(Reprinted from the CLTC Digest in cooperation with Certification for Long-Term Care, LLC, www.ltc-cltc.com. Email Amber Pate at apate@ltc-cltc.com for a more than 20 percent discount on CLTC training for Broker World subscribers—just mention code BWMAG.)

What do you think will be the breakthrough way to help get the mass market a Long Term Care insurance plan? —Mass Marketing in Massachusetts

Dear Mass Marketing,

Whether true or not, long term care insurance (LTCI) can be perceived as too expensive for the average consumer. It does not help when high cost plan designs are presented to prospective customers. The quotes are usually well-intentioned–after all the cost of care continues to march higher at an unprecedented pace. However, the result is that LTCI feels out of reach for many consumers.

I recently spoke with a senior insurance executive who shared an analogy to the early days of 401(k) planning. Retirement planning companies used to run 401(k) campaigns to build awareness about the amount of money needed to provide future retirement income to keep pace with longevity. The companies were surprised to discover that employees who were given a retirement target of many millions of dollars would not save anything at all! The reason–they felt the target was unachievable and gave up saving altogether. Eventually, the 401(k) companies got smarter and shifted their focus on a more personal solution of “what’s your number?” This connected better with consumers who realized that everybody’s retirement savings goals were different based on their individualized needs. It turns out a partial retirement plan is much better than no plan at all.

The same is true of long term care planning. Cost of care surveys can drive agents and advisors to present target benefits in the millions of dollars and cause people to delay or give up on long term care planning. Consider a different approach of focusing on a more personalized solution tailored to that client’s needs and maximizing value for their budget. This way, we can begin the process of partially insuring the long term care risk. Still included in these LTCI plans are peace of mind, guidance for the family, buying them more time at point of claim, caregiver training, and the list goes on.

Even if affordable LTCI plans can be presented, there still need to be incentives for early planning and a way to market these benefits to consumers. This is another way we can gain inspiration from the 401(k) world. Employees can save in their 401(k) plans with pre-tax dollars creating a valuable incentive to participate. Employers get a tax deduction for matching contributions up to a limit. Of course, employees participate at higher rates when employers offer matching contributions. Participation is also reinforced by financial advisors who often recommend maximizing the 401(k) match available. Finally, employers can market retirement planning to their captive employee audience reminding them of this valuable benefit on a regular basis.

There are various long term care think tanks that are working on new ideas for government programs to incentivize long term care planning, but what if we explore the LTCI advantages that already exist? Can the LTCI world replicate the success of the 401(k) world?

- Employer paid LTCI premiums are tax-deductible for employees and their spouses. Check.

- Employee paid premiums are not deductible, but benefits are tax-free instead. Check.

- A staggering 56 percent of employed caregivers work full-time1—LTCI resonates with employers and employees. Check.

As it so happens, LTCI may be a great complement to one of the bigger risks that the 401(k) retirement plan faces–an extended long term care event that could deplete significant 401(k) dollars. With employer sponsored LTCI, a strong incentive can be provided for consumers to begin planning early for the long term care risk.

401(k) plans have managed to succeed despite many challenges in their marketplace. LTCI plans in the worksite face unique challenges too. Guaranteed issue plans have proven to not be viable for insurance companies. Therefore, the existing offerings require prudent underwriting of the entire group with high minimum participation requirements or prudent underwriting of the individual during enrollment without participation requirements. Partially employer funded plans may require unisex pricing, which is available from fewer carriers. On the positive side, employees incentivized with affordable plans and employer funding are more likely to plan early, which also makes it more likely that they can qualify for coverage with underwriting.

The key to overcoming the challenges is setting expectations with employers and employees early in the process. Like an individual needs a plan that fits their budget, employers also need funding options that fit their benefits budget. Employees need to understand the value of the plan they are purchasing and whether they can qualify for plans with underwriting early in the process. Alternative planning options can be identified if a client does not qualify. Most important, employers need to understand the value of LTCI coverage to both themselves and their employees. Long term care events can deplete a company’s most important asset–its people.

Employees with competing priorities for their hard-earned dollars may still delay planning because the risk is either too far away or they think it’s unlikely to happen to them. This opens the opportunity to incorporate life/long term care hybrid solutions or traditional LTCI with return of premium. Employer funded traditional LTCI premium may still be tax deductible, even with a return of premium option, but you should consult your client’s tax advisor for their specific situation. The hybrid approach of providing value in the event that care is not needed can be compelling, especially for younger employees.

Inside the Numbers

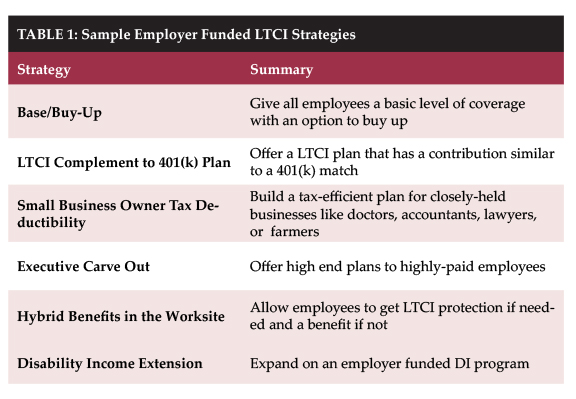

The majority of worksite LTCI plans are voluntarily purchased by employees. Consider shifting some of the employer’s total benefit spending to a tax-deductible LTCI contribution instead. Table 1 shows you a few strategies to help promote employer funded LTCI.

Base/Buy-Up

With this strategy, the employer funds a base plan for all employees with a voluntary option to purchase more coverage. The employer contribution to the base plan can free up funds for an employee to purchase additional benefits or a plan for their spouse.

LTCI Complement to 401(k) Plan

Employers are already familiar with 401(k) strategies. LTCI can be designed in a similar way. Allow the employee to voluntarily purchase a plan with the employer offering to match the purchase dollar-for-dollar. The employer can control the total spend by limiting the amount of the total match.

Small Business Owner Tax Deductibility

Most profitable businesses can deduct LTCI premiums. C-Corporation owners can generally deduct LTCI premiums in full subject to it being reasonable compensation. Self-employed business owners, S-Corporations, or Partnerships may be eligible for an “above the line” self-employed health insurance deduction subject to an annual limit. For premiums paid in 2018, the deduction allowed per person is the amount of premium paid up to $1,560 between ages 51-60 and $4,160 between ages 61-70.

Executive Carve Out

Businesses often offer tax deductible benefits programs intended to attract and retain key employees. The advantage for LTCI is that the LTCI benefits are still received tax-free. Also, employers can define rules to “carve out” eligible participants using criteria such as job title, tenure, or salary. Creative plans can be designed to use LTCI benefits instead of corporate bonuses. Despite not benefiting from the tax deduction, non-profit entities such as hospitals, academic institutions, or governmental organizations commonly use benefit programs instead of other forms of compensation to recruit, retain, and reward talented employees.

Hybrid Benefits in the Worksite

Employers seeking a fresh approach to the LTCI market may find hybrid-style benefits that address objections. Life insurance-based plans or traditional LTCI plans with return of premium can be offered to fulfill this objective. However, traditional LTCI plans offer the advantage of generally being tax deductible with flexibility on recurring premiums and inflation protection options. This new-look approach to LTCI can also help respond to the rate increase concern. After all, if a rate increase occurs on a traditional LTCI plan with a return of premium option, premiums, including the increased premium, could be returned to the employee’s beneficiary. Return of premium also opens a world of advanced planning opportunities if the return of premium benefit can be provided back to the corporation like a COLI-style program or in a trust. Be sure to consult with a tax advisor when suggesting these advanced solutions.

Disability Income Extension

An employee’s most valuable asset is often their income. Many LTCI prospects have disability income insurance to protect their income. Disability income insurance often ends at the client’s retirement. LTCI can be positioned as an extension to that original plan to protect retirement income. DI protects income from disability during working years and LTCI can pay bills for custodial care due to a chronic illness both before or during retirement.

Other Enhancements

Worksite strategies can be aided by two additional LTCI advantages. First, LTCI plans can be designed with features that qualify for long term care Partnership protection in many states. Employees who might otherwise have to deplete most of their assets to qualify for Medicaid may be able to keep assets in an equal amount to LTCI benefits received. Second, more employee benefit programs offer Health Savings Accounts (HSAs) today due to the increasing popularity of high-deductible health insurance plans. If a company offers an HSA, it can be attractive for the employee to pay a portion of the premium using pre-tax dollars from an HSA.

The Bottom Line

There are insurance solutions available on the market today to help deliver long term care plans to the mass market. The biggest obstacle is customizing plans to meet each client’s unique needs and, most important, their budget. We can replicate the success of the 401(k) market by offering tax-deductible plans that are fully or partially funded by employers. Employees with some “skin in the game” often appreciate the employer’s contribution even more.

There are myriad creative ways to apply the unique advantages that LTCI already has in the worksite. However, many participants in the market have trouble seeing beyond the guaranteed issue approach. Prudent underwriting can lead to more sustainable LTCI outcomes, benefitting all involved, in the form of more stable premiums and the availability of richer benefits.

Employers, whether large or small, are so focused on the day-to-day running of their businesses that they miss opportunities to protect themselves and their employees. Even insurance agents who are small business owners overlook LTCI benefits for themselves and their employees. As you consider offering one of the strategies above, consider your own plan first. This will give you the value of your own personal experience and story to share during your next presentation.

References:

1. Family Caregiver Alliance National Center on Caregiving. “Caregiver Statistics: Work and Caregiving.” Caring for Adults with Cognitive and Memory Impairment | Family Caregiver Alliance, 2016, http://www.caregiver.org/caregiver-statistics-work-and-caregiving.

Every situation is unique, so always have your client consult their long term care, legal, or tax advisor. The views discussed in this article are opinions of the author, and not National Guardian Life Insurance Company (NGL), LifeCare Assurance, or CLTC.