This Summer my wife and I vacationed with dear friends in the mountains of North Carolina. Jon Kling started his life insurance and financial services career in 1972 with Equitable Life of New York. Jon was one of the first people to acquire his CFP® designation.1 He was Life and Qualifying Member of the MDRT® for many years.2 Jon and I met nearly 18 years ago and worked together for a few years. He is a wise, humble, gentle, and impactful contributor to our industry. In addition, he is a cherished friend.

Between the two of us we have something like 80 years of experience in the financial services industry. (But do not be impressed. I remember a dear friend telling me about serving in the nursery at church during the worship services: “We had 18 little people who had nearly 35 years of combined life experience, yet not one of them was potty trained!”)

While we were enjoying mountaintop views and great food, I took the opportunity to ask Jon some questions in order to capture some of his wisdom for the benefit of Broker World readers.

Me: What is your advice to independent financial professionals (IFPs) about the best thing to remember in regard to clients?

Jon: People don’t do things they don’t understand.

Me: Put meat on that. Take life insurance for example, how does an IFP best approach a client’s needs?

Jon: Life insurance falls into a broad category we call “Risk Management.” There are three components of risk and how we manage it. Risk can be reduced, avoided, or insured. To some extent, a person can control risk by altering habits or activities. What IFPs are concerned about is identifying risks that are economically devastating and very real, and in fact, inevitable. Before we can effectively discuss life insurance, we need the client to understand what risks they are comfortable accepting, avoiding, or insuring.

Me: Makes sense. What is a good way for IFPs to present the types of risks life insurance is designed to absorb?

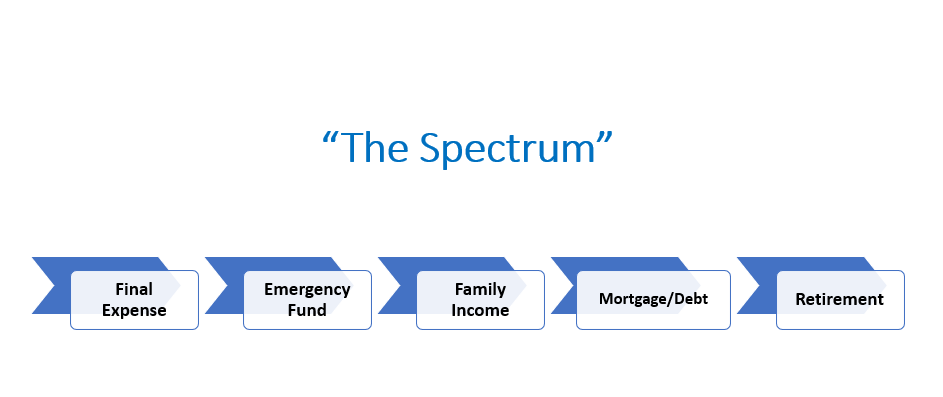

Jon: Early in my career I created something I called “The Spectrum.” It is a way of presenting the spectrum of benefits that life insurance provides for the people who own it. Think of a vertical line…the beginning and the end. All the way to the left (low end of The Spectrum) is Final Expense. Somebody else paid their way into this world so they might as well pay their own way out. Final expenses could include medical expenses from a prolonged illness, legal and accounting fees, and income and estate taxes.

Some IFPs may choose to include Emergency Fund needs in addition to final expenses. Other IFPS present the client with suitable investments that can be earmarked as emergency savings.

Moving to the right we discuss Family Income. We cannot replace the breadwinner, but we can replace the stream of income she/he provides the family.

Next on The Spectrum is Mortgage and Debt cancellation. Life insurance is an excellent way of erasing consumer debt at the breadwinner’s death and providing the surviving family members with a place to live without a mortgage.

In the middle of The Spectrum is Education Expense. Life insurance is the best plan and only self-completing time installment for providing funds for post-secondary education expenses. I did not say the best investment. An IFP can show the client an attractive alternative through systematic investments deducted from current income and channeled into an Education Fund.

All the way to the right on The Spectrum is Retirement Income. At this point the wise IFP asks a series of questions designed to discover the client’s perspectives. These questions include:

- How will you maintain your lifestyle if you live into retirement years?

- How will your spouse live post-retirement if you predecease him/her?

- At what age do you anticipate becoming financially independent?

- Will the money you expect to accumulate by retirement age last as long as you might?

- What risks have you assumed in the vehicles that you are using for sending money ahead into your retirement years?

Me: Did you ever share “The Spectrum” with other IFPs?

Jon: Yes, in fact I was asked by my core carrier to share it with their other career agent offices. Not long ago I received an email from Keith, one of the agents I taught early in his career. He wrote, “Without ‘The Spectrum’ I would never have made it 38+ years selling intangibles.”

Me: That is awesome! Hey, what other examples of good questions should an IFP use with clients?

Jon: I like these:

- Do you know the difference between transition and transaction?

- Can you tell me where your pain is?

- What do you want to accomplish?

- Have you ever wondered why some people retire with adequate income sources while others still find it necessary to work post retirement?

Me: Help me understand the first question.

Jon: A client minded IFP does not approach a client with an intention of selling something. Rather, he/she wants to help clients transition from ill-prepared to prepared, from unprotected to protected, from directionless to operating with a plan. Client minded IFPs seek to manage productive transitions for their clients, and do not focus on creating transactions.

Me: Understood. How about the fourth question?

Jon: An IFP will encounter two types of people: ‘Today’ people and ‘Tomorrow’ people. Today people plan and act today. Tomorrow people talk about planning and may, or may not, ever act. My branch manager said, “Someone who doesn’t know where they are going or how they will get there is a wandering generality.” People who retire comfortably are Today people. They recognize the importance and exercise the urgency to act now for their own future benefit. The bottom line is that IFPs need to help clients build a strategy and a plan built around their most important concerns.

Me: That is a helpful framework. What other salient advice can you offer IFPs?

Jon: I urge IFPs to tell stories when presenting potential solutions to clients. These can be stories of people who suffered upsets yet were prepared, as well as stories about people who refused to plan or prepare and whose families or employees were negatively impacted. For example, I worked with a business owner who experienced a fire in his building but, since he had no insurance, when the building was completely ruined all 17 employees lost their jobs. One person’s refusal to act impacted many other people.

Me: Many communication experts tout stories as the essential key to persuasion. What else?

Jon: Remember that we insult the intelligence of other people when we present only one solution. Respect is based on giving people options along with our recommendations. Similarly, we treat people as naïve whenever we claim that something we are offering is either cheapest or best. What people want is that which is right for them. They want to know that their individual circumstances dictated the proposed solutions.

Me: Agreed! Trust follows respect.

Jon: Simply said, the wise IFPs will sell their clients what they ask for. (Later, the IFP can sell the client what is also truly needed.)

Me: What about the issue of earning commissions or receiving fee compensation?

Jon: When an IFP presents fees to a client as part of his/her compensation, the fee itself requires that there be a discussion of value. Something not embedded in a product’s pricing (like commissions), but is paid directly by the client, demands a presentation of the value the client will receive.

Me: How important is follow-up and annual reviews?

Jon: IFPs should ask their clients, “Are your priorities static or the same as five years ago? Have they changed over the years?” The point is everything changes. Fees include the expectation of follow-up and periodic reviews. I learned that personal contact, face-to-face, or over the phone, “touch” in other words, is how to keep exceeding client expectations. Simply acknowledging birthdays and anniversaries, scheduling periodic reviews, or having any contact with clients that does not cost them more money created advocates for my work.

Me: Is there an inverse relationship between frequency of sales and length of client relationship?

Jon: Perhaps there are fewer sales as the relationship grows. But there are more ways to receive payment other than through fees or commissions. Receiving referrals is a form of payment. Brand new prospects with no connections to existing clients are harder to turn into clients. Referrals require less trust-building.

Me: One last question. As artificial intelligence expands into the financial services industry, will the IFP be eventually replaced by phones and devices?

Jon: To an extent, certainly. Anything strictly transactional is subject to being replaced by automation. In financial services, however, there remains the necessity of adding understanding to information. We want our clients to make an educated decision rather than an emotional one. Anyone today can learn all about life insurance using their phone, and discover the different product types, research the cost, compare product pricing, get quotes, and even apply online for a life insurance policy without the aid of an IFP. Stock trades can easily be done without an advisor. However, when it comes to understanding the proven techniques for applying financial principles to the vicissitudes of life, it is a rare person indeed who can navigate their way through the myriad insurance and investment opportunities without the assistance of someone who knows how.

It all comes down to the target of our attention, the object of our focus. In a letter written by the founder of an organization to its leaders, someone once wrote, “Let each of you look not only to his own interests, but also to the interests of others.”3 The successful IFP will make the clients’ interests first priority before considering how much the interaction will create in terms of income. Long-term relationships built on trust, mutual respect, and honest conversation will generate a lifetime of income for the client minded IFP.

Thank you, Jon Kling, my friend.

Footnotes:

- Certified Financial Planner Board of Standards, Inc. (CFP Board) owns a family of certification marks, including, without limitation, CFP®.

- A Registered Mark of Million Dollar Round Table®.

- https://www.biblegateway.com/passage/?search=Philippians+2%3A4&version=ESV.