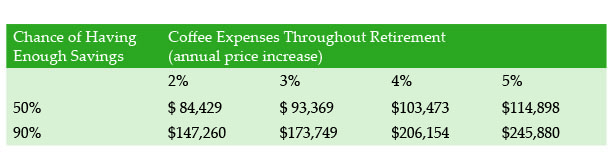

A new study by the Advantage Compendium Scary Math Institute concludes an age 65 couple will need $93,369 in savings to have a 50 percent chance of covering coffee expenses during retirement and could need as much as $245,880 to have a 90 percent chance, as this frightening looking table clearly shows:

Savings Needed to buy two Starbucks Café Mochas per day (without donut-hole)

Individuals should be concerned about saving for out-of-pocket coffee expenses in retirement for a number of reasons. Medicare generally covers only about two-thirds of the cost of coffee health care (e.g. coffee enemas and drips) and zero coverage for recreational coffee usage. Issues surrounding retirement coffee security are certain to become an even greater challenge in the future.

Wasn’t that silly…

There are a number of issues with this fictional study that mimics the language of actual studies. One is that not everyone drinks coffee, so for them there is no expense. Second, one isn’t forced to buy their venti Café Mocha at Starbucks at $4.76 (including tax), which is the item used to calculate costs. They could buy generic coffee—or coffee from Canada—at a much lower price. Third, people don’t prepay for a lifetime of coffee, they buy it one cup or pound at a time. Even using the high side, the first year cost for those daily Starbucks coffees is a more manageable $3,400 and any price increases will hopefully match the cost of living raises in those Social Security checks. The reality is no one needs to set aside $245,880 by age 65 to buy coffee and presenting it this way is extremely misleading…but that doesn’t stop researchers from doing it as a form of fear mongering.

You’ve seen newspaper headlines such as “Medicare Beneficiaries Could Need $400,000 for Uncovered Health Expenses” and then citing some study. And the studies also include other scary remarks such as “Starting in 2020, new Medicare beneficiaries will no longer be allowed to purchase Plan F that covers the Part B deductible.” However, since this is designed to scare and not educate, what they don’t say is that the Part B deductible is only $135.50 per year for most, and that almost everyone will pay less than $500 a month to buy supplemental insurance to cover the uncovered health expenses (and even the drug donut-hole cost gap is scheduled to be mostly closed in 2020). Of course, the reason they don’t say it is no one will be afraid of having to pay an additional $135.50 per year—and $500 a month sounds a lot less scary than coming up with $400,000 in a lump sum.

Although part of the motivation for the researchers is that the scarier sounding the problem, the easier it is to get grant money for new research, I believe the fear mongering is largely well-intended. In this case fear is used to get political attention on both the largely unregulated world of medical and drug price-gouging, and gaps in coverage that can force a retiree to choose between eating and buying their pills. The reality is much can be done to lower medical costs and there are still gaps that can devastate the lives of millions of low income retirees unless fixed. But it would be nice if research studies simply presented their conclusions and left the hyperbole to the politicians.