Humans Can’t Leave Well Enough Alone

Back in 2015, as I left the Victory motorcycle dealership with my brand-new Victory Magnum X1, I couldn’t wait to get it home to my garage to immediately tear it apart to “optimize” the engine (new cams, new air cleaner, new timing wheel, etc.) and replace the exhaust. My wife almost died when she walked into the garage and saw the internal organs of my brand-new bike strewn across it. Well, a week later the motorcycle ran (and sounded) great! I still have this bike and I love it!

It is human nature to not leave things well enough alone and to “optimize” everything. This human thirst for improvement and making things better is why humans are landing on Mars and dogs are not. Now, sometimes this “thirst” for optimizing can be very good—if the person doing the “optimizing” is competent—and other times, well, not so good.

That brings me to whole life insurance. With whole life, like many other things in life—whether it is IUL, cell phones or motorcycles—there are ways to optimize these products for the intended purpose. The purpose we are going to discuss today is to squeeze as much cash value out of a whole life policy as possible.

Now, many of the whole life insurance veterans that read this are certainly going to be familiar with PUAs, MECs, dividends, etc… However, what I seek to accomplish in this article is to clarify—even for the veterans—why and how various components work the way they do. If you know this material at a deeper level, you will be able to “optimize” like a world-class motorcycle mechanic. And if you choose not to do the case design yourself and instead rely on an IMO, at least you will be an educated consumer of their illustrations and know if they have done a good job with your case design. Lastly, if you like this type of material, then subscribe to www.retirement-academy.com.

A Common “Off-The-Shelf” Whole Life Design

Whole life insurance at its core is a simple concept. Whole life, in the basic sense, has three major guaranteed components to it:

- Death Benefit: As long as the client pays the premium, the death benefit is guaranteed for the “whole life”—which is usually to age 100 or age 121.

- Cash Value: Based on the guaranteed rate—usually four percent for non-par—and the internal charges in the policy, the cash value will equal the death benefit at age 100 or 121 in most cases. (Note: That is called “endowment.”)

- The Premium: In order for the carrier to guarantee a certain level of death benefit (#1) and the cash value (#2), the carrier also must be guaranteed that they will get paid a premium by the client. So, in order to get the first two guarantees, the carrier needs the third guarantee—a set premium structure. (Note: As we know however, a client can do a reduced paid-up policy in the future and also dividends can pay the premium.)

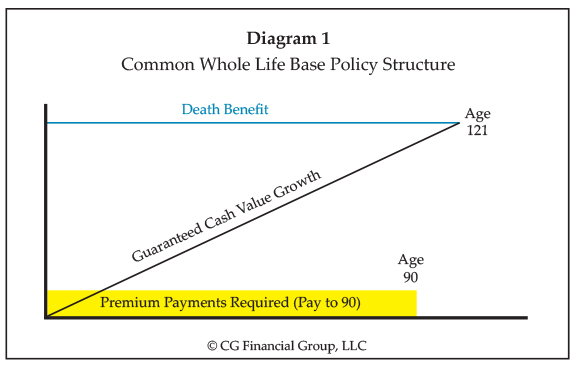

Diagram 1 shows those three components on one of my favorite whole life insurance policies by my favorite whole life company (email me if you would like details). Now, this is merely the “base policy” and we will get to the rider part in a bit.

As you can see, I outlined the “Three Guarantees” graphed out, without any numbers attached to it for simplicity. I have the guaranteed death benefit, the guaranteed cash value, and the premium that the client has to pay (in yellow). I have not included dividends in these graphs. Although dividends are very important to cash accumulation, the principal I wish to communicate in this article will hold true, with or without dividends.

Of course, this graph is not to-scale as the premium for our 45-year-old male is around 1/50th of the death benefit. However, the cash value in year one is in fact “to-scale.” That is, $0!

When I am training agents on whole life, the rhetorical question I often ask at this point is, “Is this policy optimized for cash value the way that it sits now? For our 45-year-old client, is dripping in premiums over 45 years until age 90 the optimal way? In other words, what is the ‘optimal’ way to fund a policy for cash value without taking into consideration any IRS limitations?”

The folks that know their life insurance well—and the time value of money well—will say, “The quicker, the better!” That is the correct answer!

Single Pay: Too Much of a Good Thing

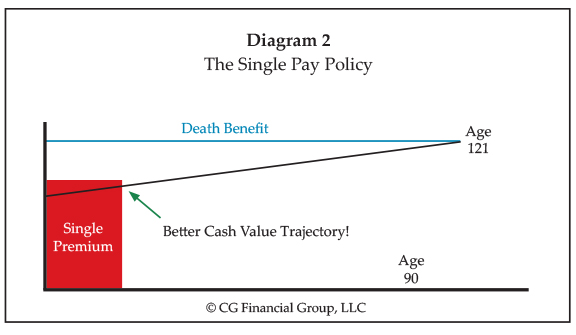

The answer to the question of “What is the optimal way of funding without considering IRS limitations?” is in fact a single premium design. Diagram 2 is representative of the same company’s single premium whole life policy. Again, the premium structure is not “to-scale” versus the death benefit but observe the cash value. Obviously, the cash value is significantly better than the previous “pay-to-90” scenario. The reasons that the single pay structure builds so much cash value is twofold: 1. More money is working in the product faster. 2. The “cost of insurance charges” are minimized because of the smaller gap between the cash value and the death benefit (Net Amount at Risk).

So, is my point going to be that “Single Pay” structures are better than the “Pay-to-90”? No! We will get there.

Although single premium life policies generally provide the quickest cash value growth, the IRS says there is such a thing as “too much of a good thing.” And single premium life (which I love) does have “too much of a good thing.” That is because you funded faster than what the IRS says you can do, at least while maintaining some of the wonderful tax advantages that life insurance typically provides. The single pay policy above is a “modified endowment contract,” meaning the cash value is taxed very much like an annuity (pre-59.5 penalties, LIFO, etc.).

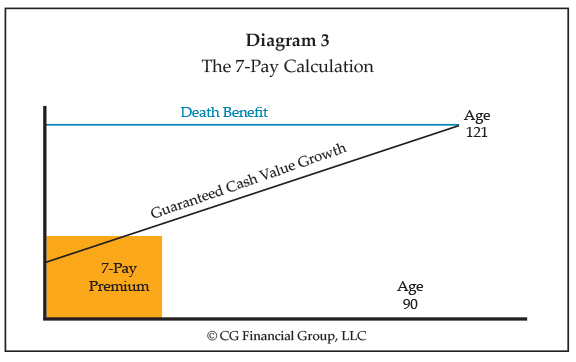

A pictorial funding example of what the IRS bases the MEC rules off of is shown in Diagram 3. That orange box is the fastest the IRS says we can fund the policy.

To the whole life “green pea,” he/she may look at the pay-to-90 product as being suboptimal because that policy must be funded low and slow. However, that “low and slow” funding structure is hard coded into the policy design.

So, what is one to do? The pay-to-90 product (Diagram 1) is funded too slow to have “optimal” cash value buildup. However, completely switching products to a single pay design (Diagram 2) would mean a MEC. Considering these policies are often bought because of the tax advantages, a MEC may not be acceptable. Is there a way to take the pay-to-90 product and optimize it where we are “effectively” funding the policy as fast as possible but not “too fast”? Yes, there is!

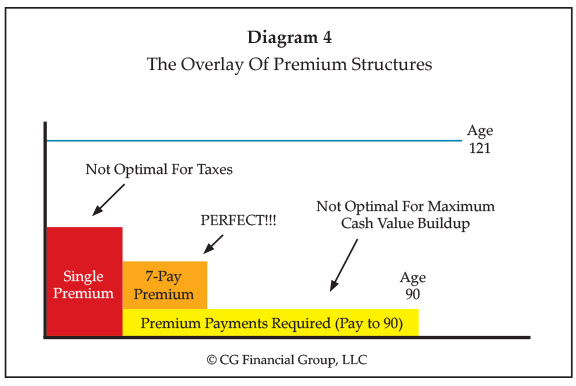

Diagram 4 is an overlay of the three premium levels we discussed in the previous graphics.

The way to “optimize” the pay-to-90 base policy is through a “Paid-Up Additions Rider.” What a paid-up additions rider does is it allows you to effectively blend out the premium structure to equal the orange box, at least per dollar of death benefit. What you are doing by adding a paid-up additions rider is you are taking the single pay funding structure that is represented in the red and you are blending that in with the yellow that is the base policy. When you blend the colors red and yellow together, you have orange… I’m color blind but that is what they tell me anyway.

With paid up additions, you are effectively making the yellow box and the red box converge to the orange box. By doing this, you have effectively funded it at the “Perfect/Optimal” level for accumulation while maintaining non-MEC status.

Again, the whole life “green pea” may view the pay-to-90 as too rigid from a funding standpoint. However, it is not “too rigid.” You can fund whole life just as optimally as you can IUL (which I love) by adding a paid-up additions rider. (Note: I am not suggesting that the client does not have to pay the premium-to-90 on the base policy. I am referring to the premium size relative to the DB.)

A Paid Up What?

Quite simply, a paid-up addition is a miniature single premium whole life policy. As a “mini whole life policy” the PUA has higher early cash values in proportion to the death benefit—versus the pay-to-90. Again, refer to the second graphic I showed you.

When you choose a PUA rider, you are electing that a chunk of your premium goes to a “Paid Up Addition.” How much of your premium gets allocated to the paid-up additions rider depends on how old the client is, health, how big the “orange box” is that the IRS holds you to, etc.

What you are doing with that paid-up additions rider is equivalent to blending in octane with the existing gasoline to get to the engine’s optimal performance level. What that “optimal level” is with life insurance is determined by the IRS (orange box).

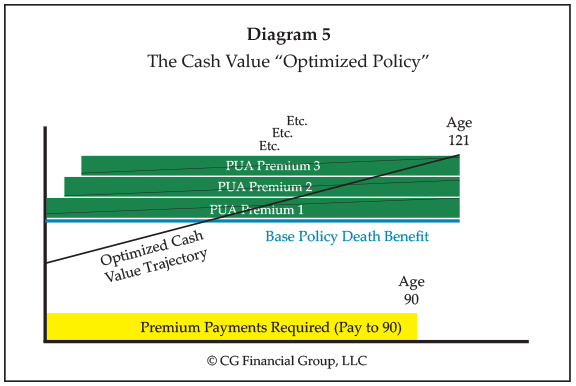

Diagram 5 shows what paid-up additions are.

As you can see, the green paid up additions are little, tiny whole life policy “slivers” stacked on top of the base policy. If you look closely, you will also see the black cash value line within each PUA that starts out low (but not $0) then equals the PUA death benefit by age 121. With each premium, a new PUA is added on top of the base policy. Again, drips of octane going into the gas tank over time. Of course, that also results in a larger death benefit as time goes by. However, in the end you have minimized the total death benefit relative to the premium to the seven pay level, which means more cash value.

Many policies are designed with 55-60 percent of the premium going to the paid-up additions rider and 45-40 percent going to the base policy premium. In many cases you can go 90 percent PUAs and 10 percent base premiums! That is where term blending comes in. Term blending basically makes the gas tank (death benefit) bigger so you can add more octane to it.

The Numbers (45-Year-Old Male, Preferred Non-Tobacco, $10,000 Premium Per-Year)

100% Base Policy

- Year 1 Death Benefit: $507,000

- Year 20 Death Benefit: $507,000

- Year 1 Guaranteed Cash Value: $0

- Year 20 Guaranteed Cash Value: $158,667

55% PUA Rider/45% Base Policy

- Year 1 Death Benefit: $246,481 (Less death benefit because single pays have less DB leverage!).

- Year 20 Death Benefit: $513,034 (Death benefit increases because of the 20 PUA “slivers”!).

- Year 1 Guaranteed Cash Value: $5,203 (More cash value because of the 60 percent PUA Octane!).

- Year 20 Guaranteed Cash Value: $213,465 (Again, higher cash value because of 20 shots of octane/PUAs).

And we didn’t even discuss dividends, dividends going to PUAs, term blending or RPUs!

“To simplify, paid up additions riders are to whole life as what an option 2/increasing death benefit is to IUL. They both work very well by increasing the premium and cash value in relation to the death benefit.”

—Charlie Gipple