Not long ago I heard a sad story from a friend about his grandfather, who had passed away when my friend was a young child. As he grew older, my friend became curious about his grandfather and asked his parents and other family members, “What kind of person was he?”

“Oh yes (with a roll of the eyes), he was a piece of work,” my friend heard from many family members. “He was a womanizer, a drinker and a gambler, basically blowing the family fortune during his young lifetime.” The story of my friend’s grandfather was another instance where a considerable fortune was wasted by one individual in one generation!

Leaving a Legacy

Most of us think of “leaving a legacy” as a positive thing. In a Huffington Post article written by Joan Moran on April 27, 2015, she writes:

“The idea of leaving a legacy is the need or the desire to be remembered for what you have contributed to the world. In some cases, that contribution can be so special that the universe is unalterably changed. However, for most mere mortals walking this earth, most will leave a more modest legacy that does not necessarily change the world but does leave a lasting footprint that will be remembered by those whose lives you touched.”

I focused on the words “… a lasting footprint that will be remembered by those whose lives you touched.” Clearly, “Grandpa’s” legacy left a lasting footprint—just not in the way that he or most people would like!

According to a blog on the Human Options website entitled Legacies Happen—Don’t Leave a Bad One:

“There are two types of legacies that one can leave behind, a positive or a negative legacy. If one is not intentional about the legacy they are creating, an unintended legacy will be created whether you plan on it or not. Most people do not consciously choose between the kinds of legacy their life will leave, nor do they realize they are actively creating one with their actions of yesterday, today, and tomorrow. More often than not, legacies just happen.”

The Unintentional Legacy

Yes, in fact, often legacies are quite unintentional, and I wish that were not the case. I believe that intentionality is critical to leaving a positive legacy—leaving it to chance is for those who do not care or do not know any better. I honestly do not think that there are many people who would intentionally want to leave a negative legacy. I could be wrong.

I recently had a call from an advisor who asked how to advise a $25 million dollar net worth client who said the following when asked about his legacy planning:

“I don’t give a sh__. I had nothing; my wife had nothing—I have seen too much money do bad things to kids. We are leaving the money to the kids and they can pay the estate and other taxes out of what they get.”

The irony is that the client said that he had seen too much money do bad things to kids—the heirs—and in the very next sentence he said he is leaving the money to the kids. I believe that this story is going to end poorly, but not for the reasons you might think.

Like so many young couples, this client and his wife had nothing when they started out (generation one). And now, they are quite intentional about not planning to have their hard-earned wealth, garnered and carefully stewarded throughout their lifetime, last for generations to come. Their estate is valued at $25,000,000—a healthy sum by anyone’s standards.

Who is responsible for managing the wealth that has been created? If bad things happen to heirs who have been left “too much money,” where does the responsibility lie to minimize this possibility? This is a responsibility that many avoid… And that becomes their legacy!

Have you heard the term “shirtsleeves to shirtsleeves in three generations”? This proverbial saying from the early 20th century, often attributed to Andrew Carnegie, implies that wealth built in one generation will be squandered by the third, leaving nothing (or very little) for generation four except to start the cycle all over again (maybe).

True Wealth

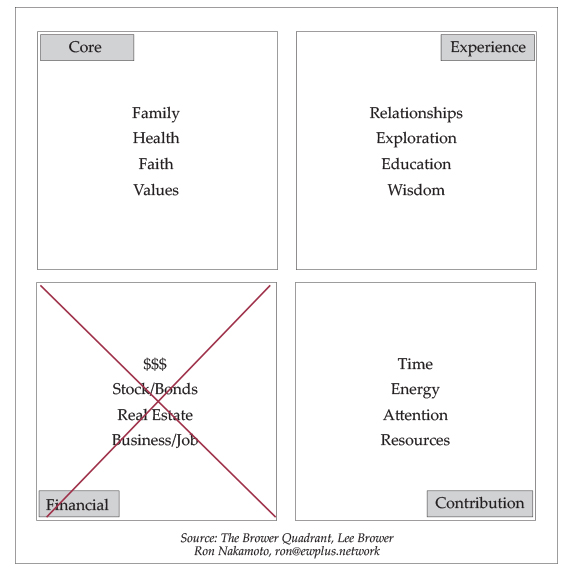

Financial wealth is only one of the four aspects of something called True Wealth. Without the other three very important parts of True Wealth, financial wealth will very likely be lost. Lee Brower, well known speaker, author, and coach on Empowered Wealth, tells a story about a woman he met on a flight between Salt Lake City and Atlanta. Following is the story from my perspective:

After the usual pleasantries on the long flight from Salt Lake City to Atlanta, the inevitable question, “So, what do you do?” came up. Lee told the woman, an accomplished businesswoman from Jackson Hole, WY, with substantial wealth, that he helped people optimize their True Wealth. Perplexed by his reply, she probed further.

Lee asked the woman, “When you think of wealth, what do you think of?” To which the woman replied “money.” Lee drew, on an airplane napkin, four quadrants with the lower left one titled “Financial” and in that box he wrote “$$$.” They continued to fill the box with other financial assets such as stocks and bonds, real estate, business interests, etc.

Then Lee asked her what she valued more than money, to which she replied, “Her family, of course.” He labeled the top left box “Core” and wrote “family” in that box. He continued to probe… “What about health, would you trade your health or your family’s health for more money?” “What about your faith or your values?”

After completing the “Core” quadrant, Lee moved on to the top right box and wrote “Experience” and asked the woman to think how she would complete this box. The words “relationships,”, “exploration,” “education” and “wisdom” came to mind.

Finally, Lee titled the last box, the lower right, as “Contribution” (think charity) and the woman completed the box with “Time, energy, attention and resources.”

When they had completed the task, Lee asked her which categories of assets she would like to see carried forward to future generations, to which she replied, “All of them,” quite emphatically and with a very eloquent explanation as to why she felt that way.

He then handed her the pen and asked her the following question, “If you had to leave one behind, which one would it be? Please cross it out.” Almost without hesitation, she crossed out “Financial.”

Next came the most important lesson of this entire conversation. Lee asked her “Why?” She explained that if her children and grandchildren were “rich” in Core, Experience and Contribution that the money would take care of itself, but if they were “bankrupt” in those areas, the money would likely be squandered in very short order.

This story clearly demonstrates that True Wealth is not just about the money. How many wealthy individuals do you know that are genuinely unhappy? Many times, the dedication to money and success is at the expense of an individual’s health, family, and relationships, and often results in illness or sometimes death, broken families, and failed friendships.

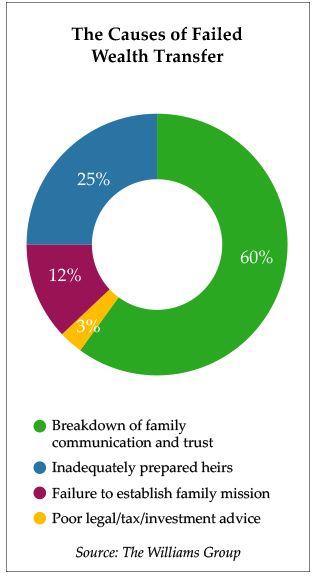

The Rates of Failure

As financial, legal, and accounting professionals who advise families on the generational transfer of wealth, commonly known as estate and/or business succession planning, our failure rate is spectacular. Only 70 percent of generational wealth transfers succeed beyond the first generation, according to The Williams Group, and beyond that the success rate is pitiful! Research from many other sources claim that the failure rate beyond generation two is 85-90 percent and beyond generation three, some claim that it is as high as a 97 percent failure rate. Let me say that a different way… As financial “guides” to our clients, we fail 97 percent of the time in helping our clients transfer wealth successfully over three generations! This is a statistic of startling proportions! As an almost 40-year professional dedicated to building, protecting, and implementing plans to transfer wealth generationally, that really bothers me. A 97 percent failure rate is unacceptable to me—what about you?

Causes of Failure

The causes of these failures are indicative of the lessons learned from the woman on the airplane story. The 25-year study by The Williams Group showed that only three percent of failures were attributable to poor legal, tax or investment advice. The other 97 percent was attributable to a breakdown of family communication and trust (60 percent), inadequately preparing heirs (25 percent), and failure to establish a family mission (12 percent). Brown Brothers Harriman & Co. published some of the research in a paper referencing The Williams Group study in 2019 titled Crossed Wires: Why Most Generational Wealth Transfers Fail. It is a wonderfully educational piece.

The most important point of this study for advisors, from my perspective, is that we all need to speak more about the “Why” of wealth—not just the “How” of transferring it to our children.

Change the Conversation!

I spend a lot of time working with financial advisors to help them guide clients toward the goal of optimizing True Wealth. Ron Nakamoto, founder of The True Wealth Mentorship Program, and friend and mentor, asks, “If we are not trying to optimize what we really care about—True Wealth—then what are we trying to do?”

He goes on to say that “after satisfying our basic needs (reference to Maslow’s Hierarchy of Needs), Money is for discovering and rediscovering happiness, fulfillment, meaning and joy in every phase of life.”

Most advisors in the estate and business succession planning world focus on the financial, process or structural conversation—investments, taxes, insurance, trusts, cost:

“Based on my assessment of your financial assets, projected estate tax exposure and liquidity needs, I would recommend an irrevocable defective trust with crummy provisions, funded with life insurance,” has been said many times by an advisor to his or her client. If I were the client, I would walk away. Sounds like a really great concept, right? It is “defective,” “irrevocable,” includes life insurance, and has “crummy” provisions! May I have two please?

I believe that an entirely different kind of conversation needs to take place first.

David York, Esq., of York, Howell, & Guymon in Utah, suggests asking different questions from the beginning that would help lead to a more intimate understanding of the client’s vision and hope for the future. For example:

- “If you could transfer all of your financial wealth without any tax or have grateful children, which would you pick?”

- “If you could average a 12 percent return on your investments or have children who are self-reliant, self-sufficient, productive, and mature, which would you pick?”

- “If you could ensure that your assets were used exactly as you outlined in your financial plan or have a family that is engaged, involved, and connected with each other 50 years from now, which would you pick?”

It is often said that clients do not care what you know until they know that you care. Change the conversation, learn to ask empowering questions, show prospective clients that you are committed to helping them optimize their True Wealth and nobody will care about fees, price, and other metrics, assuming you are competently doing your job as a financial professional with the client’s best interest at heart.

Focusing on the price of products, fees, historical returns, alpha and all the other “numbers” will ultimately lead you down a rabbit hole of commoditization. Advisors often gain a client for the same reason that they will lose a client—because of the numbers. There will always be someone who will undercut you on price or promise better returns—that is a very transient existence (and frankly, business model). What will happen when computers, through artificial intelligence, begin to take over many of the financial analytics and recommendations that are made today by humans? That is a topic for another day, but this reality is already knocking on our door.

Ask the Right Questions and Listen Carefully

Deep, personal, and intrinsic discovery that is revealed by asking the right questions and truly listening can never be replaced by artificial intelligence. Our goal as financial advisors should be to help our clients optimize multi-generational true wealth—“Living their Legacy” rather than “Leaving their Legacy.” To do that, we must understand our clients’ stories and provide the platform and the space to share these stories by asking empowering questions and creating a deep personal relationship. Only then will the financial assets that you help your clients build, manage, and protect steward the core, experience, and contribution assets for generations to come. This change in the conversation and approach will help create thriving legacies that survive the 97 percent failure rate that our profession currently experiences.