(Reprinted from the CLTC Digest in cooperation with Certification for Long-Term Care, LLC, www.ltc-cltc.com. Email Amber Pate at apate@ltc-cltc.com for a more than 20 percent discount on CLTC training for Broker World subscribers—just mention code BWMAG.)

As an independent financial advisor and RIA, I help my clients develop a holistic financial plan. My primary expertise is managing investments, but clients frequently ask about insurance planning too. How can a busy professional, who is not regularly immersed in insurance, help clients navigate the myriad of possible solutions? —Advising in Arizona

Dear Advising,

My grandmother used to say a Yiddish expression that translated to “nobody can have it all.” We need balance in both our lives and businesses regardless of our ambitions. Time is our most valuable asset, so is it worth your time to be an expert in several lines of insurance? Learning the tradeoffs between insurance solutions, pricing, products, underwriting, funding strategies, tax implications, and policy language can be very time consuming. Luckily, you do not need to be an insurance expert to help get your clients expert advice.

In my current role as chief sales officer, I have the pleasure of collaborating with many of the finest professionals in the industry. I recently spoke to a CFP named Jane who built her practice by managing the financial affairs of many successful female entrepreneurs. Her clients are generally between the ages of 40 and 65 with insurance needs for themselves and their businesses. Although Jane is a licensed life and health insurance agent, she chooses to partner with insurance specialists who provide her with ideas to protect her clients’ incomes and assets. Her value proposition is a high level of client service, but she has little time to analyze insurance products and solutions. By tapping into her network of trusted insurance experts, she can timely deliver solutions to meet her client’s needs and answer questions as they arise. She saves time and finds herself more productive than ever before.

Partnering with a specialist or doing “joint work” as it is sometimes called, is not limited to financial planners. Agents working in life insurance, LTCI, health, annuities, disability, and property and casualty are all frequently in need of an expert resource for other insurance lines, which is why joint work has been utilized by career agencies for generations. Under this model, partnering with a specialist often becomes an apprenticeship. It also provides a unique perspective to be sitting on the client’s side of the table while observing an expert at work.

Traditionally, the limitation of joint work is finding a trusted relationship in the local community with someone who has the right expertise. The biggest fears of the referring agent are that the specialist will somehow embarrass them or steal the client. Like any new relationship, trust is built over time. The right relationship should be mutually beneficial and symbiotic with the referring agent bringing the relationship to the table and opening the conversation, and the specialist providing expertise to develop a solution that meets the client’s needs and wants.

Technology and modern marketing are a gamechanger when it comes to the joint work model. Specialists can now easily obtain licenses in multiple states and be available for online consultations with screen sharing and web cams. The specialist can help the client complete an underwriting questionnaire remotely without having the advisor learn sensitive information about their client’s health, and applications can be submitted electronically through most carriers’ websites.

Finding a specialist is easier than ever before. Specialists can gain exposure by marketing on the web and by sharing their client stories. Social media can build a warm relationship without the professionals having to ever meet in person. Modern marketing can be the foundation for a long-term profitable partnership.

Inside the Numbers

I informally surveyed both brokerage general agencies (BGAs) and LTCI specialists to answer the following question: Are two professional minds better than one?

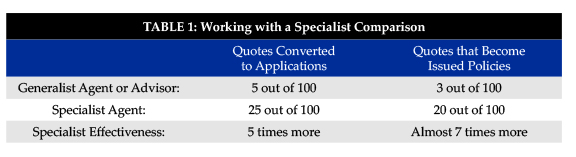

The BGAs self-reported their LTCI success rates:

- As few as five percent of unique client quotes run for generalist agents or advisors are converted into submitted applications. BGAs that also provide some point-of-sale support might see their success rates double.

- On average, about 60 percent of LTCI cases submitted by generalist agents are issued. Brokers who submit infrequent cases tend to have less success in underwriting and placing coverage.

LTCI specialists, who spend the majority of their time offering LTCI solutions, self-reported strikingly different results:

- 25 to 50 percent of quoted prospects go on to submit an application. Success rates varied by the source of the prospect and the skill of the specialist

- About 80 percent of submitted business becomes issued. Specialists are more skilled at field underwriting and identifying the best fitting product.

The data indicates that specialist agents can be at least five times more effective at getting clients coverage than generalist agents.

The Bottom Line

Specialization seems to be the natural evolution for many industries that have increased in complexity. Take the medical field as an example. One hundred years ago there were primary physicians who handled most family medical issues in their offices or by making house calls. Now, you visit a doctor who is a general practitioner who gives you medical advice on a regular basis. If the doctor diagnoses a need for further evaluation, you may be referred to a specialist. As the medical field has evolved, the natural outcome is medical professionals have become increasingly specialized.

Insurance solutions are also very personal and customizable plans. The shared economy of insurance specialists can be a win-win for all involved:

- Consumers get much needed insurance protection and two financial professionals’ minds;

- Generalists save time, energy, and the trust of their clients;

- Specialists develop a consistent source of prospects;

- BGAs dedicate more time to cases that are likely to close; and,

- Insurance carriers save money with fewer not-in-good-order applications and fewer declines.

So, the next time you are exploring a new insurance strategy or line of business, consider instead saying, “Let me refer you to my specialist.”

Every situation is unique, so have your clients consult their long term care, legal, or tax advisor. The views discussed in this article are opinions of the author, and not National Guardian Life Insurance Company (NGL), LifeCare Assurance, or CLTC.

Disclosure: The author helps financial professionals and consumers connect with insurance specialists.