The author would like to thank Jeremy Alexander and Monika Hunsinger of Beacon Research for allowing access to their comprehensive store of annuity sales data and granting permission for a portion of this research to be shared.

Data for this article was drawn from the Beacon Research “Fixed Annuity Premium Study.” The study reports sales data provided quarterly by participating insurance companies as well as results reported in statutory filings and other publicly available sources. Beacon checks this data for general reasonableness, but does not perform independent audits. Beacon uses this data to estimate overall sales and sales by product type.

Beacon Research offers a suite of products to access industry leading annuity data mined from industry filings, researched from company websites, collected from annuity issuers and rigorously quality-checked by experienced data analysts and issuing companies. Beacon Research provides the most comprehensive and accurate fixed and variable contract and sales data in the industry. They can be contacted at 800-720-3504 or on the web at www.beaconresearch.net.

Overview

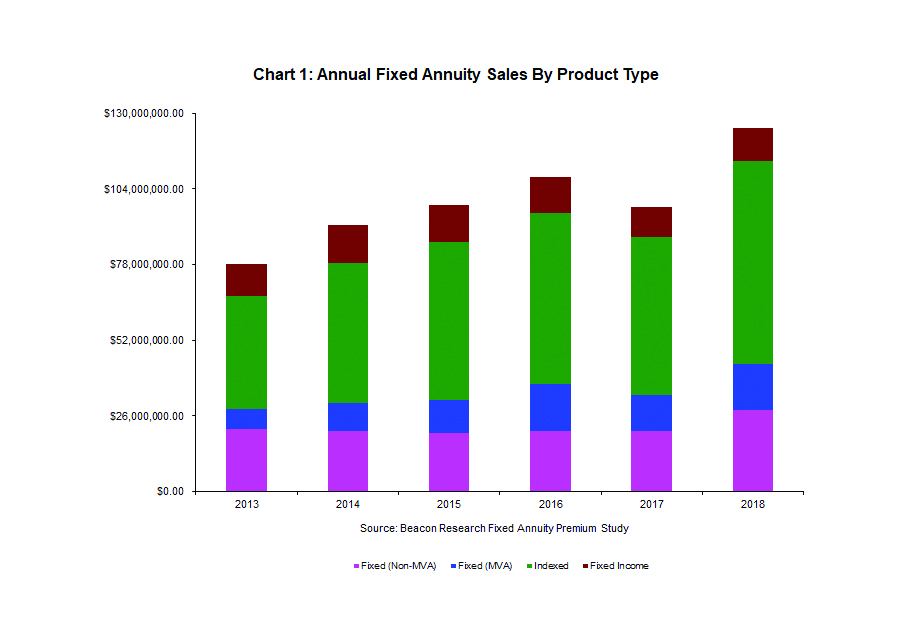

For calendar year 2018 estimated U.S. fixed annuity sales were $125 billion, up 28 percent from 2017.

With the exception of fixed income, all other fixed annuity segments posted double digit increases. Fixed rate annuity sales, including both market value adjusted (MVA) and non-MVA, exploded from $33.1 billion to $43.7 billion. Fixed index annuity sales jumped from $54.3 to $69.9 billion. Fixed income—deferred income annuities (DIA) and immediate income annuities—increased nine percent from the previous year to end up at $11.4 billion.

Product Trends

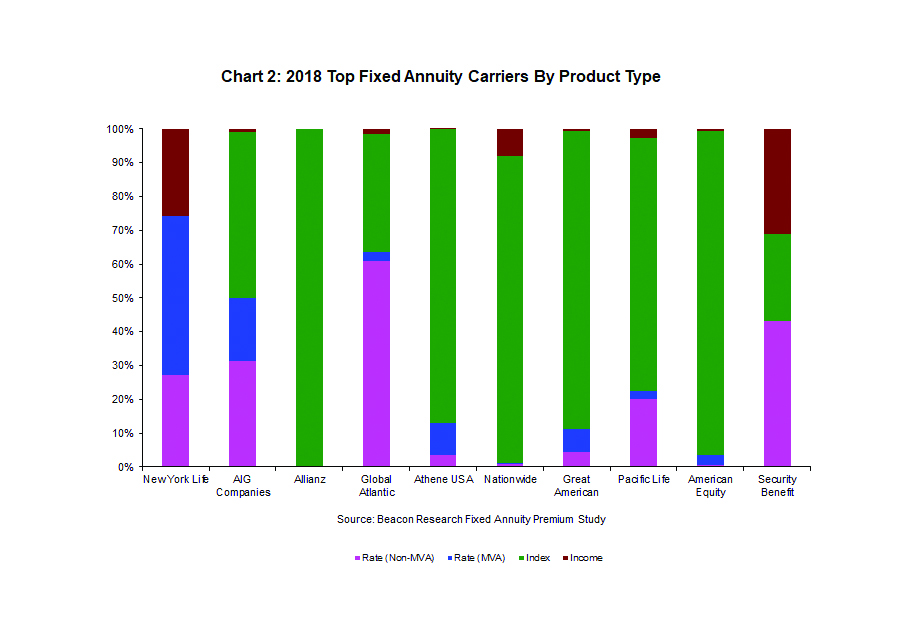

Once again, the Allianz 222 was far and away the top selling fixed annuity, followed by New York Life Secure Term MVA Fixed Annuity.

Four of the top ten selling fixed annuities were fixed rate (non-MVA), three were fixed index, two were fixed rate (MVA) and one fixed income (SPIA) completed the field.

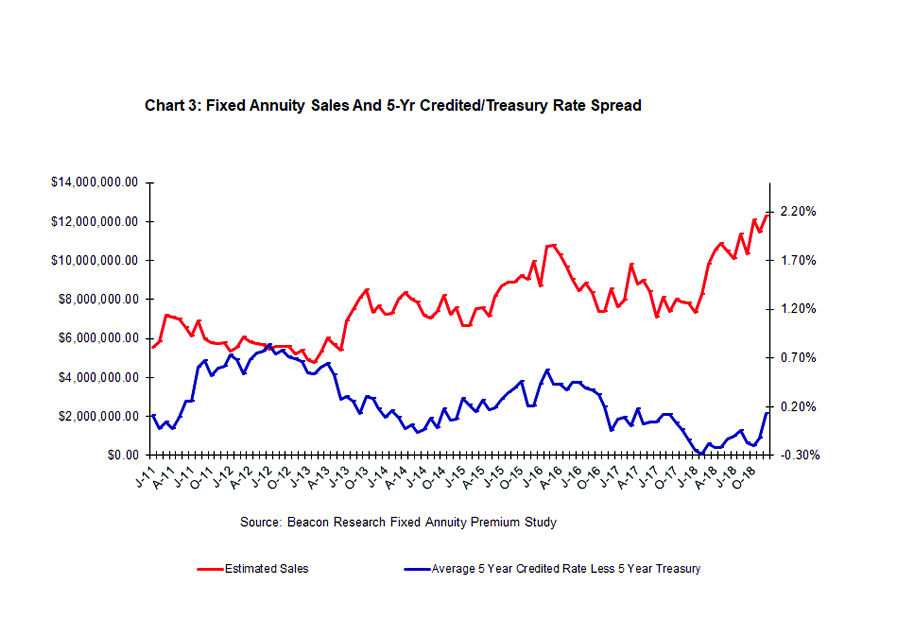

Overall sales rose eight percent in the first quarter of 2018 when compared to the fourth quarter of 2017, and then jumped up more than 25 percent in the second quarter. Third quarter sales were flat, but rose again by 13 percent when comparing the fourth quarter to the third. When compared to fourth quarter 2017 sales, fourth quarter 2018 fixed annuity sales were up 52 percent.

Interest Rate Trends

Overall interest rates were higher at the end than at the beginning of the year. The Advantage Insurer Bond Yield Index had the overall average yield on new bonds purchased by insurers at the end of 2017 at 3.78 percent and at 4.55 percent at the end of December 2018. In recent months interest rates have trended significantly lower.

Fixed annuity rates ended the year up three-quarters percent from where they began. The average yield on five-year multiple year guaranteed annuities (MYGA) was 2.04 percent in December 2017 and 2.81 percent in December 2018.

Best Selling Products By Channel

The top 10 selling products in the independent channel space and top eight in the independent broker/dealer channel are all fixed index annuities; in the wirehouse space fixed index annuities had nine out of ten slots. This contrasted sharply with the large regional broker/dealer channel where only one company with two index products cracked the top ten; in the large regional broker/dealer channel fixed rate (MVA) annuities had the lead. In the bank channel, fixed rate annuities also had the edge. (View complete list here)

Distribution Trends

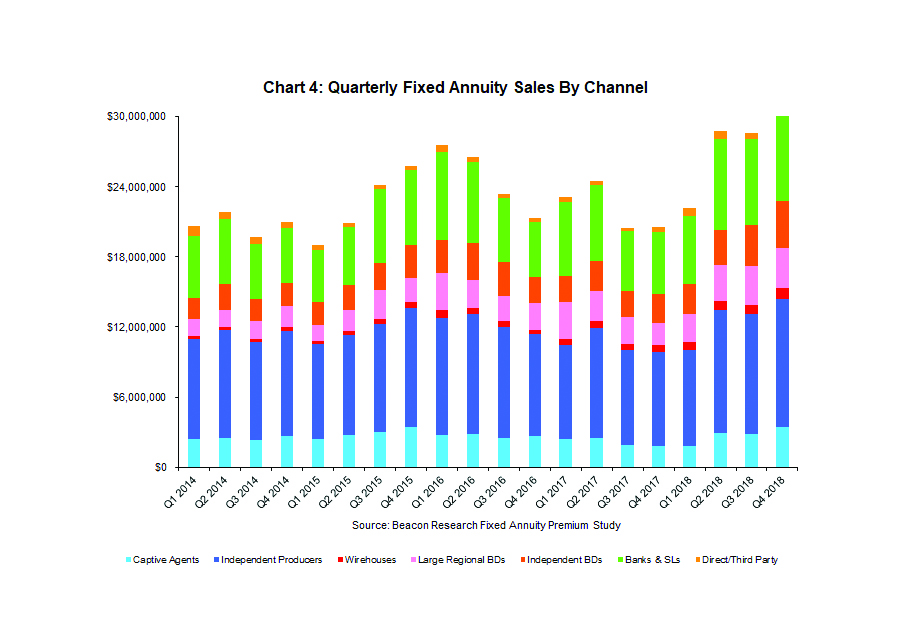

In 2018 captive and independent agents were responsible for more than 45.6 percent of total fixed annuity sales, down from more than 50 percent two years prior. Also in 2018 banks did 26.2 percent of sales with wirehouses and broker/dealers contributing 25.7 percent—up almost four percent from 2015; direct sales were at 2.5 percent.

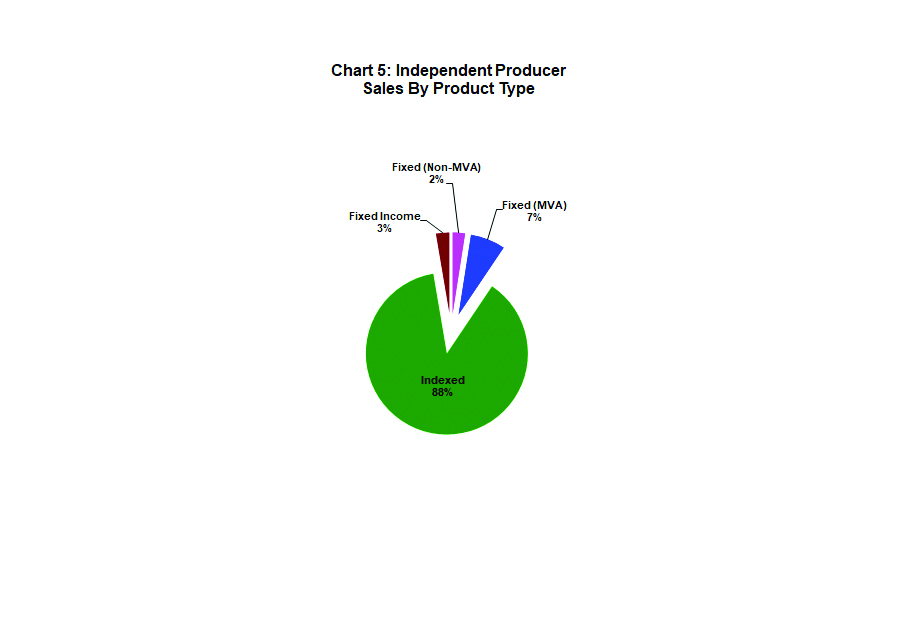

Roughly 90 percent of independent agent sales were in fixed index annuities; they represent less than three percent of total immediate and deferred immediate annuity sales.

The Forecast

With the uncertainty of the Department of Labor’s ill-conceived and poorly-written Fiduciary Rule Revision swept away, fixed annuity sales recovered and then soared last year. Although the interest rate picture has become cloudier as 2019 progresses, the forecast is for another record setting year for fixed annuity purchases.