Background

The COVID-19 pandemic and shelter-in-place restrictions have highlighted the need for businesses today to be technologically agile and operationally efficient. The world around us is becoming increasingly customer-centric, but the goal of creating a simple, sleek, and pleasant customer experience is intertwined with an organization’s ability to navigate the digital space. While the technology and retail industries have spearheaded this revolution, in many ways the insurance industry is still stuck in the old paradigm of complexity and antiquated technology. Excessive paperwork, complex policy language, and delayed claims payments have plagued all aspects of the insurance industry for decades. However, innovative carriers in the supplemental benefits industry are trying to eradicate this long-standing perception from the mindset of their customers. One emerging area of insurer investment is a new capability known as “claims integration.” Because this concept takes on various levels of assistance for consumers, the meaning often can vary depending on the audience. The ultimate goal is a fully adjudicated process, typically called “auto-adjudication,” where no consumer action is necessary to submit or validate a claim. As this is a new and innovative service, terminology utilized in the industry to describe variations of claims automation has been inconsistent at best, which has contributed to confusion. To add clarity to the conversation, let’s first define a few of the variations.

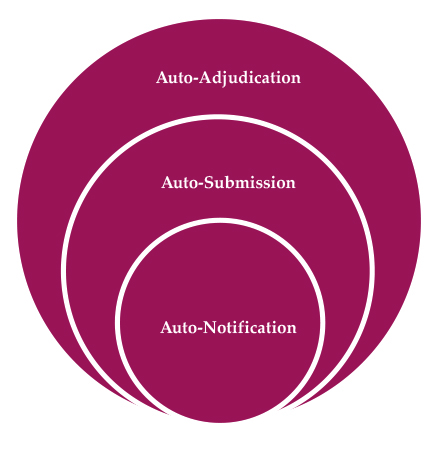

- Auto-notification/auto-indication: When a covered insured experiences an event that potentially qualifies for payment under the supplemental product’s contractual terms, that person is automatically notified of the eligibility for a benefit payment. All other elements of the claims process are unchanged. The insured is tasked with filing the claim with the carrier for the claims process to begin. Adjudication of the claim would then be handled by the insurer’s claims department using normal processes.

- Auto-submission: When a covered insured experiences an event that potentially qualifies for payment under the supplemental product’s contractual terms that claim is automatically submitted to the carrier’s claims process without the insured’s intervention, though the insured may be notified of this auto-submission. At this point the carrier will process the claim using normal methods in order to determine whether the event qualifies for a payment with known information or whether additional information will need to be requested from the customer. Auto-submission can be considered auto-notification plus the additional service of automated claims submission, though customer notification may not be necessary as the customer is not required to initiate the claim. Requests for follow-up information, though, are still a possibility.

- Auto-adjudication: When a covered insured experiences an event that potentially qualifies for payment under the supplemental policy’s terms the claim is automatically filed, processed, and, if payable, paid to the covered insured with minimal human intervention from either the covered insured or carrier. This is the “gold standard” of claims integration methodology that many carriers are striving to achieve. Auto-adjudication is functionally auto-submission plus implementation of methodology for the carrier to process claims with little to no human intervention.

Uses and benefits of claims integration

Many consumers find substantial value in supplemental health products when faced with both anticipated and unanticipated health expenses. In times when a consumer is responsible for deductibles and copays for health treatment or costs outside the scope of major medical, supplemental coverage can help to fill in the gap and provide financial stability to those experiencing unwanted health issues. Insureds who have purchased supplemental health coverage will receive extra cash that can be used to pay for both medical and nonmedical expenses (e.g., transportation, deductibles, equipment) that might otherwise deplete their savings. However, consumers are generally not as familiar with supplemental health products as other standard employee benefits such as term life and disability, and they can struggle to understand the benefits of the product.

Claims integration is an innovative technique within the supplemental benefits industry to enhance the customer experience and increase customer satisfaction by simplifying the claims submission process. If the carrier can develop a pleasant experience for the customer with each interaction, then satisfaction with the carrier and its products will likely increase. Consequently, the loyalty of the customer toward the carrier may increase as the carrier is perceived as an ally.

Imagine an individual suffers a heart attack and is confined to the hospital for three days following treatment. Upon returning home, the individual is focused on recovery and reacclimating to normal daily life. The last thing that person will want to do is to fill out insurance paperwork—especially if the insurer is already processing the heart attack claim under a major medical coverage. However, if the carrier develops an integrated claims process, then the insured can receive the supplemental payment with minimal hassle based on the major medical claims data and instead focus entirely on the recovery process. As the voluntary benefits industry strives to make successful inroads into consumer benefit offerings, presenting and marketing this valuable service to insureds can increase the awareness and perceived value of a supplemental benefit.

While we are very focused on the benefits for the customer, there are significant benefits for the carrier as well. First, variable expenses per claim should drop materially, as there is less human intervention within the claims adjudication process. Second, the time that staff previously spent on processing claims can now be utilized more effectively and efficiently in other internal business areas (e.g., process improvements, market intelligence, etc.). Finally, the carrier’s reputation and business retention will likely improve as customer satisfaction increases.

Lastly, imagine the likely benefits to the writing agent. In a full auto-adjudication setting the agent can reassure clients that their benefits will not be lost due to failure to file paperwork. Complaints about nonpayment or delayed payment of claims may be dramatically reduced. Quicker processing of the supplemental claim will likely strengthen the relationship among the employee, employer, and broker, which can translate into greater loyalty and potentially more sales.

Selling a product with claims integration

The value of supplemental products can significantly increase when claims integration is available as a product feature. With this additional value, marketing supplemental products may become easier and more consumer-friendly. Most customers appreciate simplicity; claims integration fits this perfectly. Conventional products require customers to put forth some effort in order to receive a benefit, which may place a significant burden on someone who has recently experienced a significant health event. Claims integration provides increased marketability and selling points for brokers in the sales process.

Some questions that may arise are, “Who pays for this additional benefit?” “Is the additional cost put on the employee, employer, or insurer?” “Will products with these additional features have a higher cost?” Streamlining the claims process should ultimately help to decrease variable expenses; however, claims volume will likely increase due to the claims generated from the integrated platform. The initial cost of developing the claims integration platform and features can be material due to the intricacies of the concept. Currently, carriers are evaluating the cost of building a claims integration infrastructure as compared to the expected improvements in sales volume, persistency, and other customer satisfaction metrics. The anticipated costs for each carrier will vary depending on access to data, current technological capabilities, and underlying claims behavior assumptions as well as the level of claims integration attempted. Knowing how each carrier handles these costs and being up-front with clients about this is paramount to a successful sale. Experts can provide a wide variety of assistance including product restructure support to facilitate claims integration or assistance with medical record code interpretation and mapping.

Challenges of claims integration

The benefits of claims integration come with certain challenges that are due to dependencies on claims data. While medical data is ideal, accessing it may be challenging for some carriers, particularly when the carrier offering the supplemental benefits coverage is not providing major medical health coverage. In some instances carriers may adjudicate supplemental benefits claims using alternative sources such as disability claims, life claims, or other available data sources.

In the development of a claims integration process, the carrier will have to implement the proper claims adjudication methodology. Implementation involves complex algorithms that utilize medical coding information. The quality of customer experience is directly tied to the quality of the claims integration algorithms. Sometimes carriers may need to modify contract language and limitations (and potentially pricing) to facilitate system and data needs as they move toward full claims integration. To quickly and efficiently build solutions to these challenges, it may be more effective to use the support of external experts to assist in the development of the claims integration processes. Experts can provide a wide variety of assistance including product restructure support to facilitate claims integration or assistance with medical record code interpretation, medical code mappings, and claims processing algorithms.

Due to the manual nature of claims submission, currently some insureds may not file for a benefit on all qualifying claims. Thus, upon implementation of claims integration, benefit utilization is expected to increase by varying degrees depending on the level of automation. As experience is tracked, insurers will gain the necessary data to ensure that the process is running smoothly and is consistent with customer, broker, and company expectations.

Finally, carriers need to be conscious of privacy concerns, which include recognition of HIPAA and other data privacy requirements. Medical records can only be released with the consent of the individual or a guardian. Carriers will need to ensure they have the appropriate documentation and consent to use the medical claims data within the claims integration process. Unless the carrier is simultaneously offering medical and supplemental benefits under the same legal entity, it may be more difficult for a supplemental benefits carrier to obtain the necessary information to automatically process and pay claims. This puts medical carriers at a competitive advantage, compared to true supplemental carriers. In some instances, supplemental carriers may be able to adjudicate claims utilizing non major medical data, such as disability or other claims processed by the carrier.

Current status of market

As of this article’s publication, multiple carriers have implemented auto-notification and are advertising this capability. Some carriers are also auto-submitting claims, which, in limited circumstances, has resulted in auto-payments. While this innovation is in early stages of implementation and still being perfected, these examples show how the supplemental health industry is driven to improve the customer experience. We expect to see significant developments in capabilities over the next two years.

Technology behind claims integration

Many carriers have started the process of implementing some form of claims integration through utilization of Excel-based models that retrieve and analyze claims data and identify potential supplemental claims. After gaining experience and understanding the process, they have begun to create internal proprietary platforms that automatically analyze and process claims data and subsequently notify the insured or submit the claim for review. Carriers can also leverage other options such as third-party software or benefit administration platform capabilities to meet their specific needs.

Conclusion

As the industry transitions to being more customer-centric, implementing claims integration will likely become a must-have feature. This capability allows individuals to fully access and utilize the inherent value in supplemental health products and provides a smoother claims experience for all involved.

The additional value provided by claims integration has the potential to boost customer awareness of these products, increase customer satisfaction, and attract more purchasers. In addition, it’s not just medical carriers that are able to implement claims integration, but all carriers offering supplemental benefits have the opportunity to modernize their products. Within the supplemental industry the concept of integration is in its infancy, but as it quickly matures promising results have already been obtained. Moving forward, agile carriers will be able to react to changes in the marketplace as this feature develops, leading to successful implementation of claims integration.

Obstacles are likely to present themselves as various carriers tackle this new adventure, hindering the transition to claims integration. Experienced experts are available to support carriers as they develop claims integration processes. Assistance can include support with claims code mapping and product refreshes to modernize benefits and features as well as facilitate claims integration. In short, there is no reason that claims integration cannot become the new norm for all carriers, resulting in a better experience for consumers everywhere.