Today we are talking about a remarkably interesting topic that most consumers and advisors have never even heard of, or spent the time to truly dive into: Premium financing a life insurance policy. The reason this is a great topic is because I’ve heard many people in the past say, “Yes I want life insurance; I just don’t want to pay for it.” It’s the old “Have your cake and eat it too” saying at play here. If you are able to explain what life insurance can do for a client without calling it life insurance, I can promise you every person you speak to will want what you’re talking about—whether it’s protection for the family in case one dies too soon, tax deferred accumulation, tax free income, liquidity, use, control, or coverage in case of illness along the way. The list goes on.

My goal with this article is to show you how to use “OPM” (other people’s money) to pay for what I like to call the Swiss army knife of planning: Index universal life insurance. What makes this such a timely topic is that everyone is having cash flow constraints at the moment due to inflation and volatility. Being able to show a client that they can accomplish the same objectives with less out-of-pocket payments or accomplish three, five or even 10 times the amount of benefit using the same out-of-pocket payments is crucial. Everyone wins. Bonus points are in play for advisors focused on assets under management due to the fact that we are now giving your clients the benefits of life insurance without reducing your AUM dollar-for-dollar.

Whether your goal is to become an expert in legacy building, estate planning, tax-free income, insurance planning for your business, or to simply be your own banker and diversify and protect your money, this concept can be a perfect fit for a well-structured plan or portfolio.

Before we go over the “how,” let me set the stage.

I want you to raise your hand if you’re a little uncertain about the future of our economy. If your hand is up, don’t worry, you’re not alone. My hand (both of them, actually) and a lot of other people’s hands are up as well, and if your hand isn’t up then I’d say you’re either way smarter than all the rest of us or vice versa.

Why?

When it comes to investing over the last 10+ years we, along with our customers, have been at one of the best parties in the history of parties! An absolute rager! Unfortunately for most Americans though, the lights have come on, the proverbial punch bowl is empty, and it’s time to sober up and go home. This is a metaphor for the amount of “run up” the market and growth sectors have had for years. Now that the frothiness is subsiding, the market is repricing itself back to a more reasonable level and we are feeling the effects of the downward volatility. It is not all sunshine and roses in the investment world anymore.

We all know inflation has been running red hot. Due to the supply chain disruption the Fed will likely be raising rates throughout the year, which can cause volatility in the stock market and your investment accounts. Traditionally a safe alternative to stocks, bonds have had one of the worst starts to the year in a long time.

So the question is, where are your clients’ hard-earned dollars safe?

A good answer is with an insurance company, and specifically within cash value life insurance.

Remember, while everyone wants the benefits of life insurance, nobody wants to pay for it. As a quick reminder, IUL is a life insurance policy built for cash accumulation. You pay an after-tax premium, it builds up tax-deferred cash, and eventually there will be enough cash in the policy that you can use for tax-free income, large capital purchases, investing, business planning, etc. Again, the list goes on.

With that said, let’s talk about premium finance and some of the high-level mechanics.

With premium finance, instead of paying a premium directly to the insurance company, you will pay a contribution to a lender and the lender pays the premium for you to the insurance company as a loan. Eventually there is enough cash value in the life policy to pay the lender back using a participating policy loan from the insurance company, and your life policy is now free and clear from the lender to be that Swiss army knife of planning.

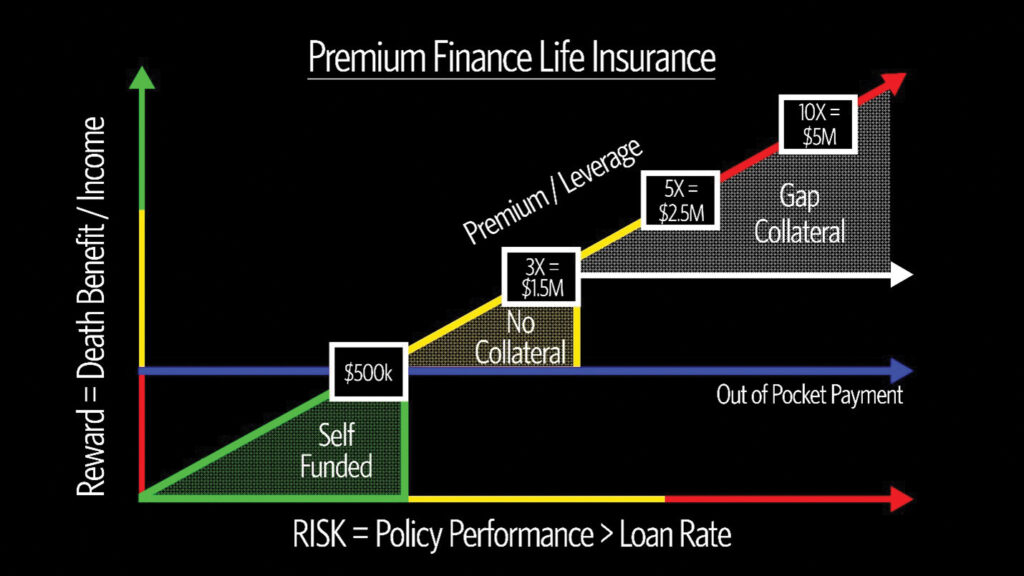

To better illustrate how to premium finance a life insurance policy, check out the graphic.

A couple key metrics here are the death benefit and income, premium, out-of-pocket contribution, collateral, and leverage. If you tell us how much you want to contribute, how much leverage you want, and what your goal is, we can design a plan to meet your objectives.

On our vertical axis we have the reward, which I like to think of as the good stuff. These are the benefits we already mentioned (death benefit and/or income, etc.).

On our horizontal axis we have the risk spectrum. This isn’t like the risk you’re familiar with though. Remember, we already said that life insurance is a great place to put assets right now, so this risk isn’t in the same category as stock market risk or inflation risk. This risk is defined as the possibility that your life insurance policy performance does not exceed the borrowing rate for your loan. Put another way, we are not able to sustain positive arbitrage between the loan rate from the bank and the credited interest to your index universal life policy. An important note here is that we only need to earn approximately two percent (2.5 percent above our borrowing rate) to have a successful plan depending on the amount of leverage used.

Our diagonal line is premium, which is typically correlated to the amount of leverage used. The more premium paid into the policy, the more reward you get. Notice the lower left portion is self-funded, which means we have the lowest risk but we also have the lowest reward. You do get compensated for the amount of risk you’re willing to take with lots of reward.

The blue line is your out-of-pocket contribution to the lender. Out-of-pocket will typically stay constant and is usually paid for five to 10 years. As your out-of-pocket goes up, so can the premium and ultimately your output which is more death benefit or income. If we keep your out-of-pocket the same, and increase leverage, then your output can go up as well. If we do this there is a chance you may need to post gap collateral (as shown in black). Gap collateral is roughly the difference between the cumulative loan and the cash value in the life policy. An important note here is that the low point cash value calculations that lenders use to calculate gap collateral is not as simple as a cumulative bank loan minus cash value of the policy math equation. Any loan ledger showing this as the collateral calculation should be of concern. This is the number one reason these plans do not stay on the books. Advisors do not do a good job explaining the collateral requirement. As a result, clients get upset and refuse to post collateral, lenders don’t pay the premiums and policies lapse. Lose, lose, lose. It’s crucial when you’re illustrating a plan that you stress test the collateral by increasing the borrowing rate or decreasing the policy performance. Therefore, the client is fully aware of potential future obligations.

Notice as we increase premium and keep the out-of-pocket the same, we are increasing leverage on the policy which can reap great reward. If we stay around three times leverage, we typically do not need any collateral. As we go above three times leverage there may be a need for gap collateral which is fine. When collateral is used correctly, it can reap lots of reward as well. Those who understand leverage in premium finance can keep their out-of-pocket costs low and reward extremely high. They are essentially getting all the benefits of life insurance without having to pay the full sticker price. OPM–other people’s money!

In this example in the graphic this person had an all-in budget of $500,000, and if they were to use leverage they could potentially get $5 million of premium into a cash value life insurance policy and ten times the amount of income and death benefit!

In sum, the entire premium finance plan is based on your goals and the amount of leverage with which you are comfortable. If you want to pay cash for your policy it can still easily meet your objectives. However, as we just showed, those that understand leverage and how to use other people’s money can take their same out-of-pocket premium they were going to use to pay cash for their policy and leverage it up to get three times, five times, even 10 times the amount of premium in the policy and reap 10 times the reward whether it be death benefit for your family or business or tax free income for your retirement.

Remember: When we have uncertain times in our economy—inflation is high, markets are volatile, and insurance companies are doing well—cash value life insurance can be a safe haven for your hard-earned dollars. With the correct use of leverage and other people’s money we can accomplish much more with your same out-of-pocket budget. So, the party doesn’t have to be over and the punch bowl maybe isn’t empty just yet. It’s simply time to ask the DJ to change the song, turn it up and party on!