And Flexible Benefits Plans")

This article examines the rules for participants going on an unpaid Family and Medical Leave Act (FMLA) leave. Internal Revenue Service (IRS) Regulation 1.125-3 summarizes employees’ rights to continue or revoke coverage and cease payment for healthcare flexible spending accounts (FSAs) when taking an unpaid FMLA leave and specifications for participants returning from leave. The leading principle outlined mandates employers offer coverage under the same conditions as would have been provided if the employee were continually working during the entire leave period.

Coverage Continuation

Employers may require an employee who chooses to continue coverage while on FMLA leave to be responsible for the share of premiums that would be allocable to the employee if the employee were working. FMLA requires the employer to continue to contribute their share of the cost of employees’ coverage.

Flexible benefits plans may offer one or more payment options to employees who continue coverage while on unpaid FMLA. These options are pre-pay, pay-as-you-go, and catch-up.

- Pre-pay is paying for coverage in advance of the FMLA leave. This may be a difficult method of continuing coverage for a couple of reasons. The first consideration is if participants cannot afford to have extra funds taken from their paycheck and the second consideration is a timing issue. Most leaves involve an incident or circumstance that is not planned, making the pre-pay option impossible to deduct from participants’ paychecks. However, if planning in advance is feasible, the coverage can be paid on a pre-tax basis through the flexible benefits plan.

- The Pay-as-you-go option means that participants pay their share of coverage payments on a schedule as if they were not on leave. This method would require the participant to write a check to the employer each month or pay period in order to continue coverage. Since no payroll is taking place, this payment is with after-tax dollars.

- Catch-up contributions allow employees to continue coverage but suspend coverage payments during their leave. Contributions are made up upon their return. The advantage is that contributions can be taken out on a pre-tax basis through a flexible benefits plan. The downside for the employer is if the participant does not return from the leave, the employer may have reimbursed expenses in anticipation of the participant making up the coverage payments.

The flexible benefits plan may offer one or more of the payment options and may include the pre-pay option for employees on an FMLA leave even if this option is not offered to employees on a non-FMLA leave. However, the pre-pay option may not be the only option offered.

As long as employees continue healthcare FSA coverage, or employers continue it on their behalf, the full amount of the election for the healthcare FSA, less any prior reimbursements, must be available to the participant at all times, including the FMLA leave period.

Coverage Revocation

Prior to taking an unpaid leave, participants may revoke existing healthcare FSA coverage. Failure to make required payments during an FMLA leave may also result in lost coverage. Regardless of the reason for the loss of coverage under FMLA, plans must permit employees to be reinstated in the healthcare FSA upon their return.

Depending on the plan document language, returning employees may decide not to elect coverage into the healthcare FSA; or plans may require returning employees to be reinstated in healthcare coverage. If the employer requires reinstatement into the plan, they must also require those returning from an unpaid leave not covered by the FMLA to also resume participation upon return from leave.

The employer also has the right to recover payments for benefits when the employee revokes coverage.

If coverage under the healthcare FSA terminates while employees are on FMLA leave, employees are not entitled to receive reimbursement for claims incurred during leave. Even if employees wish to be reinstated upon return for the remainder of the plan year, employees may not retroactively elect healthcare FSA coverage for claims incurred during leave when coverage was terminated.

Employees have the right to reinstate coverage at the level before their FMLA leave and make up unpaid coverage payments, or they may resume coverage on a prorated basis at a level that is reduced for the period during FMLA leave for which no premiums were paid. This prorated level of coverage is further reduced by prior reimbursements and future coverage payments are due in the same monthly amounts payable before the leave.

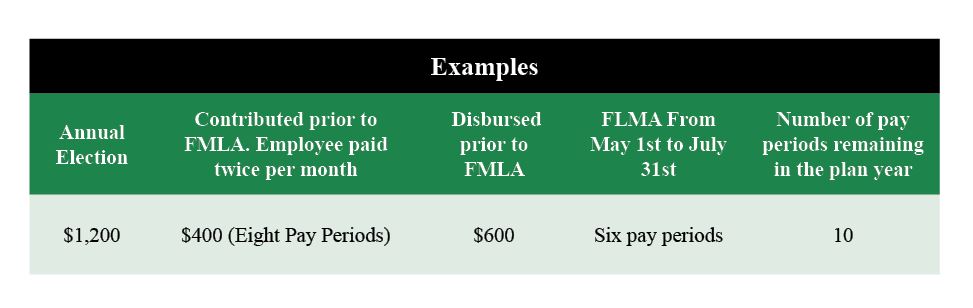

Reinstate Coverage. Using the above facts, and upon the participant’s return from FMLA, the annual election will remain at $1,200. The election, or coverage amount, for the remainder of the year is as follows: Original annual election minus reimbursed to date ($1,200 minus $600) equals $600. The new per pay period contributions will increase to $80 per pay period. Remember, they are making up contributions from the three-month leave. The employee will contribute $1,200 [$400 contributed prior to the leave plus $800 ($80 times 10)]. The employer exposure is $1,200 ($600 disbursed prior to leave plus $600 available upon their return. Now let’s see what happens if employees choose to prorate coverage upon their return from FMLA leave.

Prorate Coverage. The calculation is different in this instance. A new annual election is determined. This is done by prorating the original annual election for the months participants were absent. Using the same facts as previously, the annual election amount minus six pay periods that were missed ($1,200 minus $300) equals $900. The new prorated annual election, reduced by prior reimbursements ($900 minus $600), equals $300. The per pay period contribution remains the same as before at $50 per pay period. In this instance the employee will contribute $900 ($400 plus $500) with an employer exposure of $900 ($600 plus $300).

In either scenario, employees are not covered for the time they are on FMLA if coverage is revoked. They may not turn in claims that were incurred during leave whether they choose reinstatement or prorated coverage upon their return.

Certain restrictions apply when an employee’s FMLA leave spans two flexible benefits plan years. A flexible benefits plan may not operate in a manner that enables employees on FMLA leave to defer compensation from one plan year to a subsequent flexible benefits plan year. In other words, employees may not pre-pay for coverage in one plan year that pays for coverage in the subsequent plan year.

If on paid FMLA leave, the employer may mandate that the employee’s share of premiums be paid by the method normally used while the employee was working.

And finally, employees on FMLA leave have all the rights to change their elections according to the change in status rules under IRS Regulation 1.125-4 when returning from an unpaid leave of absence. They may also enroll in benefits for new plan years or any benefits that may have been added by the employer while they were on leave.

The information contained in this article is not intended to be legal, accounting, or other professional advice. We assume no liability whatsoever in connection with its use, nor are these comments directed to specific situations.

Changing Elections After The Beginning Of A Benefit Plan Year

Happy New Year! Benefit plans have started their new plan years and questions are already coming in about how and when participants may change their plan elections. So, it’s a perfect opportunity to review the change in election rules for the most popular benefits plans such as flexible spending accounts (FSAs) (cafeteria) plans, Health Reimbursement Arrangements (HRAs), Health Savings Accounts (HSAs), and parking and transit plans.

Cafeteria Plans

The IRS 1.125-4 Regulations outline a two-pronged approach to determining when a change may be made to an existing cafeteria plan election: (1) a change in status or a change in cost or coverage occurs, and (2) the election change satisfies the consistency rules. We’ll first look at the conditions necessary for a change and then discuss the consistency rule.

Although changes to current elections are not required in the plan document, most flexible benefit plan documents allow for election changes throughout the plan year. Please check your plan documents for specific rules surrounding allowable election changes.

Conditions for Change

Seven circumstances allow for changes to accident or health plans (including healthcare FSAs within a cafeteria plan), disability, group term life insurance plans, dependent care assistance, and adoption plans:

1) Special enrollment rights under HIPAA (Health Insurance Portability and Accountability Act). Allows for election changes on a prospective basis in the event of marriage (a HIPAA event). Election changes on a retroactive basis can be made for the HIPAA events of birth, adoption, or placement for adoption if the change is requested within 30 days of the event.

Also, the gain or loss of Medicaid or state children’s health insurance program (SCHIP) coverage in the cafeteria plan can be retroactive if elected within 60 days of the event.

2) Changes in status events.

3) Judgements, decrees, or orders. A conforming election change can be made that results from a divorce, legal separation, annulment, or change in legal custody (including a qualified medical child support order). Such a change would allow an increase to the election if the order was to provide coverage or it would allow the participant to cancel coverage if the order required another to provide coverage and if it was, in fact, provided by another.

4) Entitlement or loss of eligibility to Medicare or Medicaid. Allows participants to decrease or increase an election under an accident or health plan.

5) Significant cost or coverage changes: There are four events that apply to accident or health plans (not including healthcare FSAs), disability plans, group term life insurance plans, dependent care assistance plans, and adoption assistance plans.

Cost changes such as automatic increases or decreases in a qualified plan or significant cost changes. If the cost charged to an employee significantly increases, the employee may revoke an election and change to coverage under another benefit package option or drop coverage under the accident and health plan if no other benefit package option is offered. On the other hand, if the cost charged to an employee decreases significantly, an employee may commence participation in the cafeteria plan for the option with a decrease in cost.

This applies whether the increase or decrease results from an action taken by the employee (switching between full-time to part-time status) or from an employer increasing or reducing the amount of employer contributions for a class of employees.

Coverage changes such as a significant curtailment of coverage under a plan allow participants to revoke their election and, on a prospective basis, receive coverage under another benefit package option that provides similar coverage. A loss of coverage permits participants to revoke their election and elect coverage under another benefit package option or drop coverage under the accident and health plan if no other benefit package is offered. (A loss of coverage means a complete loss of coverage including the elimination of a benefits package option, a network ceasing to be available in the area, by reaching an overall lifetime or annual limitation, a substantial decrease in the availability of medical care providers, a reduction in benefits for a specific type of medical condition or treatment, or any other similar fundamental loss of coverage.)

A coverage change that adds to or improves an existing benefit package option allows eligible employees to revoke their election under the cafeteria plan and elect coverage under the new or improved benefit package. This includes employees who had made no previous election under the cafeteria plan.

A coverage change is made under another employer plan. This includes changes made during an open enrollment period or a valid change of status of spouse or dependent.

A loss of coverage for the employee, spouse, or dependent under any group health coverage sponsored by a governmental or educational institution, including a state’s children’s health insurance program (SCHIP), a medical care program of an Indian Tribal government, the Indian Health Service, a tribal organization, a state health benefits risk pool, or a foreign government group health plan.

These cost or coverage events would include situations in which an employee switches between full-time and part-time employment, an employer changes the percentage of premium that an employee must pay, or a new benefit option is added. The cost charged to an employee is the key factor in determining whether a cost change has occurred.

6) Family and Medical Leave Act (FMLA). Employees may revoke an existing election for group health plan coverage and make another election for the remaining portion of the period of coverage as provided under the FMLA.

7) 401(k) plans. Elections may be modified or revoked in accordance with 401(k) plan documents. Generally, most plan documents allow for changes on any pay period.

Consistency Rule for Accident or Health Coverage

The second part of the equation deals with whether the election change satisfies the consistency rule. The consistency rule applies to each employee, spouse, or dependent separately and basically requires that the election change be on account of and correspond with a change in status that affects eligibility for coverage under an employer’s plan. This includes an increase or decrease in the number of an employee’s family members or dependents who may benefit from coverage under the plan.

One exception to the consistency rule allows a plan to permit the employee to increase payments under the employer’s cafeteria plan if the employee, spouse, or dependent becomes eligible for COBRA under the group health plan of the employee’s employer.

Keep in mind that, under these rules, the change occurs when an employee, spouse, or dependent gains or loses coverage eligibility for accident or health coverage and group term life insurance. Therefore, a spouse that goes on an unpaid leave of absence, where no eligibility change takes place, would not constitute a reason for the participant to change their coverage elections.

When a participant gains coverage under another employer’s plan and revokes his or her election, a certification that coverage was actually obtained should be sought from the employee.

Regulations do allow a participant to revoke their election and receive, on a prospective basis, coverage under another benefit package option that provides similar coverage by another employer, such as a spouse’s or dependent’s employer.

Note, however, that the “Significant cost or coverage changes” section of the regulations do not apply to healthcare FSAs. Employees may only change their election to a healthcare FSA if any of the other five “Conditions for Change” occur and the resulting election change satisfies the consistency rule.

Additional changes allowed for Marketplace enrollment: A change is allowed for employees to prospectively revoke or change an election with respect to an employer’s accident or health plan if the employee wants to begin participation during open enrollment or a Special Enrollment Period, such as marriage or addition of dependent, to a Marketplace Qualified Health Plan (QHP). The new coverage in the QHP must be effective no later than the day immediately following the last day of the original coverage that is revoked.

HRAs, HSAs, Parking and Transportation Accounts, and 401(k) Plans

HRAs: Employees do not elect into HRA plans. Their eligibility for the HRA is based on the criteria outlined in the plan document. For example, the eligible group may be all those that selected a particular employer-sponsored group health plan. However, under certain conditions, participants in the HRA may suspend their participation in the HRA before the HRA coverage period begins and forgo payment or reimbursement by the HRA to perhaps participate in an HSA or to seek Premium Tax Credits for marketplace insurance coverage. Employees may also switch from single to family insurance coverage, or vise/versa. Employers may make changes to their HRA plans at any time during or at the beginning of the plan year.

HSAs and Parking and Transit Plans: It’s a lot less complicated for participants that have an HSA or are enrolled in parking and/or transit plans. Basically, an election in any of these types of accounts may be increased or decreased for any reason on a prospective basis.

401(k) Plans—inside and outside of a cafeteria plan: Election, generally, can be changed on a per payroll basis without any sort of status change. The selection of the types of investment options for HSAs or 401(k) plans can be changed at any time from the plans’ portals.

Lastly, there may be one more avenue for changing an election to a cafeteria plan—when a mistaken election occurs. This would require clear and convincing evidence that a change is needed. For example, if a participant signed up for the dependent care benefit, thinking it was for healthcare expenses of a dependent, although no child under the age of 13 resides in their home.

Of course, plan documents must be consulted to see when and how changes to elections may be made for any particular benefit plan.

The information contained in this article is not intended to be legal, accounting, or other professional advice. We assume no liability whatsoever in connection with its use, nor are these comments directed to specific situations.