“All ballplayers should quit when it starts to feel as if

all the baselines run uphill.”—Babe Ruth

I am a simple man. My exercise program for over forty years has consisted of jumping rope, doing push-ups, pull-ups, dips and stretches. I always jump rope outside, wherever I am. I throw the rope in the bag, get on a plane and go.

I do not encounter much of anything that prevents me from exercising. Snow, cold, rain, heat, wind, traffic noise, people staring, smokers using the same space outside the hotel…nothing changes what I do or how long it takes.

Now…if I was a runner, that would be another blister altogether.

According to what I have read, a person’s running performance is impacted greatly by such things as dew point, temperature, altitude, incline and even posture. Take temperature for instance. At 60 degrees, a person’s running pace suffers a two to three percent increase, meaning that someone who averages an eight-minute mile pace experiences an increase of about twelve seconds per mile. At 80 degrees, the runner’s pace slows by 12 to 15 percent, so that a mile pace becomes more like 9:06. (There is actually a temperature calculator at Runners Connect, found here: https://runnersconnect.net/training/tools/temperature-calculator/)

Or consider altitude. High altitudes decrease the amount of oxygen getting to the muscles, and for runners there is the added risk of dehydration. Table 1 is helpful.1

Point: Runners are impacted by the physics of the environment, but they can make adjustments based on measurements and calculations.

Independent financial services professionals face an ever-more challenging environment. What should they measure in order to stay on pace, or even achieve improved performance?

Critical Success Factors

It is critical that independent financial services professionals measure the right things. The reason? They only have so much time.

“Time is the scarcest resource and unless it is managed, nothing else can be managed.”2—Peter F. Drucker

To improve time efficiency and business success, begin measuring these Critical Success Factors (CSFs):

- Time invested by you per client

- Revenue per client

- The 20 percent of your clients who give you 80 percent of your revenue

- Clients who provide you with referrals

- Clients who provide repeat sales

The remainder of this article will address each of these CSFs.

CSF #1 Time Invested by You per Client

Like running the baselines in baseball, the progression from prospect to client is divisible into clear phases. There are at least these seven:

- Uncovering a potential client through Prospecting

- Pre-appointment communication

- Scheduling the first appointment

- The Fact-Finding appointment

- The Closing appointment

- Product Delivery

- Annual Review

According to H. James Harrington, “Measurement is the first step that leads to control and eventually to improvement. If you can’t measure something, you can’t understand it. If you can’t understand it, you can’t control it. If you can’t control it, you can’t improve it.”

Measure » Understanding » Control » Improvement

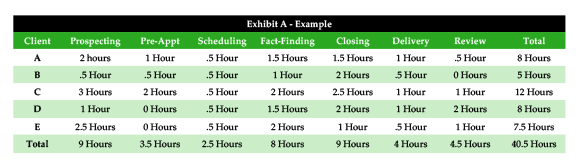

Most independent financial services professionals I have met do not measure how much time is invested in each phase of the sales cycle. Here is a tool that I hope proves helpful. (Exhibit A)

What can be learned from analyzing the results in Exhibit A?

- An average of eight hours is spent per client from prospecting through review.

- The large disparity between clients in the amount of time involved in prospecting begs investigation. What controls could be implemented to improve efficiency?

- Scheduling takes half an hour and should be delegated to an assistant.

- Is the pre-appointment process well-understood? Can the process be improved through tighter controls?

- A fair question is, “How long should product delivery take?” Is there a set process?

- Should fact-finding take nearly as long as closing? Perhaps a well-designed agenda can be applied to both kinds of appointments to make the process more efficient.

- What is the correlation between total time spent per client and the revenue earned per client?

CSF #2: Revenue per Client

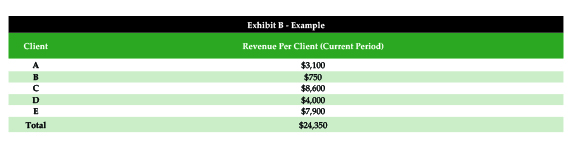

Even for the independent financial services professionals who work specific markets and have well-honed client profiles, there is always a disparity in revenue earned per client. It is important to measure revenue per client—not because it makes one client more important than another, but because it provides insight into how efficient the sales process is. First, we will look at Exhibit B.

These five clients returned an average of $4,870 in revenue. How does the revenue earned per client compare with the amount of time invested in each phase leading up to product placement?

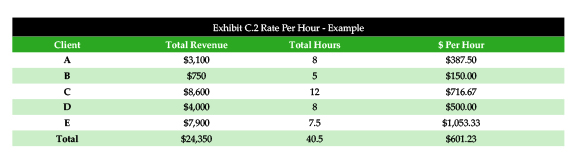

Allocating revenue to each phase in proportion (Exhibit A) to the total time spent per client is found in Exhibit C.1.

A quick look at the chart reveals that the two most revenue-intensive activities are prospecting and closing.

Revenue per client is best measured against time spent resolving the financial concerns of the client. To truly understand efficiency in the process, it is important to measure revenue in terms of income per hour. Only then can controls be applied to generate efficiency improvements.

Observations and questions:

- There are only two ways to improve revenue earned per hour:

- Keep total time static but increase total revenue.

- Keep revenue static but decrease time required to make sales.

- To earn a higher rate per hour the independent financial services professional must work with a higher revenue generating client, or, become more efficient in allocating valuable time.

- The hourly rate for an independent financial services professional does not change by the activity, but by the client.

- A fair question is, “Why should revenue from smaller income-generating clients be held hostage to the same process that the independent financial services professional uses with every client?” The process must be adjusted as soon as the revenue can be estimated.

Example: If the only activities involved in serving Client B were fact-finding and closing, then the revenue per hour would be $375, a respectable rate according to the chart.

CSF #3: 20 Percent of Clients Generate 80 Percent of Revenue

I meet with many people in our industry who feel much like the aging Babe Ruth. Every step in the process seems to be uphill. I remind them that exertion is minimized through efficiency.

Efficiency is achieved in any business by innovating to the point where the process generates a maximum return. The most important innovation is to identify the ideal prospect and design the process to best serve that type of prospect.

In our example, Client C returned the highest revenue in the measured period. However, Clients C, D and E combined for 84 percent of the total revenue in our sample of five clients. Not quite the 80/20 Rule; however, the point can be made that by knowing the commonalities and similarities of the top three revenue-producing clients we could establish the profile of the ideal prospect.

Shared Threads to Discover:

- Industry

- Occupation

- Position

- Age

- Referral Source

- Affinity Groups

- Financial Needs Resolved

- Objectives and Dreams

Armed with an understanding of the kind of client that returns the highest revenue per hour invested, the independent financial professional can begin to control the referral process and improve the kind of prospect generated. For instance, instead of asking, “Who do you know that may need my kind of services?” ask, “Do you know any computer software and systems software engineers, between 35 and 45 years old, married with children, who enjoy the outdoors, especially golfing?”

CSF #4: Clients Providing Referrals

This leads naturally to something many independent financial professionals fail to measure. Not all clients provide good referrals. The ones who do should be rewarded. In addition, there was a reason that they were willing to make introductions to new prospects. It is important to understand their motivation and learn how to control the process of asking for referrals in order to improve overall results.

The fact is, most independent financial professionals simply lack good tools and processes to ask for and collect referrals. The best tool in my experience is a simple survey presented to new clients at product placement.

Have you heard the phrase, “Happy customers make happy customers?” Clients who are satisfied with the process and the acquired products will refer more people. Therefore, whenever independent financial professionals meet or exceed the expectations of the client, and receive affirmation to that effect (perhaps through a survey), that is the exact moment when the request for referrals should be made.

CSF #5: Clients Providing Repeat Sales

F.J. Raymond said, “Next to being shot at and missed, nothing is really quite as satisfying as an income tax refund.” Similarly, better than receiving referrals from existing clients is getting repeat sales from them. Yet many independent financial professionals do not measure the frequency of this occurrence, nor the circumstances.

Repeat sales can be measured by calculating a repeat purchase rate, which is the percentage of clients who make another purchase. There is never a better time than right now to begin calculating a repeat purchase rate.

It’s equally important to measure and understand how receptive existing clients are to subsequent appointments to discuss additional financial needs. The most important factor is time between purchases.

Time between purchases shows how long a typical client goes before making a repeat purchase. This is a good metric to know because it aids in tailoring the optimal client review process to their behaviors.

Time between purchases and the repeat purchase rate are critical metrics for increasing purchase frequency among existing clients.

Practical Tips:

- Always send “Thank You” notes after each sale and each referral.

- Take great notes during every appointment and send them out in a summary email that includes “Next Steps.” These should always include the areas of planning that remain unaddressed.

- Use a survey to secure a client’s written satisfaction with the process and product.

- Send articles addressing the needs that are yet to be resolved.

- Conduct annual reviews if only via Skype or FaceTime.

Summary:

Every independent financial professional requires a defined process to turn prospects into clients. For those experiencing “uphill” climbs along each phase of the process, the answer is not to quit or slow down. The answer is to measure in order to understand, and in understanding eventually to control and improve the process.

References:

1. https://www.runtothefinish.com/sea-level-to-high-altitude-running-how-it-impacts-running/

2. “The Effective Executive,” New York: Harper Business, 2006, p 51.