The Internal Revenue Service (IRS) and Social Security Administration have released the cost-of-living (COLA) inflation adjustments that apply to dollar limitations set forth in certain IRS Code Sections. The Consumer Price Index rose and therefore warranted increases in most indexed figures for 2020.

Social Security and Medicare Wage Base

For 2020, the Social Security wage base is $137,700. The Social Security rate of 6.2 percent is applied to wages up to the maximum taxable amount for the year; the Medicare portion of 1.45 percent applies to all wages.

In addition, individuals are liable for a 0.9 percent “Additional Medicare Tax” on all wages exceeding specific threshold amounts.

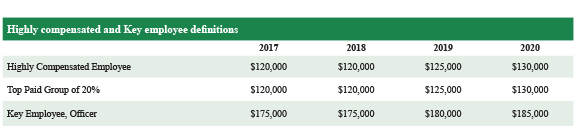

Indexed Compensation Levels

Highly compensated and Key employee definitions.

401(k) Plans

In 2020 the maximum for elective deferrals is $19,500 and the catch-up contribution for those 50 or older is $6,500. That means if you are age 50 or over during the 2020 taxable year, you may generally defer up to $26,000 into your 401(k) plan.

Healthcare FSA

The annual limit for participant salary reductions for the healthcare flexible spending account (FSA) for plan years starting on or after January 1, 2020, may not exceed $2,750. However, this does not preclude employer contributions (as long as they are not convertible to cash) from being added to participants’ healthcare FSAs.

Adoption Credit

For 2020 this tax credit is $14,300. The credit starts to phase out at $214,520 of modified adjusted gross income (AGI) levels and is completely phased out when modified AGI reaches $254,520.

The exclusion from income provided through an employer or a Section 125 cafeteria plan for adoption assistance also has a $14,300 limit for the 2020 taxable year. And remember – a participant may take the exclusion from income and the tax credit if enough expenses are incurred to support both programs separately.

Health Savings Account (HSA)

Minimum deductible amounts for the qualifying high-deductible health plan (HDHP) increased to $1,400 for self-only coverage and $2,800 for family coverage for 2020. Maximums for the HDHP out-of-pocket expenses increased to $6,900 for self-only coverage and $13,800 for family coverage for 2020.

Maximum contribution levels to an HSA for 2020 increased to $3,550 for self-only coverage and $7,100 for family coverage. The catch-up contribution allowed for those 55 and over is set at $1,000 for 2020. Remember, there are two general requirements in order to fund an HSA: You must have qualifying HDHP coverage and no other impermissible coverage (such as coverage under another employer’s plan or from a healthcare FSA that is not specifically compatible with an HSA).

Archer Medical Savings Account (MSA)

For high-deductible insurance plans that provide self-only coverage, the annual deductible amount must be at least $2,350 but not more than $3,550 for 2020. Total out-of-pocket expenses under plans that provide self-only coverage cannot exceed $4,750. For plans that provide family coverage in 2020, the annual deductible amount must be at least $4,750 but not more than $7,100, with out-of-pocket expenses that do not exceed $8,650.

Although new MSAs are not allowed, maximum contributions to existing MSAs that are attributable to single-coverage plans is 65 percent of the deductible amount. Maximum contributions for family-coverage plans are limited to 75 percent of the deductible amount. MSA contributions must be coordinated with any HSA contributions for the taxable year and cannot exceed the HSA maximums.

Qualified Small Employer Health Reimbursement Arrangement (QSEHRA)

The annual limit for employer-sponsored QSEHRAs is $5,250 for those with single coverage and $10,600 with family coverage for 2020.

Dependent and/or Child Daycare Expenses

Just a reminder that although the daycare expense limit associated with a cafeteria plan is not indexed, the tax credit available through a participant’s tax filing was raised in 2003. The daycare credit must be filed on Form 2441 and attached to the 1040 tax filing form. Limits for daycare credit expenses are $3,000 of expenses covering one child and $6,000 for families with two or more children. If one of the parents is going to school full time or is incapable of self-care, the non-working spouse would be “deemed” as earning $250 per month for one qualifying child and $500 for two or more qualifying children. This “deemed” earned income is used whether a person is using the employer’s cafeteria plan or taking the daycare credit.

The cafeteria plan daycare contribution limit is $5,000 for a married couple filing a joint return, or for a participant filing a single return, or filing as “Head of Household.” For a married couple filing separate returns, the limit is $2,500 each. The daycare credit is reduced dollar for dollar by contributions to or benefits received from an employer’s cafeteria plan. An employee may participate in their employer’s cafeteria plan and take a portion of the daycare expenses through the credit if they have sufficient expenses in excess of their cafeteria plan annual election, but within the tax credit limits.

Commuter Accounts

For 2020 the monthly parking limit is $270 and the 2020 monthly limit for transit also increases to $270.

Long Term Care

For a qualified long term care insurance policy, the maximum non-taxable payment increases to $380 per day for 2020.

Finally, by participating in a cafeteria plan, the participant will be lowering their income for the Earned Income Tax Credit (EITC). Check out the new limits in IRS Publication 596 “Earned Income Credit” and for more information about this tax credit.

The information contained in this article is not intended to be legal, accounting, or other professional advice. We assume no liability whatsoever in connection with its use, nor are these comments directed to specific situations.