(Reprinted from the CLTC Digest in cooperation with Certification for Long-Term Care, LLC, www.ltc-cltc.com. Email Amber Pate at apate@ltc-cltc.com for a more than 20 percent discount on CLTC training for Broker World subscribers—just mention code BWMAG.)

It’s no secret that long term care costs will continue to rise. Start with an aging population, add to that a shortage of caregivers, and sprinkle it with two and a half years of COVID and that gives you all the ingredients needed for an almost worst-case scenario for long term care costs. As a result, some states are considering ways to provide minimal long term care benefits to their citizens.

There’s an opportunity and not just for long term care insurance specialists.

Depending on how states structure the legislation, these new state benefits could have a considerable impact on the long term care insurance market for a few reasons:

- The developments will be newsworthy because anything related to an increase in taxes hits the news with a vengeance.

- As experienced in Washington State, there will be a limited number of products available.

- It creates a sense of urgency for a solution and a need for information.

Let’s begin by understanding the proposed legislation in two significant states.

Washington and California Move Forward

Washington was the first state to get serious about long term care costs. That’s partly because the state has some of the highest long term care costs in the nation, according to Genworth’s Cost of Care Survey. One of the reasons may be that it also has one of the most generous Medicaid waivers. Medicaid programs are strained in states around the country, but especially in Washington.

In 2019, the state passed a law to fund a public long term care program through a mandatory payroll tax on every W-2 employee. The only exception offered was to opt out by purchasing private long term care insurance. Things were relatively quiet until the state amended the law in April 2021 that shortened the time available to purchase private LTCI. People had about six months to find a specialist, explore available products, and apply if they had any hope of qualifying for the payroll tax exemption.

Suddenly, everyone in Washington was rushing to find a long term care insurance specialist.

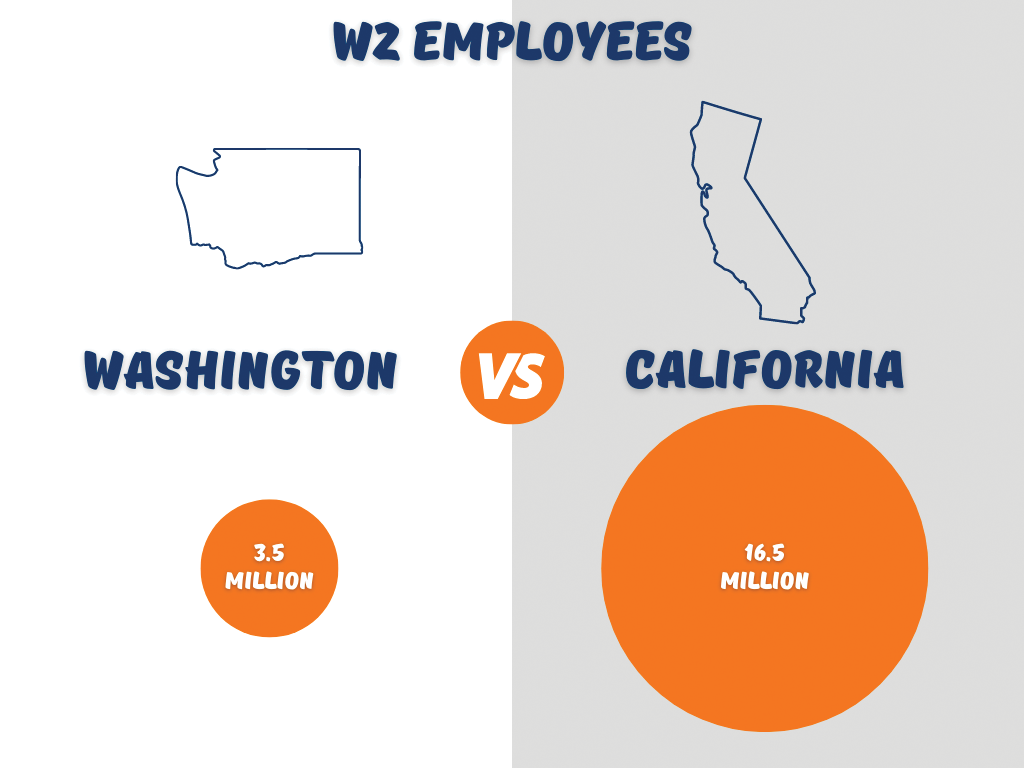

When all was said and done, of the nearly 4 million W2 employees in the state, 450,000 purchased a long term care insurance or hybrid policy with a long term care rider that qualified them to opt-out of the payroll tax in Washington. Most of them purchased during the four-month period prior to the deadline. To put that in perspective, we estimate that less than 200,000 purchased long term care insurance in the entire country during all of 2021.

At BuddyIns, we took a conservative approach in Washington and encouraged people to obtain meaningful coverage rather than just choosing something for the sake of opting out of the payroll tax. One of the biggest and most surprising outcomes was that hundreds of thousands of younger employees used this as an opportunity to purchase life insurance sooner than they might otherwise have done. The demand for both traditional LTCI and hybrid LTCI was extraordinary.

Next up is California. With approximately 16.5 million W-2 employees, the number of employees who might be suddenly interested in planning for their life or long term care needs is staggering.

California continues its push toward a payroll tax model that is similar to Washington that would fund a minimum long term care benefit. The California Long-Term Care Insurance Task Force recently provided recommendations regarding the legislation.

On October 6, 2022, the Task Force released its draft Feasibility Study for Assembly Bill 567. The study recommends options for establishing a statewide long term care insurance program. Early indications are that a proposed tax would be on earned income for W-2 employees. It is unclear yet how an exemption would work if someone owned a qualifying long term care insurance policy. However, the task force recommendation currently includes opt-out language just like Washington State. The final study is scheduled to be completed by December 31, 2022.

Notable draft program design elements per the California Long-Term Care Insurance Task Force:

- May split the cost of the payroll tax between employer and employee.

- May allow an opt-out provision or a reduction in the payroll tax if the employee has a private LTCI policy.

- No firm details on what the California payroll tax exemption will look like.

- Benefit eligibility of two of six activities of daily living (ADLs), or severe cognitive impairment.

- Benefits available outside of California with some exceptions.

- Family caregiver support includes reimbursement to informal or family caregivers subject to completion of certified caregiver training.

A Practical Sales and Marketing Strategy

California has the potential to create a flood of activity in both long term care insurance and life insurance. At BuddyIns, we’re working hard to get ahead of that challenge. Keep in mind that our goal is to encourage consumers to purchase meaningful coverage.

BuddyIns recommendations:

- Be proactive. It’s important for employees to obtain meaningful LTCI coverage and to start the process before any final state announcements. This helps to avoid the rush for long term care insurance coverage that we saw in Washington.

- Start identifying your portfolio of solutions. There may be slightly fewer group and individual products and carriers in California than in Washington because product approvals from the state take longer.

- Understand the group market. Hybrids are the most likely solution in this space. We expect the capacity of individual products in California to be limited, but group products with guaranteed issue or streamlined underwriting may have more availability.

- Be prepared to offer both life insurance and long term care insurance options. As experienced in Washington, life insurance will see a surge in sales due to younger employees needing life insurance and long term care insurance.

Create an effective outreach strategy. At BuddyIns, we will model what we did in Washington with a few modifications:

- Create an outreach process and campaign that targets employers, business owners, and higher-earning professionals who would be good candidates for coverage.

- Establish a dedicated team of long term care insurance specialists.

- Make it easy for employees to educate themselves on long term care planning and solutions using webinars, articles, and videos that plug into an employer’s established communication channels.

- Simplify the application process through technology as much as possible, including pre-underwriting, pre-quoting, and streamlining the application process.

More than a dozen states, including Minnesota, Pennsylvania, and New York, are considering this type of legislation as they seek to manage long term care costs that continue to climb. It’s an opportunity for financial planners, insurance agents, and long term care insurance specialists to lead the conversations with clients about how long term care funding should be part of a comprehensive financial strategy. Now is the time to get ahead of those conversations by building out your marketing and sales strategy.