than individual coverage.

- Core/Buy-Up programs have particularly young age distributions and modest coverage because a lot of people do not buy-up and are less likely to insure spouses.

- Executive carve-out programs generally provide the most robust coverage. One- or two-couple executive carve-out sales may not qualify for a multi-life discount with some insurers, hence may not be labeled as worksite sales in submissions to our survey.

The amount of worksite sales reported and its distribution among the sub-markets significantly impact sales characteristics. Table 6 is indicative of the full market (including our estimates for insurers that did not report sales), but this year’s sales distributions do not reflect the insurers focusing in the group voluntary and core/buy-up markets. More information about worksite sales will appear in the August issue of Broker World magazine.

As we noted last year, the future of the non-executive carve-out LTCI market is unpredictable with Transamerica’s departure. LifeSecure, Mutual of Omaha, and National Guardian may pick up market share; combination worksite products are likely to pick up market share; and/or worksite LTCI-related sales might drop.

Affinity Market Share

Affinity groups (non-employers such as associations) produced $7.51 million in new annualized premium based on 2,494 new policies (average premium of $3,011) compared to $7.47 million on 2,762 policies (average premium: $2,706). We do not have WA-specific data for affinity coverage, but the decrease in the number of policies suggests that affinity group sales were not influenced much by the WCF exemption given the sales increases observed for other coverage. The higher average premium reflects price increases for new sales. The percentages in Table 7 reflect only participants’ sales.

Characteristics of Policies Sold

Average Premium Per Sale

To determine the average premium for new sales, we exclude FPOs. Due to WA sales, our participants’ average new business (NB) premium per insured and per buying unit (a couple comprise a single buying unit) each plunged 25 percent in 2021, as shown in Table 8.

Participants’ combined average premium per insured outside WA was $3,785, a five percent increase over 2020’s $3,646 because some carriers raised prices in late 2020 and early 2021. (These numbers are slightly overstated because they do include FPOs.)

Three participants had average WA premiums ranging from $522 to $762 per year. On the other hand, one insurer had an average premium of more than $2,000 per year.

Average WA premium ranged, by insurer, from 21 to 80 percent of average premium outside WA. The two insurers for whom the ratio exceeded 36 percent both doubled their minimum size and required three percent compound inflation in WA, which kept their WA premium from dropping as much as for other insurers. One insurer also raised their minimum issue age in WA significantly. At least one other insurer took all three steps, yet still had a much lower average premium in WA than outside WA.

The jurisdiction with the lowest average new premium for participants in 2021 (including FPOs and counting 100 percent of single premiums) was Washington ($1,089), followed by Puerto Rico ($1,349), and Idaho ($2,137). Indiana and Oregon followed with a more typical $2,912 annual premium. The jurisdiction with the highest average premium was Maine ($5,722), followed by Connecticut ($5,174), New Hampshire ($5,039) and Massachusetts ($5,009).

If we include data from, and estimates for, non-participants, the average premium per insured was $2,557 in the non-worksite market, $661 in the worksite market, and $1,371 overall.

Data for 2017 and earlier years included FPOs in these calculations, overstating the average premium per new insured and buying unit.

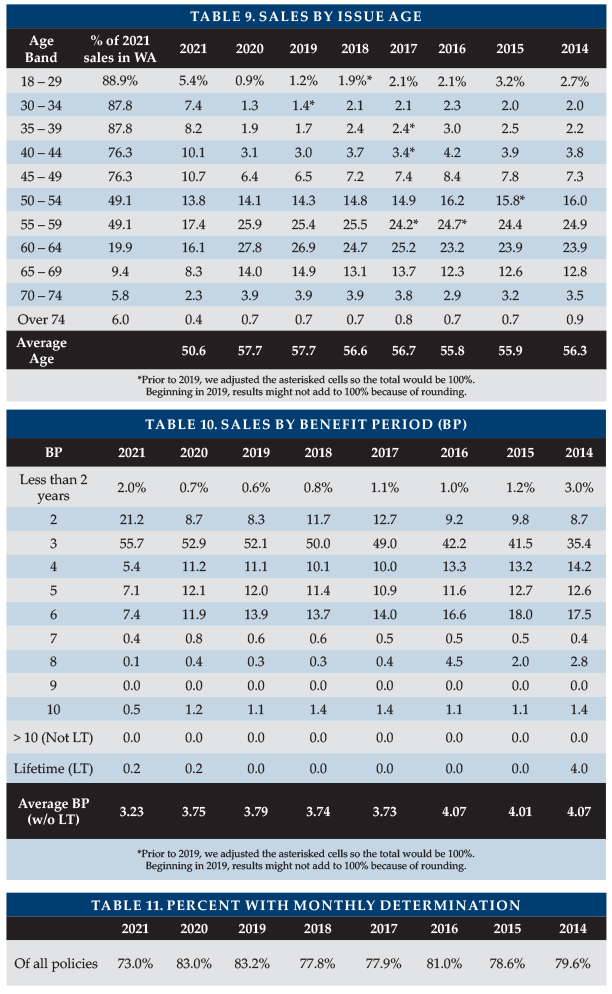

Issue Age

Table 9 shows that WA sales dropped our participants’ average age from 57.7 to 50.6, as 31.1 percent of buyers were below age 45 compared to 7.2 percent in 2020.

The shift to younger ages seems understated because some major worksite carriers did not provide age distribution. Some insurers raised their minimum issue age in WA to 40. That shifted young age business to other insurers and to combination products.

A special column in this table shows the percentage of participants’ placed policies that came from WA, based on age. Not surprisingly, 88.9 percent of the policies for people ages 18-29 came from WA, dropping to 87.8 percent for ages 30-39 and 76.3 percent for ages 40-49. At higher ages, the percentage in WA was much lower, but in each age group it exceeded WA’s 2020 three percent market share.

We estimate that our participants’ average issue age in WA was about 15 years lower than outside WA.

The age distributions for 2016 and earlier had more worksite participants than recent years. Note: one survey participant has a minimum issue age of 40, one will not issue below 30, and one will not issue below 25.

Benefit Period

Table 10 summarizes the distribution of sales by benefit period. The average benefit period for limited benefit period policies dropped more than half a year from 3.75 to 3.23. The reduction in length of coverage is even larger; WA sales were less likely to include Shared Care because there were a lot of single and one-of-a-couple sales and because couples trying to minimize cost were less likely to buy Shared Care. Two-year benefit periods accounted for 21.2 percent of the sales, despite not reflecting the major worksite carriers.

Monthly Benefit

A change in distribution by carrier led to the reduction in policies sold with monthly determination (Table 11). With monthly determination, low-expense days leave more benefits to cover high-expense days. One insurer offers only daily determination; one insurer offers a choice; and the other insurers automatically have monthly (or weekly) determination.

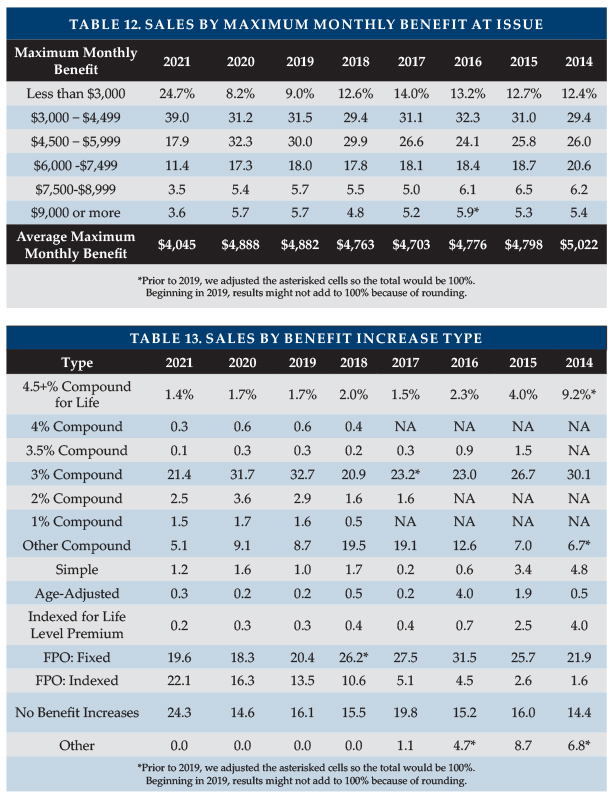

WA sales included a significant number of small policies, causing the average initial maximum monthly benefit to drop to $4,045 (as shown in Table 12), the lowest in the history of our survey despite increasing costs for care. Two insurers accounted for 87.4 percent of the sales that had an initial monthly maximum less than $3,000.

Benefit Increase Features

Table 13 summarizes the distribution of sales by benefit increase feature. WCF permitted policies to qualify for exemption even if there were no benefit increases. This contributed to a rise in the percentage of policies nationwide with no benefit increases, from 14.6 to 24.3 percent. Also, the percentage of FPO sales increased from 34.6 to 41.7 percent, presumably because FPOs do not require first-year premium outlay. Future FPO election rates might drop if a meaningful percentage of these buyers have no intention of exercising such options.

“Indexed Level Premium” policies are priced to have a level premium, but the benefit increase is tied to an index such as the consumer price index (CPI).

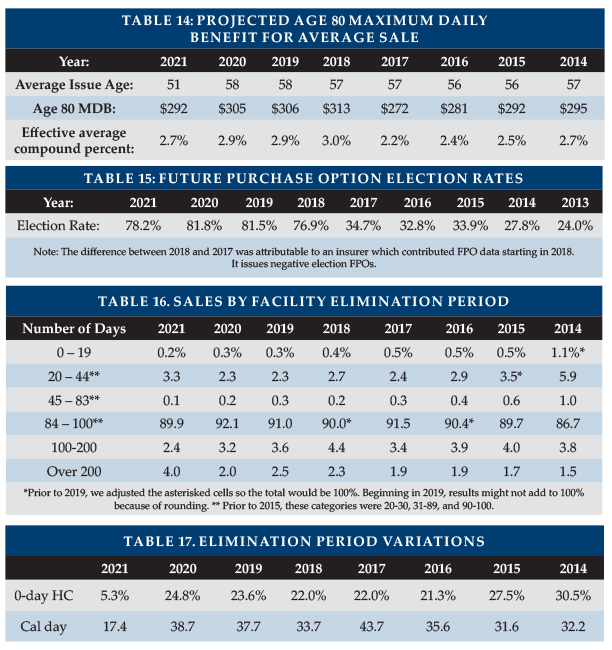

As shown in Table 14, we project the age 80 maximum daily benefit by increasing the average initial daily benefit from the average issue age to age 80, according to the distribution of benefit increase features, using current future purchase option (FPO) election rates and a five percent per year offer for fixed FPOs. The maximum benefit at age 80 (in 2050) for our 2021 average 51-year-old purchaser projects to $292/day (equivalent to 2.7 percent compounding). Had our average buyer bought an average 2020 policy a year ago at age 50, her/his age 80 benefit would be $394/day. The lower initial maximums and reduced benefit increases driven by WA sales caused this drop in coverage. It is even more striking considering that the 2021 buyers are less likely to exercise FPO options and more likely to reduce the monthly maximum or drop the benefit increase feature and that inflation is a growing concern. Pandemic protocols are likely to increase facility costs and there are a variety of inflationary pressures which apply to LTC staff salaries at all types of venue. Most policyholders seem likely to experience eroding purchasing power over time if cost of care trends exceed three percent.

FPOs are important to insureds in order to maintain purchasing power, and 78.2 percent of our participants’ 2021 FPOs were exercised. The high election rate is noteworthy, considering that the cost increases each year due to larger coverage increases each year, increasing unit prices due to age, and additional price increases due to rate increases.

One insurer had an election rate of 88 percent, two insurers had 67 to 68 percent, one insurer had 47 percent, and two insurers had 25 to 29 percent. It seems clear that higher election rates occur if FPOs are more frequent (i.e., every year vs. every three years) and are “negative-election” (i.e., activate automatically unless the client rejects them) as opposed to “positive-election” (i.e., which activate only if the client makes a request). At least some blocks of business demonstrate that policyholders will exercise FPOs if they must do so to continue to receive future offers.

FPOs can also be important to insurers. Two insurers got a large percentage of their new premium (42 percent for one; 51 percent for the other) from FPO elections.

Elimination Period

Table 16 summarizes the distribution of sales by facility elimination period (EP). The percentage of people buying 84-100day EP dropped arithmetically by 2.2 percent, nearly evenly divided between people opting for shorter EPs and those opting for longer EPs. Five insurers saw between 2.75 and six percent of their new buyers opt for roughly six-month EPs and two of those insurers saw between eight and 11 percent of their new buyers opt for one-year EPs. One insurer mentioned that 20 percent of WA purchasers selected a one-year EP.

Table 17 shows the percentage of participant policies with zero-day home care elimination period (but a longer facility elimination period). For insurers offering an additional-cost zero-day home care EP option, the purchase rate is sensitive to the cost. Table 17 shows a shift away from the zero-day home care EP option due to WA sales, as individuals generally sought out lower cost coverage to qualify for the WCF exemption.

Table 17 also shows the percentage of participant policies with a calendar-day EP. It is important to understand that most calendar-day EP provisions do not start counting until a paid-service day has occurred. A significant part of the drop in calendar-day EP is a change in distribution between carriers.

Sales to Couples and Gender Distribution

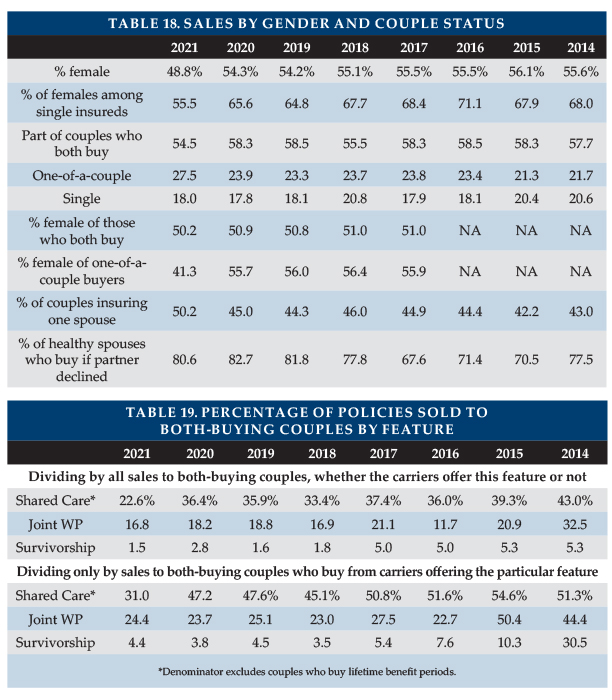

Since inception, the LTCI industry has struggled to attract the attention of male consumers. As shown in Table 18, which summarizes the distribution of sales by gender and single/couple status, a majority of 2021 purchasers (51.4 percent) were male, largely influenced by WA sales. Among single purchasers, the male percentage increased from 34.4 to 44.5 percent.

WA sales also spurred an increase in the percentage of one-of-a-couple sales, from 23.9 to 27.5 percent in 2021. The percentage of one-of-a-couple sales to men increased from 44.3 to 58.7 percent in 2021.

The percentage of accepted applicants who purchase coverage when their partners are declined dropped slightly. It varies significantly by insurer based on their couples pricing and their distribution system. Only two insurers (both large and active in WA) were able to report this data. Their results were almost identical (80.3 and 80.9 percent, respectively) for the percentage of accepted applicants who purchased coverage after a partner’s denial.

Shared Care and Other Couples’ Features

Table 19 summarizes sales of Shared Care and other couples features.

- Shared Care allows one spouse/partner to use the other’s available benefits if their own coverage has been depleted or offers a third independent pool the couple can share.

- Survivorship waives a survivor’s premium after the first death if specified conditions are met.

- Joint waiver of premium (WP) waives both insureds’ premiums if either insured qualifies for benefits.

Changes in distribution by carrier can greatly impact year-to-year comparisons (Table 19), as some insurers embed survivorship or joint waiver automatically (sometimes only for particular circumstances. For example, joint waiver of premium might be automatic if Shared Care is purchased) while others offer it for an extra premium, offer it only under some circumstances, or do not offer the feature.

In the top half of Table 19, percentages are based on the number of policies sold to couples who both buy (only limited benefit, for Shared Care). The bottom half of Table 19 shows the percentage of policies that results from dividing by sales of insurers that offer the outlined feature.

Because WA buyers appeared to minimize their cost (as observed by lower reported average premiums), these features were less popular in 2021. Of couples who both bought limited benefit period, only 22.6 percent added Shared Care, compared to previous percentages of 33.4 to 43.0 percent.

For insurers reporting Shared Care sales, the percentage of both-buying couples who opted for Shared Care varied from four percent to 64 percent. The corresponding percentage of couples with Joint WP varied from four to 100 percent and for Survivorship ranged from 2.7 to 9.0 percent.

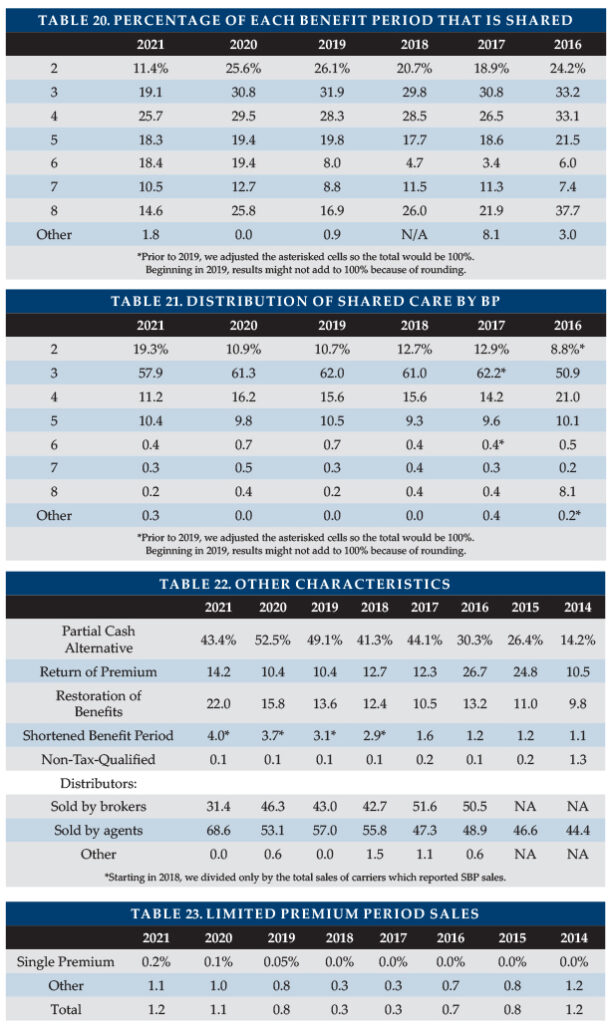

Tables 20 and 21 provide additional breakdown on the characteristics of Shared Care sales. Table 20 shows that couples buying four-year benefit period policies became the most likely to add Shared Care, presumably because people seeking a minimal premium might buy a 3-year benefit period but without Shared Care. Each benefit period can have anywhere from zero to 100 percent Shared Care among its couples.

Table 21 looks only at Shared Care policies and reports their distribution across benefit period, so the percentages must total 100 percent. As many policies have three-year benefit period, more than half the Shared Care policies had a three-year benefit period (Table 21) even though a higher percentage of four-year benefit period policies had Shared Care (Table 20).

Table 19 shows a low percentage of policies having Shared Care, partly because its denominator includes all policies, even those sold to single people or one of a couple. Table 20 denominators are couples who both bought coverage with the particular benefit period. Table 21’s denominator is the number of Shared Care policies.

Shared Care is generally more concentrated in two- to four-year benefit periods than are all sales. Couples are more likely to buy short benefit periods because couples plan to help provide care to each other and Shared Care makes shorter benefit periods more acceptable. Single buyers are more likely to be female and opt for a longer benefit period.

Existence and Type of Home Care Coverage

Three participants reported sales of facility-only policies, which accounted for 0.4 percent of total sales. One insurer was responsible for 85 percent of such sales. Nearly ninety-six percent of the comprehensive policies included home care benefits equal to the facility benefit. The other sales all had a home care benefit of at least 50 percent of the nursing home benefit. The last home-care-only sale in our survey was sold in 2018.

Other Characteristics

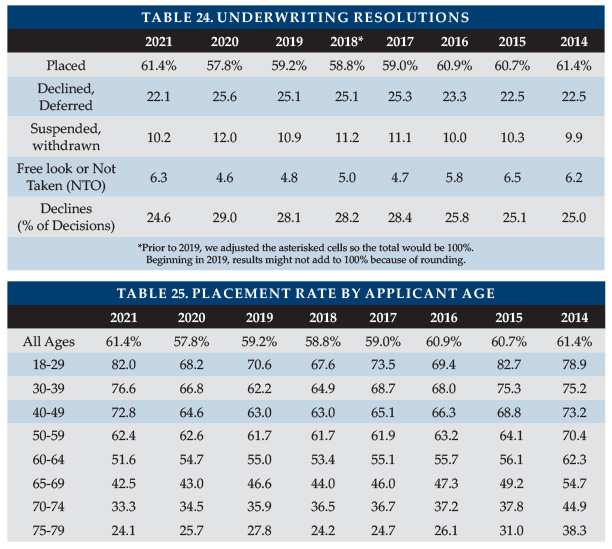

As shown in Table 22, partial cash alternative features (which allowed claimants, in lieu of any other benefit that month, to use between 10 and 40 percent of their benefits for whatever purpose they wish) were included in fewer of our participants’ policies due to a change in market share among participants.

Return of premium (ROP) features were included in 14.2 percent of policies, a surprising increase due to a market share change. ROP returns some or all premiums (usually reduced by paid LTCI benefits) when a policyholder dies. Ninety (90 percent) of ROP features were embedded automatically in the product. Embedded features are designed to raise premiums minimally, typically decreasing the ROP benefit to $0 by age 75.

Due to market share change, 22 percent of policies with limited benefit periods included a restoration of benefits (ROB) provision, which typically restores used benefits when the insured has not needed services for at least six months. Approximately 90 percent of ROB features were automatically embedded.

Insurers must offer shortened benefit period (SBP) coverage, which makes limited future LTCI benefits available to people who stop paying premiums after three or more years. The insurers able to report SBP sales, sold SBP to 4.0 percent of buyers, a small increase due to market share change.

Only one insurer issued non-tax-qualified (NTQ) policies, which accounted for 0.1 percent of total industry sales.

“Captive” (dedicated to one insurer) agents produced 68.6 percent of the sales, their highest percentage since we have been reporting this data. Brokers produced 31.4 percent of the sales. Some direct-to-consumer sales were made but not by our participants. At one time, “captive” agents who sold LTCI tended to specialize in LTCI. Now many are agents of mutual companies.

Sales distribution by jurisdiction is posted on the Broker World website.

Limited Pay and Paid-Up Policies

In 2021, two insurers in the survey sold policies that become paid-up in 10 years or less, accounting for 1.2 percent of sales.

Because today’s premiums are more stable compared to policies sold years ago, premium increases are less likely. One of the key reasons for buying 10-year-pay (avoidance of rate increases after the 10th year) is greatly reduced, while the cost of 10-year-pay has increased, making it less attractive for consumers than in the past. Nonetheless, limited-pay and single-pay policies are attractive to minimize post-retirement outflow and to accommodate §1035 exchanges.

Seven participants reported that 2.9 percent of their inforce policies are paid-up, a lower percentage than last year because an additional insurer participated.

PARTNERSHIP PROGRAM BACKGROUND

When someone applies to Medicaid for long-term care services, most states with Partnership programs disregard assets up to the amount of benefits received from a Partnership-qualified policy (some Indiana and New York policies disregard all assets). Except for California, states with Partnership programs grant reciprocity to Partnership policies issued in other jurisdictions. Partnership programs are approved in 44 jurisdictions, all but AK, DC, HI, MA, MS, UT, and VT, but MA has a similar program (MassHealth).

Four states (CA, CT, IN and NY) blazed the trail for Partnership programs in the early 1990s. Other states were allowed to adopt Partnership regulations (which were simplified and more standardized) as a result of the Deficit Reduction Act of 2005 (DRA).

Approximately 60 percent of Partnership states now allow one percent compounding to qualify for Partnership, which can help low-budget buyers qualify for Partnership and also enables worksite core programs to be Partnership-qualified. A higher percentage of policies would qualify for Partnership in the future if insurers and advisors leverage these opportunities. However, currently only three insurers offer one percent compounding.

Partnership programs could be more successful if:

- Advisors offer small maximum monthly benefits more frequently to middle-income individuals. For example, a $1,500 initial maximum monthly benefit covers about four hours of home care every two days and, with compound benefit increases, may maintain buying power. Many middle-income individuals would like LTCI to help them stay at home while not “burning out” family caregivers and could be motivated further by Partnership asset disregard. (This approach does not work in CA, CT, IN and NY because of their high Partnership minimum daily benefit requirements.)

- Middle-income prospects were better educated about the importance of benefit increases to maintain LTCI purchasing power and qualify for Partnership asset disregard.

- The four original Partnership states migrate to DRA rules.

- More jurisdictions adopt Partnership programs.

- Programs that privately finance direct mail educational LTCI content from public agencies were adopted more broadly.

- Financial advisors were to press reluctant insurers to certify their products and offer one percent compounding.

- More financial advisors were certified. Some people argue that certification requirements should be loosened. At a minimum, the renewal certification process could be improved.

- Linked benefit products became Partnership-qualified.

PARTNERSHIP PROGRAM SALES

Participants reported Partnership sales in 41 states, all authorized states except CA, CT and NY. One carrier sold a Partnership policy in each of the 41 states. One has chosen not to certify Partnership conformance.

Insurance brokers do not have access to Partnership policies in CA, CT and NY and from only one insurer in IN. However, consumers may be able to purchase Partnership-qualified coverage from another entity.

As only 23.4 percent of participants’ WA policies qualified for the Partnership, participants’ Partnership-qualified policies in DRA states dropped from 55 to 34.6 percent. Other states saw some slippage in Partnership sales, presumably because benefit increase provisions are less popular. Minnesota (76.6 percent, down from 81.4 percent in 2020) leads each year. Wisconsin was second (67.5 percent) and six states had between 60 and 64 percent. Indiana (3.7 percent) and New Mexico (8.3 percent) were the only states with participant Partnership sales in which fewer than 20 percent qualified.

UNDERWRITING DATA

Case Disposition

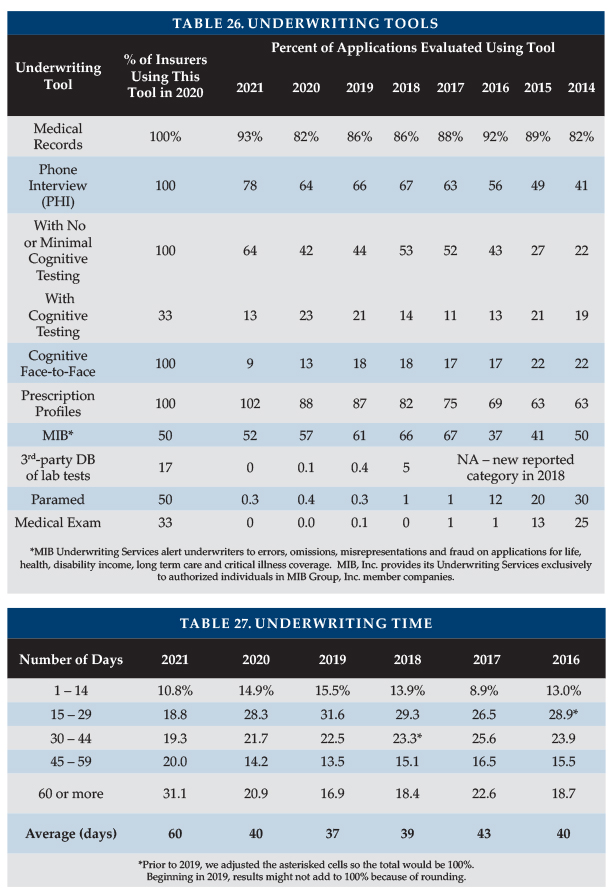

Seven insurers contributed application case disposition data to the survey (Table 24). In 2021, 61.4 percent of applications were placed due to WA sales. In 2020, 57.8 percent were placed. Two insurers placed 71 to 78 percent of their applications and five insurers placed 45 to 60 percent. One insurer had a lower placement rate than in 2020.

Declines were down in 2021, to 24.6 percent from 29.0 percent in 2020. Decline rates varied by insurer, ranging from 12.0 to 35.1 percent (based on decisions).

The percentage of suspended and withdrawn policies dropped but free look and not-taken (NTO) increased about as much. Our participants experienced between 6.6 and 15.6 percent terminated cases for such reasons. In WA, suspended, withdrawn, and NTOs more often resulted from the applicant finding a less expensive solution, sometimes through their employer. Thus, from a consumer standpoint, the placement rate was likely higher than stated above.

Seven insurers contributed to our WA placement data. They had a 72.7 percent placement rate in WA with a 54.1 percent placement rate outside WA. Their decline rate was 13.3 percent in WA vs. 27.4 percent elsewhere. Their combined withdrawn/suspended/NTO rate was 14.1 percent in WA vs. approximately 18.5 percent outside WA.

The WA placement rate was higher primarily for applicants under age 50.

Factors such as age distribution, distribution system, market, underwriting requirements, and underwriting standards affect these results.

Table 25 shows that the placement rate increased at all ages. The improvements under age 50 resulted from WA sales. One insurer sold a product with a short benefit period that qualifies as LTCI in WA. Had we included that product, placement rates would have been higher at older bands represented in the table.

This data is a subset of the placement data in Table 24.

Low placement rates increase insurers’ cost per placed policy. More importantly, low placement rates discourage advisors from discussing LTCI with clients. In addition to not wanting to waste time and effort, advisors may fear that declined clients will be dissatisfied. In the Market Perspective section, we listed ways to improve placement rates. This is a critical issue for the industry. If readers have suggestions, they are invited to contact the authors.

Underwriting Tools

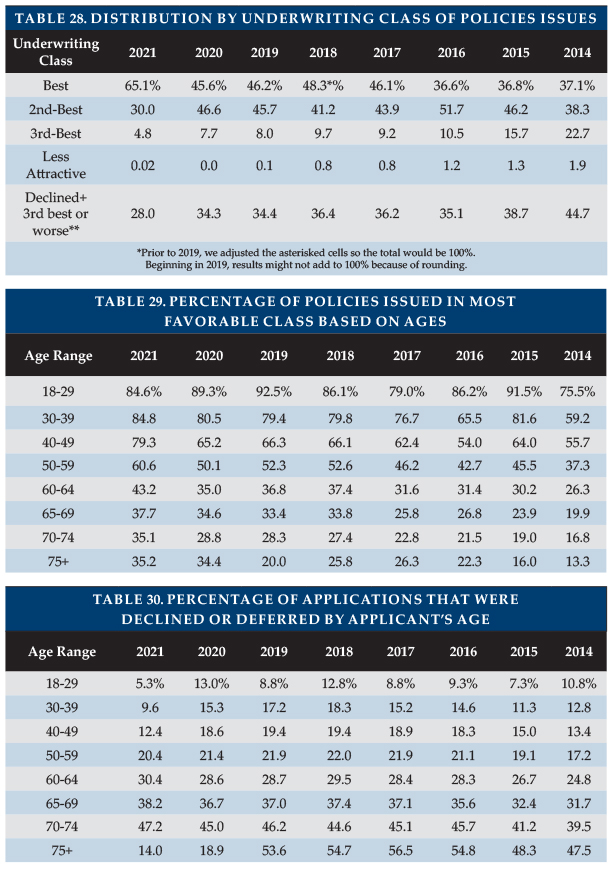

Four insurers contributed data to Table 26, which divides the number of uses of each underwriting tool by the number of applications processed. For example, the count of instances where medical records were requested was 93 percent of the number of applications. That does not mean that 93 percent of the applications involved medical records, because some applications resulted in more than one set of medical records being requested.

Year-to-year changes in distribution of sales among insurers significantly impact results. Lower maximum ages result in fewer face-to-face exams. Insurers might underreport the use of an underwriting tool because they may lack a good source for that statistic. For example, an insurer might not be able to split phone interviews by whether or not they include cognitive testing.

Medical, phone interviews, and prescription profiles all increased, signs of more thorough underwriting. The 2021 changes all reflect the impact of WA sales, with fewer apps needing face-to-face exams or phone interviews with a cognitive test due to the mix of younger applicants.

Underwriting Time

Table 27 shows an average processing time, from receipt of application to mailing the policy, of 60 days. The increase in sales due to the WCF exemption swamped insurers, adding significantly to processing time. The issue appeared to be significantly more severe for some insurers marketing combination products.

Rating Classification

Table 28 shows that almost two-thirds of 2021 policies were issued in the most favorable rating classification due to WA sales.

Table 28 shows the percentage of decisions which were either declined or placed in the 3rd or less-attractive classification is reducing. We conclude that the industry made more favorable decisions rather than declining applicants in lieu of giving them a substandard rating.

Tables 29 and 30 show the 2020 percentages of policies issued in the most favorable category and decline decisions by issue age. Tables 29 and 30 do not exactly match Table 28 because some participants provide all-age rating or decline data. The percentage placed in the most favorable classification increased for all ages, except 18-29.

The overall decline rate reduced because, as explained earlier, WA sales included younger and likely healthier applicants. The lower decline rate was most noticeable under age 50. Above age 60, where increased WA sales had less impact, the decline rate increased (except for a likely statistical fluctuation at ages 75+).

CLOSING

We thank insurance company staff for submitting the data and responding to questions promptly. We also thank Sophia Fosdick, Rachelle Jacobs, and Zane Truesdell of Milliman for managing the data expertly.

We reviewed data for reasonableness and insurers reviewed their product exhibit displays. Nonetheless, we cannot assure that all data is accurate.

If you have suggestions for improving this survey (including new entrants in the market), please contact one of the authors.

Footnotes:

- Single premium sales are counted at 10 percent for the annualized premium calculations herein.

- Elizabeth Festa, “2021 a Banner Year for Life Insurance Sales; Highest Growth Since 1983 Charted”, March 22, 2022, https://www.investopedia.com/2021-a-banner-year-for-life-insurance-sales-5222729.

- Society of Actuaries (November 2016). Long-Term Care Insurance: The SOA Pricing Project. Retrieved May 16, 2020, from https://www.soa.org/globalassets/assets/files/static-pages/sections/long-term-care/ltc-pricing-project.pdf (PDF).