Much has been written about the various generations and their buying and spending habits. From the Greatest Generation and their children, the Baby Boomers, to the Gen-Xers, the younger Gen-Yers on down to the ever growing influential force known as the Millennials.

Twenty years ago, when I joined the long term care industry on a full-time basis, life was simpler. While there were nearly ten times the number of carriers in the traditional long term care industry, most of us were captive agents—part of a particular carrier’s career shop. There may have been a few different versions of the long term care insurance policy to offer the client, but it was largely one-size-fits-all, and, because of contractual limitations, a great many of us were prompted to be myopic in our view of what to offer the client. Add to this scenario the fact that most of our clients were an average of sixty-eight years of age, retired, living on a fixed income consisting of an employer-provided pension supplemented by Social Security, with a paid off mortgage and little debt, it was easy to serve this relatively homogenous population segment.

Today our clients come from all walks of life, the various and sundry generations, with varying financial situations that demand our consideration of the financial suitability of the various products and carriers that we can now offer them. This is both the good news and the bad. As long term care advocates, it is now incumbent upon us to know a wider spectrum of product offerings ranging from the familiar traditional stand-alone long term care insurance (7702(b) tax-qualified, partnership eligible) plans to the hybrid and combination plans that bring the features and benefits of life insurance and long term care together, as well as the mixed underwriting with the contrary focuses on mortality and morbidity. Add to this the need to know the funding mechanisms permitted by applicable Federal regulatory and statutory laws, as well as the features and benefits offered by these plans, and it is far more demanding an industry for the average producer than in past years. There is no doubt that acquiring and maintaining the requisite technical acumen with which to best serve the client is also a challenge that must be met head on.

In addition to knowing the often subtle differentiators between products and the carriers offering them, the producer must now concern himself or herself with the need to market themselves. Leads are pretty much passé, and a producer has to network, market, and prospect with the intent of building a network of strategic alliances to get in front of more and more people.

What has not changed over the years is the need for producers to enhance the education and awareness of not only the general consumer, but also the strategic partners that already have the relationship with the client we are seeking. Teaching and counseling remain very successful and non-threatening means by which to help these clients and their advisors help themselves.

All of this notwithstanding, I believe that the single largest challenge rests with knowing your audience. How does a producer really know which product is going to serve the client best? Quite simply, by asking questions, listening intently and engaging in diligent fact-finding. To further facilitate this effort, I also believe that some general statements about the buying habits of the various generations can now be made based on the buying habits exhibited relative to other goods and services that they are purchasing.

To understand this concept we can apply the Law of Diffusion, but first, a bit of history. The concept of diffusion, as it was first known, was studied by the French sociologist Gabriel Tarde in the late 19th century and by German and Austrian anthropologists and geographers such as Friedrich Ratzel and Leo Frobenius.

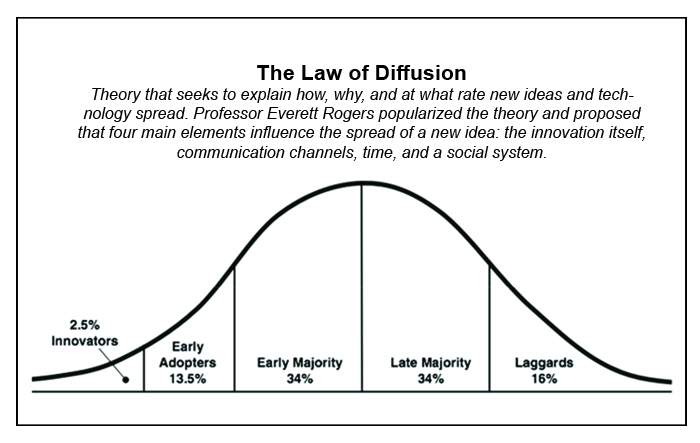

The Diffusion of Innovation (DOI) Theory was subsequently developed and refined by Everett M. Rogers in 1962. Rogers was the Distinguished Professor Emeritus in the Department of Communication and Journalism at the University of New Mexico. It remains one of the oldest social science theories. It originated in communication to explain how, over time, an idea or product gains momentum and diffuses (or spreads) through a specific population or social system.

The theory essentially seeks to explain how, why, and at what rate new ideas and technology spread. Rogers proposes that four main elements influence the spread of a new idea: The innovation itself, communication channels, time, and a social system. This process relies heavily on human capital. The innovation must be widely adopted to be deemed self-sustainable. Within the rate of adoption there is a point at which an innovation reaches critical mass and general acceptance ensues.

With most goods and services, and the industry immaterial to this discussion, the law of diffusion mandates that the buying habits of the public can be broken down in the following manner:

If we apply the Law of Diffusion to products such as laptop computers, smart phones, DVD and Blu-Ray players it becomes apparent that there are those people who will stand in line for hours (or days in some cases) to be one of the first to have the latest innovation. At the same time there are those who will stand back and watch what all of the hoopla is about, and then some of us content to be part of the late majority who will jump on the bandwagon only after all of the bugs have been worked out or our own current version of the VHS player or the flip phone suffers an ignominious death.

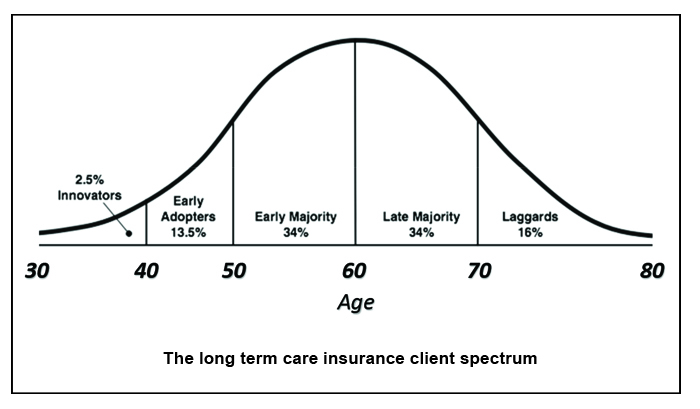

If we look at it in generic terms and apply this concept to the heretofore identified generations utilizing ten year increments to the planning and buying habits relative to long term care insurance and related products, we see that the Law of Diffusion manifests itself largely along the same lines.

I believe many will draw the conclusion that the diffusion chart for LTCI looks to be on the identical path of VHS tapes, flip phones, etc. However, while chart segment definitions could be similar they certainly are not the same. With literally millions of years of client data, LTCI has never been more pertinent and needed than it is now. So, dive deeper… What happened? It may relate to a change in the way many people now think, and their desire to live today with all the “stuff” they can have now, including things bought on credit, as well as those things they do not yet have but strongly desire. Far beyond seizing the day, these people live for the day and worry about saving for the future later. Further complicating things are the misconceptions under which these people are now laboring. While some freely admit that they should have this valuable insurance, they believe that it is too expensive to purchase and maintain. Others may falsely believe that they will not personally need it, or that there will be time to worry about it later. These falsehoods represent the very heart of the challenges we face as LTCI advocates.

Further undermining the sales of these critically needed products is the laissez-faire attitude of producers, past and present, who demean themselves to the role of order taker. They ask a couple of questions. If the clients elect to buy, great. If they don’t, see you later. To be fair, some are better than others in guiding a prospect through the sales process that allows them to feel comfortable and focused on taking care of a future long term care need now. The most powerful tool for the producer in creating an immediate desire to buy LTCI is the experience of having cared for a family member for an extended period. With this experience in the client’s background it is not uncommon for us to hear, “I don’t want my kids to go through this with me.”

We know that Millennials are saving for retirement and do not believe that Social Security will be around in the same manner that their parents can rely upon. Some are actively pursuing retirement vehicles and even borrowing from some of these plans to simultaneously attain the status of homeowners. They want what we have and they believe they can achieve it because of the accelerated nature of the world in which we live, but also that it is easier to address such future needs now while they are young, healthy, and the product is available at very modest premiums.

Their parents often find themselves as part of the sandwich generation, namely caring for aging parents (or footing the bill for their care) while also supporting children in pursuit of higher education. This oftentimes is being done completely to their own financial detriment as they sacrifice their own long term care planning needs, saddling themselves with second mortgages or borrowing from their own retirement plans.

Why talk about the Law of Diffusion? Because it is imperative to know where along the Bell Curve your client falls in terms of their general mindset toward the line of products that we have to offer them as long term care advocates.

Opinion leaders have the most influence during the evaluation stage of the innovation-decision process particularly on late adopters. In addition, opinion leaders typically have greater exposure to the mass media, greater contact with change agents, higher socioeconomic status, and are more innovative than others. They in turn utilize people like Maria Shriver, Rob Lowe, Tom Selleck and Henry Winkler who are only a handful of celebrity endorsement partners employed to talk about the virtues of products ranging from long term care insurance to home wquity conversion mortgages (reverse mortgages).

Research was done in the early 1950s at the University of Chicago attempting to assess the cost-effectiveness of broadcast advertising on the diffusion of new products and services. The findings were that opinion leadership tended to be organized into a hierarchy within a society, with each level in the hierarchy having most influence over other members in the same level and on those in the next level below it. The lowest levels were generally larger in numbers and tended to coincide with various demographic attributes that might be targeted by mass advertising. However, it found that direct word of mouth and example were far more influential than broadcast messages, which were only effective if they reinforced the direct influences. This led to the conclusion that advertising was best targeted, if possible, on those next in line to adopt, and not on those not yet reached by the chain of influence. Think about the influence of commercials aired during the Super Bowl, or the mass appeal of the iPhone and how it has changed the very fabric of our society.

Prior to the introduction of the internet, it was argued that social networks had a crucial role in the diffusion of innovation. Imagine how your own buying habits were influenced by first print ads, radio, television commercials, and now social media. I dare say that anyone contemplating a major purchase of any kind begins the buying journey by engaging in a search on the internet.

Public consequences comprise the impact of an innovation on those other than the individual, while private consequences refer to the impact directly on the individual. Public consequences usually involve collective actors, such as countries, states, organizations or social movements. Can there be any doubt that long term care can bring down the Medicaid system as it remains the number one line item in each state’s budget, most of which are drowning in red ink? Can there be any doubt that the issue of long term care for our elderly has reached a level of pandemic importance? As noted, private consequences usually involve individuals or small collective entities, such as a community or, in our industry, the family. Can there be any doubt that caregivers suffer consequences ranging from poor health and loss of socialization to lost wages, retarded employment opportunities and lack of career advancement? The innovation of long term care insurance is most assuredly concerned with the improvement of quality of life as well as the reform of organizational or social structures.

It is with this very quality of life issue that we find ourselves most concerned as we continue to seek out the methodology that will permit us to reach the public and provide them with the critical information necessary for them to reach an informed decision and to answer the call to action necessary to protect themselves and their families against the scourge of long term care.

(D. Jeffrey Levin, Jr., MBA, CLTC, also contributed to this article.)