Claude Thau is president of Thau Inc., and works to help build a sound long term care insurance industry. Thau wholesales long term care-related products for brokers nationwide as Marketing Manager at BackNine Insurance. In addition to his duties at BackNine, Thau consults for insurers, consulting firms, regulators, etc., creates unique software to help advisors educate clients, and does LTCI and long term care pro bono work, as LTCI’s value relies on quality long term care being available.

He also sells a little LTCI himself, as current sales experience is important to be a good wholesaler and consultant.

Thau’s LTCI experience is unusually broad and deep. After a career as an actuary, he led a major insurer’s LTCI division, which then grew five times as fast as the rest of the LTCI industry for each of three consecutive years. Since setting up Thau, Inc. in 2000, he has consulted for the Federal government’s LTCI program, chaired the Center for Long-Term Care Financing, and, since 2005, led the Milliman LTCI Survey, published annually in the July and August issues of Broker World.

A former inner-city public school teacher, Thau enjoys mentoring brokers individually to help them grow their business.

Thau can be reached by telephone at 913-707-8863. Email: claude.thau@gmail.com.

The 2025 Milliman Long Term Care Insurance Survey is the 27th consecutive annual review of stand-alone and combination long-term care insurance (LTCI) published by Broker World magazine. This comprehensive report, authored by Claude Thau, Nicole Gaspar, Chris Giese, and Matthew Epps, provides a detailed review of the individual and worksite stand-alone LTCI marketplace, sales distributions, claims, underwriting trends and available products as well as sales and commentary relative to combination LTCi. We thank insurance company staff for submitting the data and responding to questions promptly.

The report includes the following sections and exhibits:

Section IV: Claims Data Analysis – Stand-alone LTCI

Section V: Statistical Analysis of Stand-alone LTCI Sales

Section VI: Underwriting Data Analysis – Stand-alone LTCI

Stand-Alone LTCi Product Display shows financial ratings, LTCI sales and inforce policies, and generic product details

Stand-Alone LTCi Premium Display includes lifetime annual premiums by insurer for various benefit options

Stand-Alone Underwriting Class Display shows the premium adjustment (from the Premium Display) for each underwriting class and also shows the distribution of issued policies by underwriting class

Dive into the complete 2025 Milliman Long-Term Care Insurance Survey for all the data, analysis, and expert commentary. Read the Full Report

Funding long-term care (LTC) has been recognized as a huge issue for our country for a long time. Insurers, regulators, politicians, providers, educators and policy wonks continue to seek solutions.

For the purposes of this article, let’s assume that a client age 55 buys a Partnership-qualified policy with an initial monthly maximum of $4500, 3% compounding and a 3-year benefit period after a 90-service-day elimination period. Let’s assume the client begins to need qualifying care at age 85½, at which time her maximum monthly benefit would have risen to $11,044. For convenience, I’ll assume the insured/claimant is female and her life partner (if any) is male. If she uses the full amount each month, her LTCi benefits would be as follows:

Insurance Age at the Beginning of the Claim Year

Maximum Monthly Benefit

Number of Months of Benefits Paid

Reimbursement of that Year’s Expenses

Comment

85

$11,044

3

$33,132

Claim started at mid-year; 90-day EP; so only 3 months paid

86

$11,375

12

$136,500

87

$11,717

12

$140,592

88

$12,068

9

$108,612

Total

$418,836

The government benefits from that purchase of private LTCi in the following ways:

The private insurance LTCi benefit of $418,836 likely kept the client off Medicaid or contributed to the cost of Medicaid care, saving money for both the Federal government and state government.

For those kept off Medicaid, the state avoids the administrative cost of determining whether the insured is eligible for Medicaid, setting up records, and making payments.

The state and Federal governments benefit because LTC providers get the full private pay rate rather than the reduced Medicaid rate. Providers are therefore better able to provide outstanding service. The more LTCi there is, the more likely it is that innovators will want to be in the LTC industry, providing new and better services.

The additional revenue enables the provider to earn more profit and/or pay higher salaries. Thus, the provider and/or its employees pay higher income taxes to the state and Federal governments.

With LTCi, the client is likely to be less dependent on family care. Thus, family members are likely to be more productive for society and to generate more income, which results in more income taxes for state and Federal governments.

The insurance agent who sold LTCi will pay income taxes on his/her commissions to the state and Federal governments.

The insurance company will pay premium tax to the state and income tax to the Federal government.

As noted in the above bullets, the insured person benefits, the insured’s family benefits, the providers and their employees benefit, insurance brokers and their families benefit, and insurers (and their employees and shareholders) benefit, as well as the state and Federal government.

The Robert Woods Johnson Foundation (Mark Meiners, in particular) brainstormed to find a way to protect the government from the LTC costs of an aging population. What could the government do to encourage the middle class to buy more LTCi? They developed a win-win-win-win-win-win concept to make private long-term care insurance (LTCi) more affordable for the middle class: State/Carriers Public Partnerships. In a nutshell, State Partnerships are an additional back-end safety net to reward middle-class people for buying LTCi.

Four states (CA, CT, IN and NY) blazed the trail for Partnership programs in the early 1990s. However, an aide to Congressman Henry Waxman incorrectly concluded that the Partnership was a boondoggle for the rich. So, Waxman inserted into Federal legislation (OBRA, 1993) a provision prohibiting other states from developing future Partnerships. The four existing programs (including his state, CA) were grandfathered.

Twelve years later, the Deficit Reduction Act of 2005 (DRA) removed the restriction, allowing more jurisdictions to create Partnership programs. Now, 45 states have Partnership programs. (Partnership policies are not available in AK, HI, MA, MS, or VT, nor in DC, Puerto Rico or Guam. However, MA has a similar program called MassHealth Exemption.) The original, grandfathered states’ provisions differ among themselves and also differ from the provisions of the other 41 “DRA” states. There are also slight differences among the DRA states, most particularly relative to what types of compound benefit provisions can qualify for Partnership status.

Medicaid Eligibility in General

When our claimant applies to Medicaid for long-term care services, state reviewers determine whether she is eligible for Medicaid (“Medi-Cal” in California) LTC benefits. The numbers in this section of the article apply in 2025, unless otherwise indicated.

Any of her income in excess of $50/month (varies by state and may differ for home care) must be applied to the cost of care. If that income is sufficient to cover her entire cost of care, she is not eligible for Medicaid. Notes:

Her spouse is entitled to his independent income (however, if he owns an annuity in payout mode that has a certain period or death benefit, the state must be identified as a secondary beneficiary.

If her spouse is impoverished, she can transfer income to him to bring his income up to $2,555/month. He can appeal to get as much as $3,948/month, so some jurisdictions (AK, CA, DC, GA, IL, IA, LA, MS, NV, NY, OK, SC, TX, WY) automatically permit up to $3,948 instead of $2,555.

Some states have an “income cap” ($2,901/month) rather than determining whether the income is sufficient to cover the cost of care. That is, if your income exceeds $2,901/month, you are ineligible for Medicaid LTC support. People who can’t afford their LTC but who earn too much income can put excess income into a Miller Trust which pays their provider. That brings their income within limits, qualifying them for Medicaid if they and their trust were unable to pay the full cost..

In jurisdictions other than California, the care-needy individual must also apply “countable assets” in excess of $2,000 (in most states) toward the cost of care.

Non-countable assets include:

The person’s home (unless equity exceeds the amount shown below) if any of the following circumstances apply

The person may return to the home

The person’s spouse is living in the home

The person’s child under age 21 or blind or permanently & totally disabled is living in the home

A sibling is living in the home and resided in it for at least one year (while having an ownership interest) immediately before the person was admitted to the facility.

A child is living in the home and resided in home for at least two years immediately before the person’s admission and provided care which permitted the person to stay home rather than be in an institution.

The person is ineligible for Medicaid if home equity exceeds $730,000, except that the cap is $1,097,000 in CO, CT, DC, HI, MA, NJ, NY, and WA. (CA does not impose this limitation.) These limits are indexed each year.

One automobile

Household and personal belongings

Wedding and engagement rings

Income-generating property (because the income must be used to pay for care)

Burial plot and prepaid burial plans

Cash value of life insurance if, and only if, the combined death benefit under such policies is less than 1500.

Term insurance

To be clear “countable assets” include:

Cash above the limit ($2000 or so for single people; $3000 or so for a couple who both need care)

Other liquid assets: CDs, T-bills, stocks, bonds, retirement accounts (Keough*, 4.01k*, IRA*, 4.03b, etc.). Kansas is an exception in that the spouse’s §4.03B funds are exempt.

Cash Value of life insurance if the combined death benefits exceeds $1500

Vacation home

Second vehicles

Medicaid Repayment

Federal legislation (Public Law 104-191) requires that Medicaid costs be reimbursed by the recipient’s estate (“estate recovery”). When someone begins to need Medicaid support for LTC, the state may place a lien on that person’s home. When exemptions eventually wear off (e.g., children or a spouse no longer live in the home), the government collects the cost incurred by Medicaid to enable us, as a country, to provide Medicaid support to other needy individuals. Essentially, Medicaid LTC benefits are a long-term interest-free loan which is forgiven if there is no ability to repay.

The state is reimbursed for LTC services and related prescription drugs and hospital costs. The state may also recover any Medicare cost-sharing and non-LTC Medicaid costs.

Medicaid-planning attorneys help people protect assets for their beneficiaries (children or non-profits). There is an on-going ‘cat and mouse game’ as attorneys find ways to protect assets and legislators and regulators plug what they perceive to be loopholes.

Current law looks back five years (30 months in California, which also restricts estate recovery in several other ways) at any transfers that were made without adequate “consideration”. If such transfers are found, the amount of such transfer is divided by the jurisdiction-specific average daily or monthly cost of care to determine how long the person must wait to qualify for Medicaid service. The following chart show how this works, assuming that the monthly cost of care is $6,000.

How the Partnership Helps

Because you have a LTCi policy, you are unlikely to need Medicaid to pay for your LTC. The government benefits in the ways described at the beginning of this article.

The purchaser of the policy also benefits by not having to qualify for Medicaid. But what if you are very unlucky and use up your LTCi policy and still need LTC? Partnership programs provide an additional back-end protection (additional to Medicaid) under such circumstances.

You can keep $1 of your ‘nest egg’ for every $1 you get from a Partnership-qualified LTCi policy. This concept is called “Asset Disregard” and also “Asset Protection”. Thus, you can qualify for Medicaid without having to spend that money first and that money is also disregarded by the state after you die. This is also described as “Dollar-for-Dollar”. Partnership policies in New York and some Indiana Partnership policies allow all assets to be disregarded (called “Total Asset Disregard”), even beyond the benefits paid by the Partnership LTCi policy.

The Partnership allows a LTCi policy to protect your money twice.

It pays for your care, saving you money

It allows you to avoid having to spend that money “down” to qualify for Medicaid.

In the example at the beginning of the article, the insured individual collected $418,836 from the LTCi policy, which then expired. Presuming that the person continues to need care, can they qualify for Medicaid?

If their countable assets are less than or equal to $420,836 and they satisfy above-mentioned qualification requirements, they can qualify for Medicaid immediately. The $420,836 figure reflects their $418,836 expenditure plus the presumed $2,000 jurisdiction-specific exclusion.

With $450,000 of countable assets, you’d have to spend $29,164 of your own money before you might qualify for Medicaid. That wouldn’t take very long.

What if you have $1,300,000 of countable assets? Then, you must spend $879,164 in addition to the $418,836 already spent (plus the amount you spent during the elimination period or because your monthly maximum benefit was insufficient or for non-covered services) before you could qualify for Medicaid.

Spending an additional $879,164 on your care is very unlikely. So, someone with $1,300,000 of countable assets is not likely to qualify for Medicaid. Furthermore, it would take years to spend that additional $879,164. During that period of time, your assets wouldn’t deplete quickly because of your social security, pension, and investment income, RMDs, etc. The $1.3 million in assets is likely to generate $40,000 to $65,000 of income. You’d also have to spend that additional income before you could qualify for Medicaid. That’s a HUGE amount. You’d likely die before spending so much.

This example should make it clear that the Partnership is not a boondoggle for the rich. Some critics think the rich somehow know exactly how much assets they’ll have so they can buy an amount of insurance that will be exactly what they need to allow all their assets to be disregarded. (This would also require that they know when they will need care and how much it will cost.)

Of course, people can’t predict such things accurately so there is an inefficiency in their LTCi planning as they will either buy too little or too much coverage.

More fundamentally, if the rich were so clairvoyant, they would have a huge amount of LTCi that they would be very unlikely to use up. And they’d still have to contribute their income to the cost of their LTC.

Thus, even such clairvoyant people would be unable to game the system meaningfully.

Although this example assumes that the Partnership policy had been totally depleted (expired), in most jurisdictions it is possible to qualify for Medicaid while the Partnership policy is still effective. If past claims create a total Asset Disregard that exceeds countable assets and the policy benefits are insufficient to cover the full cost of care, the policyholder may be eligible for Medicaid help.

In Indiana, Partnership-qualified LTCi policies qualify for a state income tax deduction, but non-Partnership LTCi policies do not qualify for that tax deduction. In other jurisdictions and with the Federal government, tax considerations are the same for Partnership and non-Partnership policies.

Partnership policy qualification requirements

To qualify for Partnership status, the policy must be tax-qualified.

They must also have numerous consumer protections, many of which are required for tax-qualified status and/or for LTCi policies by state regulation.

Legislators have wanted to assure that LTCi coverage stays meaningful as the insured person ages. Compounding the benefit by 5% each year (before claim and while on claim) is expected to do a good job of maintaining purchasing power. Therefore, a level premium 5% compound increase feature is a “safe haven”, guaranteeing that the policy will satisfy the compounding requirement.

Compounding according to a Consumer Price Index qualifies for Partnership except in Kentucky. Level premium 3% compounding qualifies except below age 75 in Idaho.

A provision which applies such compounding to premiums as well as benefits (i.e., is not a level premium approach) qualifies for Partnership status except in KY, PA and SD.

However, future purchase options which charge an attained age price for each slice of additional coverage generally do not qualify for Partnership status.

At least twenty-nine jurisdictions allow level premium 1% compounding to qualify for Partnership status. (AL, AR, AZ, CO, FL, GA, ID, KS, LA, MD, ME, MI, MN, MT, NE, NH, NM, NV, NJ, NC, ND, OK, PA, RI, SD, TN, TX, WV, WY. This can help low-budget buyers qualify for Partnership and also enable employers to pay for a core program so their employees have Partnership-qualified coverage. A higher percentage of policies will qualify for Partnership in the future if insurers and advisors leverage these opportunities. Currently only four insurers offer 1% compounding (CareScout, LifeSecure, Mutual of Omaha and Thrivent).

The original Partnership states (CA, CT, IN, NY) and South Dakota ($100/day) have minimum size requirements for Partnership policies. The original states’ size requirements increase, typically annually. Indiana’s 2025 requirement is low ($115/day) and if the coverage pool is at least $522,686 at issue, total asset disregard applies. The higher minimum size requirements in CA, CT and NY contribute to the lack of Partnership sales in those jurisdictions.

Advisor LTCi Certification

The DRA also established a requirement that agents selling Partnership policies have suitable training. The NAIC, in drafting a model Partnership regulation, required such training to sell all LTCi policies. It wanted to encourage all LTCi salespeople to have training.

Some states adopted the DRA wording while others adopted the NAIC wording, one way in which standards vary by jurisdiction. In states with the NAIC wording, certification is also required to sell linked-benefit policies with §7702B wording. Policies with chronic illness (§101g) wording, rather than §7702B “LTCi” wording, can be sold by agents who are not certified.

Most states require 8-hour training up-front and 4-hour renewals every 2 years. Doing such training in one state is sufficient to qualify in all such states. However, some states have unique training requirements. The original 4 Partn ership states (CA, CT, IN and NY) have their own training requirements. CO requires 16-hour training up-front and 5-hour renewals for domestic agents. Several states (such as GA,MA, MN, SD, VA, VT, WI) require a one- or two-hour supplement that addresses state-specific Partnership and/or Medicaid rules. (In these states, the basic training is accepted, but the supplement is required.)

Although certification renewal every two years is standard, the measurement of the two-year period varies by jurisdiction. Many jurisdictions require that the training be done once in every renewal licensing cycle. In such states, an agent might remain qualified to sell LTCi even if they have gone nearly four years without re-certifying. (They could have taken the certification class early in one cycle, then late in the next.) However, some insurers balk at accepting applications if the agent has not taken the certification class in the two-year period prior to the date the application is signed.

Twenty-one states require that re-certification occur within two years of the previous certification. In these jurisdictions, if an agent takes the certification class earlier than necessary, they have to take every future re-certification class earlier.

An agent’s failure to maintain certification can be damaging to the agent’s clients. Insurers fear being fined if they accept an application from an agent whose certification is out-of-date. Thus, they require the agent to get certified, then take a new application. The following problems can occur:

A health change may can the applicant to no longer be insurable or to be placed in a less favorable class.

The client may have had a birthday that causes them to be too old to qualify for coverage.

An age change can cause the applicant to have a higher premium forever into the future.

A product may no longer be available or may have become less attractive.

The applicant may no longer be married or may get fewer years of tax break.

The applicant will have lower benefits at claim time because compounding will be delayed and perhaps one less future purchase option may be offered prior to claim.

Some benefits, like survivorship and sometimes return of premium on death, require that the policy have been in force for 10 years. An applicant may end up not qualifying for such a benefit because of the later date of the second app.

The client also has the nuisance of a new app.

In addition to the client problems and potential liability, delay can also be a nuisance for the broker because it can require taking the 8-hour class again (Illinois requires a new 8-hour exam if renewal occurs 12 or more months too late and Virginia requires a new 8-hour exam if renewal is just one day late.

Advisors can ask the state to put in writing that, to avoid consumer disadvantage, it is OK for the insurer to accept the application despite certification having been completed after the date of the application. With such assurance, insurers will sometimes accommodate the applicant.

Partnership Success

Prior to the Deficit Reduction Act, Partnerships for long-term care insurance were available only in CA, CT, IN, and NY. Their success seems clear because 13.2% of the individual LTCi policies in the USA were sold in those 4 Partnership states in 1993, before the Partnerships were effective, but 19.4% of the policies in 2007 (and 24.1% of the premium) were sold in those states. What would have caused that increased market share other than the Partnerships?

However, since then, LTCi has become much more expensive. The Partnership target market has a much tougher time trying to afford coverage.

The table below shows, for each jurisdiction, the percentage of 2024 sales that qualified for the Partnership and the average premium per insured (for all policies and just for Partnership policies; these average premiums are distorted by including FPOs and 100% of single premiums).

Traditionally, north central states such as Minnesota, North Dakota, and Wisconsin have had a high percentage of policies qualify for Partnership. The restrictive requirements of the four original Partnership states has resulted in no Partnership sales being reported in 2024 in California, Connecti

Jurisdiction

% qualified

Average Premium including FPOs and full Single Premium

For Partnership

Total

Partnership

Alabama

20.1%

$5,139.29

$3,829.03

Alaska

0.0%

$5,008.13

Arizona

39.1%

$4,916.26

$6,288.26

Arkansas

19.5%

$4,514.11

$5,707.61

California

0.0%

$5,085.68

Colorado

32.7%

$5,192.62

$5,110.70

Connecticut

0.0%

$4,942.90

District of Columbia

0.0%

$4,826.74

Delaware

17.2%

$4,254.30

$4,464.19

Florida

20.0%

$3,800.33

$3,969.00

Georgia

43.5%

$5,010.28

$5,896.17

Hawaii

0.0%

$3,542.03

Idaho

27.3%

$5,177.34

$5,543.61

Illinois

25.7%

$6,026.78

$5,402.07

Indiana

2.2%

$4,361.52

$4,345.00

Iowa

48.7%

$4,619.13

$5,781.95

Kansas

35.3%

$3,677.07

$4,739.14

Kentucky

20.2%

$3,668.27

$6,870.04

Louisiana

31.3%

$4,581.23

$6,733.14

Maine

13.2%

$4,140.79

$4,881.78

Maryland

29.5%

$5,079.68

$4,002.57

Massachusetts

0.0%

$6,509.52

Michigan

23.5%

$3,615.51

$3,716.26

Minnesota

62.2%

$4,453.43

$5,257.07

Mississippi

0.0%

$5,973.75

Missouri

19.6%

$4,135.87

$5,537.02

Montana

31.5%

$3,763.96

$4,294.08

Nebraska

47.9%

$4,596.42

$6,018.41

Nevada

44.7%

$3,873.18

$4,236.62

New Hampshire

24.4%

$4,479.23

$3,690.45

New Jersey

15.4%

$3,958.01

$5,343.11

New Mexico

12.8%

$6,205.18

$4,358.84

New York

0.0%

$6,025.40

North Carolina

37.6%

$4,326.59

$6,417.17

North Dakota

62.0%

$4,296.13

$4,653.20

Ohio

55.1%

$4,949.35

$6,113.57

Oklahoma

35.3%

$4,638.05

$6,987.64

Oregon

51.8%

$6,650.21

$8,533.18

Pennsylvania

19.6%

$4,802.45

$4,534.44

Puerto Rico

0.0%

$874.83

Rhode Island

28.2%

$4,361.46

$6,855.65

South Carolina

35.3%

$4,141.82

$5,935.71

South Dakota

51.1%

$6,506.58

$7,089.57

Tennessee

38.6%

$4,700.81

$6,851.20

Texas

19.7%

$3,888.70

$3,912.12

Utah

0.0%

$5,462.42

Vermont

0.0%

$5,381.62

Virginia

30.6%

$4,568.10

$6,437.06

Washington

27.2%

$4,134.90

$4,578.07

West Virginia

8.8%

$2,853.16

$3,063.89

Wisconsin

62.8%

$5,023.45

$5,697.89

Wyoming

30.8%

$5,350.37

$10,871.57

Total

26.9%

$4,654.18

$5,499.52

Participants reported Partnership sales in 41 states, all Partnership-authorized states except CA, CT and NY. Only one insurer sells Partnership in IN; that insurer issued Partnership policies in 41 states. One insurer issues no Partnership policies.

Overall, 26.9% of policies qualified for Partnership, but 33.5% of policies qualified for Partnership in the DRA states (38.9% excluding Bankers’ Fundamental Plus product). Excluding Bankers’ Fundamental Plus product, 80% of Minnesota’s policies and 74% of Wisconsin’s policies qualified for Partnership, but 5 DRA states had less than 20% qualify.

Partnership programs could be more effective if:

Advisors offer small maximum monthly benefits more frequently to middle-income individuals and stress the importance of benefit increases to maintain LTCI purchasing power and qualify for Partnership asset disregard. For example, a $1,500 initial maximum monthly benefit covers about 1.5 hours of home care per day and, with compound benefit increases, may maintain buying power. Many middle-income individuals would like LTCI to help them stay at home while not “burning out” family caregivers and could be motivated further by Partnership asset disregard. (This approach does not work in CA, CT, IN and NY because of their high Partnership minimum daily benefit requirements.)

The four original Partnership states migrate to DRA rules. That would make it easier for policies to qualify for the Partnership in those four states and would create more uniformity. Uniformity would simplify the process for agents and general agents and encourage Partnership sales in multi-jurisdiction employer sales.

AK, HI, MA, MS, VT, and DC adopt Partnership programs.

Programs that privately finance direct mail educational LTCI content from public agencies were adopted more broadly.

Financial advisors press reluctant insurers to certify their products and offer 1% compounding.

More financial advisors were LTCI-certified. Some people argue that certification requirements should be loosened. Certainly re-certification rules could be improved in some jurisdictions.

Linked-benefit products became Partnership-qualified.

All Partnership jurisdictions honored asset disregard accumulated in other jurisdictions. The DRA established reciprocity unless a state opted out and permits states to opt out in the future even if they recognize reciprocity today. Except for California and for New York relative to policies not approved in NY, states with Partnership programs currently grant reciprocity to asset disregard from policies issued in other jurisdictions.

Reciprocity in agent certification was more common. California does not recognize out-of-state certification.

All states guaranteed asset disregard. Some states retain the right to deny asset disregard at any time in the future, including disavowing past asset disregard accumulations. I am not aware that such uncertainty has harmed the market, but ‘bait and switch’ practices are unbecoming. Ironically, a state which guarantees asset disregard requires that applicants be notified that asset disregard is not guaranteed. (This happened because they copied the disclosure requirement of a state that does not guarantee asset disregard.)

They are your clients, and they will have questions. Naturally, your inclination is to help—even if they didn’t purchase the long-term care policy from you. Instead, first stop. Stop, to avoid overcommitting. To be clear, the point of stopping is not for clients to delay submitting their claim. The point is to be thoughtful and prudent before acting. Has your client even reviewed the policy before calling in the claim? Will you be assisting them? The goal is to produce a good experience for them and to avoid the hassle and stress associated with a delayed or denied claim.

If the insured or family member reaches out telling you they think it’s time to go on claim, listen. Listen and empathize as they describe their challenges and the strain on their family. Then, take a moment to praise the decision to purchase the policy to begin with. They already have a great head start compared to most Americans. Even so, it’s important to convey the process they are about to embark on.

Understanding Eligibility A long-term care insurance (LTCi) policy is catastrophic coverage, comparable to homeowner’s insurance. The homeowner’s policy kicks in when the house is destroyed by a fire or tornado. But it won’t pay for home maintenance and repairs.

Similarly, LTCi is not designed to help with all the afflictions of growing old. Generally, insureds need support before they can satisfy the criteria to receive LTCi benefits from their policy. They will likely need help with Instrumental Activities of Daily Living (IADLs) like food preparation, grocery shopping, housekeeping, managing medications, managing finances, paying bills, yard work, or transportation.

When they think they are eligible to be on claim, a licensed health care practitioner (doctor, nurse, social worker) will assess whether they satisfy the eligibility criteria (i.e. triggers). Generally, this is (1) having a severe cognitive impairment or (2) needing help, from another person, with at least 2 out of 6 activities of daily living (ADLs) like bathing, dressing, toileting, transferring (in and out of bed or chair), eating, and continence. Once the criteria have been met, the LTCi policy can cover IADLs as well.

Note: Most policies consider ADLs to include standby assistance as well as hands-on assistance. Also, older LTCi policies issued before 1993, may have language requiring hospitalization or nursing home stay before benefit eligibility.

Common Reasons for LTC Claims Denials:

Insufficient evidence or documentation to satisfy eligibility

Insufficient documentation for the Plan of Care

Unapproved or unlicensed care provider

Services not covered

Elimination period not met

Policy lapsed

Conflicting medical opinions

Excluded conditions (like substance abuse or self-inflicted injuries)

Manage Expectations–The Process Claims can take eight-plus weeks to get approved when assisted by third parties like: Amada Senior Care, Jahnke Consulting, or Thalheimer Insurance. For unassisted claims it could be eight to 12 weeks or longer. Consequently, with a waiting period like 90 days, the family can expect to pay out of pocket for care for five to six -plus months prior to receiving a payment from the insurer.

Note: Sometimes families hold invoices until the claim decision is finalized. But they should submit them right away so they can be paid when the claim is approved. In fact, one can contact the insurer even before they receive an invoice—like to obtain provider approval. (Typically, the elimination or waiting period begins from the first date of qualified care service.

Setting proper expectations can avoid turmoil and stress. Insurers need adequate documentation supporting the insured’s eligibility and plan of care. Unfortunately, the psychology of getting old is that insureds are likely to overstate their abilities at doctors’ appointments. They may conceal their declining physical or mental condition due to embarrassment and/or fear of losing their independence.

For example, during an assessment, one claimant denied problems with continence while he was literally wearing Depends. Insureds are inclined to talk about their best days but perhaps they should describe their worst too. Consider “sundowning” with dementia (confusion, agitation, pacing, aggression) which gets worse late in the afternoon or evening. Knowing this, should one schedule the cognitive assessment in the morning when they are at their best?

Unfortunately, sometimes doctors’ notes are written optimistically to protect patients’ feelings—thereby complicating benefit eligibility. Doctors today generally do not supply the same amount of detail they did years ago. They may click a digital option from a selection describing the patient’s condition vs. a personalized written narrative.

The family should review the insured’s medical records and encourage doctors to be forthcoming, detailed, and prompt. Additionally, consider that billing specialists are motivated to submit paperwork, so doctors get paid—whereas LTC claims requests may be a lower priority.

The insured/families are responsible for assembling records from physicians and caregivers and submitting them to the insurer. Insurers have very specific criteria (fax, mail, portal, email) which seniors may find challenging.

Important: while insureds are known to overstate their abilities—sometimes they or their families exaggerate or misrepresent their condition. This confuses and delays benefit eligibility. Therefore, be up-front and honest—since insurers may elect to engage an investigator for questionable claims.

Manage Expectations—Your Engagement Your clients should read their LTCi policy. Afterwards, they should read it again. Reviewing the contract, obtaining medical and care provider records along with communicating with the insurer is an arduous task. Although well-intentioned, you likely won’t have the time or expertise to do this. So, don’t get in over your head and commit to assisting when you are unable to. However, you can arm clients with basic knowledge to help them manage the claim or refer them to a LTC claims consultant who will charge a fee for their professional services.

Let them know up-front if you will be engaged or not. The very last thing you want to do is antagonize them. Appropriately managing expectations can leave a good impression on your clients and their family.

Client Considerations

Do Not let the policy lapse.

Urge families to sign up for third party notification to prevent lapses.

If the policy has lapsed due to cognitive impairment or functional incapacity, quickly explore if the policy can be reinstated.

Review coverage parameters. Get a copy of the policy if necessary.

Did the client make a change to reduce their benefits such as during a rate increase or otherwise?

Encourage families to select one point person to interact with the insurer.

Consider setting up Power of Attorney (POA). Obtain necessary paperwork like HIPAA release forms to allow the insurer to communicate with physicians and caregivers.

Ask about the insurer’s claims process. Find out how providers are assessed and get suggestions about care coordinators. Ask about discounts for LTC services.

Ensure the trusted family member/POA is present each time the insured interacts with the insurer.

Seniors on their own may get confused and not disclose sensitive care needs which harms their eligibility for benefits.

Be prepared to supply the following (a) a copy of the license for the home health care provider or facility (b) the health care practitioners Plan of Care (c) the care provider’s daily caregiving notes (d) invoices for care services and (e) a list of the physicians and medications.

Policy Provisions to Review

What criteria trigger benefit eligibility?

How long is the Waiting/Elimination Period? How exactly is it counted?

What is the Maximum Daily/Monthly Benefit?

Will the maximum benefit increase annually?

What Is the Lifetime Maximum Benefit Amount?

What types of care services are covered and how are they defined?

Does the Benefit Amount, Elimination Period, or Benefit Period vary for Home Health Care v. Assisted Living Facility v. Nursing Home?

Is the policy Reimbursement (most common) or Indemnity?

Is there Joint coverage?

What riders are included in the policy?

Is there Waiver of Premium and when does it begin?

What exclusions apply?

If you want to learn more about LTC definitions you can refer to CLTC: A_Guide_For_Your_LTC_Insurance_Policy.pdf (certitrek.com)

Good News—Silver Lining While LTCi often gets a bad rap as having an onerous claims process, we should recognize insurers have the responsibility to avoid paying ineligible claims. They need adequate documentation to justify payment. The more prepared your clients are, the more pleasant their claims experience will be.

It’s human nature when we receive good service, like 10 times in a row, that we simply carry on silently. But if on the 11th visit, we have a bad experience, then it’s the one time we talk about. Now imagine if you have a negative experience with a claim while under the pain and duress of a loved one’s decline. It is magnified—unbelievably so.

We’ve all heard of heart-breaking LTC claims examples. But, in 2023 alone, $14+ billion of traditional LTCi claims were paid. We don’t hear enough about these heart-warming testimonials where they were rescued by their policy. Not just the insured, but their spouses and children too—who now can spend more quality time with them vs. caregiving. Perhaps it’s our own fault, as an industry. We fail to toot our own horn, particularly in November, during Long-Term Care Awareness Month.

In the U.S., there are over 10,000 people turning 65 every day. It’s been dubbed the silver tsunami. So, get ready. More and more of your clients will be contacting you about their LTCi policy. Be prepared to push the brakes and stop. Congratulate them on their purchase. Help manage expectations. Arm them with the knowledge that it will likely be a lengthy process—but to hang on and be patient. Then outline your ability to assist (or not), provide pointers to review their policy, or refer them to a third party.

The good news is, claim time is the time when the insurer delivers on their promise and it’s the time for you to serve the next generation, potentially your future clients.

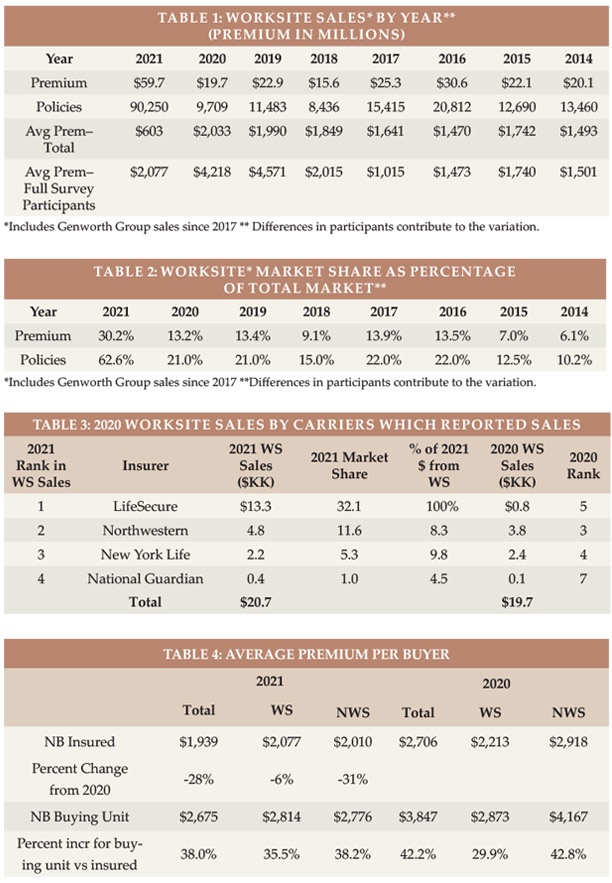

The 2024 Milliman Long Term Care Insurance Survey, published in the July/August issue of Broker World magazine, was the 26th consecutive annual review of long-term care insurance (LTCI) published by Broker World magazine. It analyzed product sales, reported sales distributions, and detailed insurer and product characteristics.

From 2006-2009, Broker World magazine published separate group LTCI surveys, but discontinued those surveys when the availability of group LTCI policies shrank. In 2011, Broker World magazine began this annual analysis of worksite (“WS”) sales to complement the overall market analysis.

The WS market consists of individual policies and group certificates (“policies” comprise both henceforth) sold with employer support, such as permitting on-site solicitation and/or payroll deduction. If a business owner buys a policy for herself and pays for it through her business, participants likely would not report her policy as a WS policy because it was not part of a WS group. If an employer sponsors LTC/LTCI educational meetings, with employees pursuing interest in LTCI off-site, sales would likely not be reported as WS sales.

We limit our analysis to US sales and exclude “combination” products, except where specifically indicated. (Combination products pay meaningful life insurance, annuity, or disability income benefits in addition to LTCI.)

The bulk of worksite sales that cover activities of daily living (ADLs) or cognitive impairment do not qualify as LTCI under section 7702(B) and are not covered in this survey (except as specifically mentioned).

In addition to “WS” to represent worksite sales, we use “NWS” to represent individual (non-worksite) sales and “Total” to refer to WS and NWS sales combined.

About the Survey Participants: Seven insurers (Bankers Life, Knights of Columbus, Mutual of Omaha, National Guardian Life, New York Life, Northwestern, and Thrivent, referred to as “Participants” herein) contribute broadly to stand-alone sales distributions reported herein. Total 2023 sales data includes one additional contributor (LifeSecure) and 2023 inforce data includes two additional contributors (LifeSecure and CalPERS).

Our stand-alone LTCI WS sales and statistical distributions come from participants National Guardian Life, New York Life, and Northwestern; WS sales data from contributor LifeSecure; and inforce business from those insurers plus Mutual of Omaha.

The following ten insurers participated in our combination sales data: AFLAC, John Hancock, Mass Mutual, New York Life, Nationwide, Northwestern Mutual (Northwestern), OneAmerica, Securian, Trustmark and United of Omaha.

Comparisons of sales distributions: WS statistical distributions can vary significantly from year-to-year if particular segments of the WS market are over- or under-represented (the three segments are core, carve-out, and voluntary, described later). Carriers that provided our 2023 distributions had an average worksite annual premium of $2,271, excluding FPOs and single premium policies, whereas insurers that provided sales, but not distributions, had an average annual worksite premium of $1,476. That discrepancy, consistent with the past several years, suggests that our worksite sales distributions are dominated by carve-out executive sales.

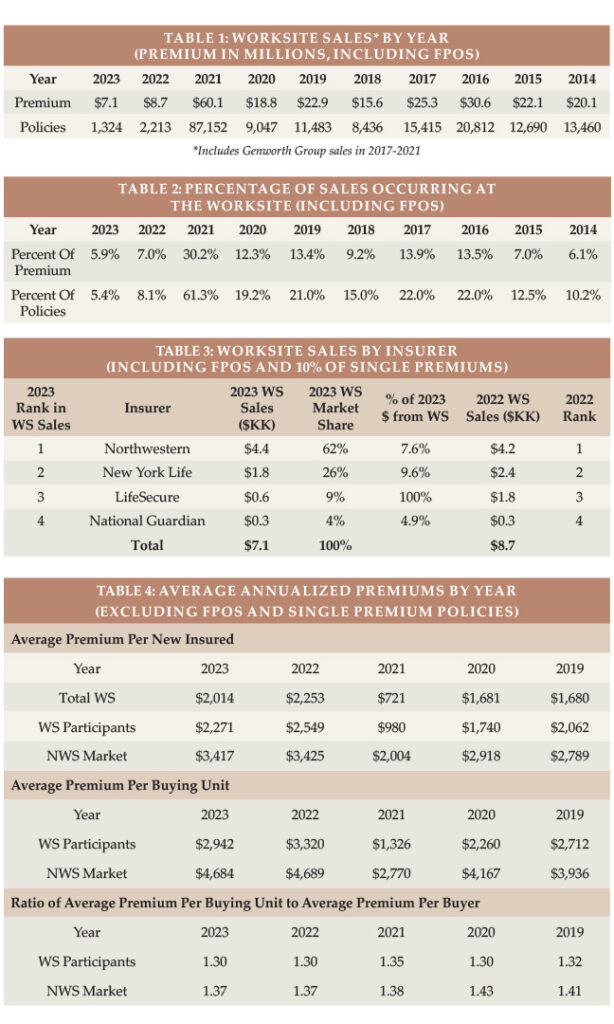

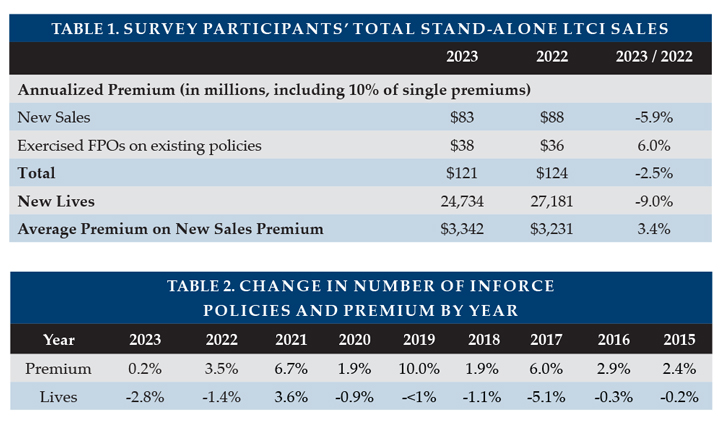

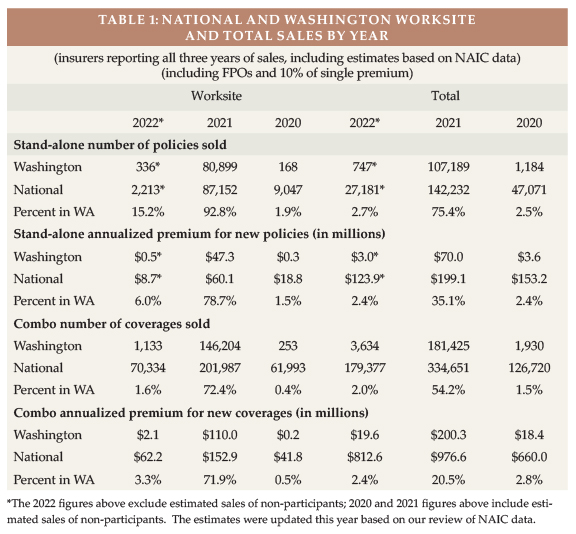

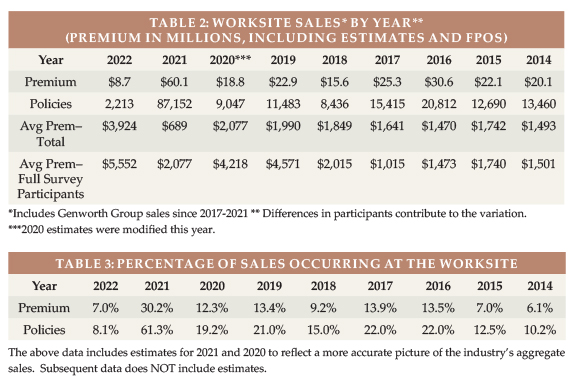

Highlights from This Year’s Survey Table 1 shows WS new sales by year (for 2023: 1,324 lives, down 40 percent from 2022, and $7.1 million of annualized premium, including FPOs, down 18 percent) and Table 2 shows the percentage of Total sales that were made in the WS by year (5.4 percent of lives and 5.9 percent of premium in 2023). The WS stand-alone LTCI market has reduced substantially since the major writer discontinued sales in 2021 and is a decreasing percentage of the Total market. As discussed previously, some sales that are worksite-related may not be classified as WS sales.

Over at least a 20-year period prior to 2022, the fewest stand-alone worksite LTCI policies sold in a year was 8,436 policies (2018). Worksite sales with coverage for ADL-deficiency and cognitive impairment have shifted to combination policies, most of which do not qualify as LTCI under section 7702(B). Only two of the carriers in that market reported combo worksite sales for our survey, but those two carriers sold roughly 80,000 such worksite policies in 2023 (up 16 percent from 2022) compared to the industry’s 1,324 stand-alone LTCI WS sales. Among our combination contributors, WS sales accounted for 36.3 percent of reported lives and 9.9 percent of annualized premium. We have a good-sized sample of combination insurers, but a lower percentage of industry sales than in the stand-alone market.

MARKET PERSPECTIVE There are three segments of the WS market. A single WS case may involve different segments for different employee classes.

In “core” (“core/buy-up”) programs, employers pay for a small amount of coverage for generally a large number of employees. Employees can buy more coverage. “Core” programs generally have low average ages, short benefit periods, low daily maximum benefits and a small percentage of spouses insured.

In “carve-out” programs, employers pay for robust coverage for key executives and usually their spouses. Generally, executives can buy more coverage for themselves or spouses. Compared to “core” programs, a higher percentage of insureds are married and more spouses buy coverage. Because the age distribution is older, the maximum monthly benefit is higher, and the benefit period is longer, the average premium is much higher than for core programs.

In “voluntary” programs, employers pay none of the cost. The typical coverage is more robust than “core” programs, but less robust than “carve-out” programs. Voluntary programs tend to be most weighted toward female purchasers.

Because of tax savings, small executive carve-out issue dates may have effective dates weighted toward the end of the year. On the other hand, large voluntary cases are more likely to have fall enrollments with January 1 effective dates.

National Guardian, New York Life, and Northwestern write mostly executive carve-out programs and are the only insurers that provided statistical worksite distributions; therefore, our distributions are heavily weighted to the executive carve-out market.

Carrier and product shift: Voluntary WS programs have gravitated toward combination products that include life insurance because insurers, brokers, employers, and employees tend to favor combination products.

Insurers’ pricing, underwriting, and distribution considerations favor combination products. Prior to 2012, insurers used unisex “street” pricing and typically discounted “street” prices by five percent for the worksite. Gender-distinct “street” pricing made WS pricing more complicated for insurers who believe unisex pricing is preferable in the WS due to Title VII of the 1964 Civil Rights Act. Pricing, state filing, administration, and illustration work increased when insurers could no longer simply reduce “street” prices by five percent.

Because women have higher expected future claims, unisex pricing saves women money compared to gender-distinct NWS pricing. On the other hand, men pay much more (e.g., roughly 50 percent more for some insurers) with unisex pricing than with gender-distinct pricing, possibly complicating WS sales and raising insurer concerns about gender anti-selection (a higher percentage of females in WS cases). Insurers also fear health anti-selection (unhealthy people being over-represented among buyers), as stand-alone LTCI does not have a high voluntary participation rate. Therefore, WS stand-alone LTCI programs have limited, if any, underwriting (health) concessions.

Combination products with LTC-related benefits are less affected by unisex pricing as females pay less for the death benefit but more for the LTCI (or chronic illness) benefit. Furthermore, products with chronic illness riders do not require salespeople to be LTCI-certified, which provides insurers access to a broader distribution system than with stand-alone LTCI. As combination life programs have higher penetration rates, insurers often offer “guaranteed issue,” coverage based on the number of employees and participation rates.

From the broker, employer, and employee perspective, simplicity is very attractive. “Guaranteed issue,” along with typically fewer age restrictions than for unisex stand-alone LTCI pricing, allows any employee to be covered and makes enrollment easier and faster, like other employee benefit offerings.

Additionally, combination products’ death benefit avoids the “use it or lose it” issue and is more meaningful for young and less affluent people than is LTCI. Such products can allow 100 to 300 percent of the death benefit to be used for help with ADLs or cognitive impairment, typically using up to four percent of the death benefit each month. Alternatively, they can allow 100 to 200 percent of the death benefit (at a rate of four percent per month) but restore the death benefit each month when a LTCI claim is processed. With “restoration”, beneficiaries will receive the full death benefit regardless of how much LTCI benefit was received. Most of these provisions qualify as “chronic illness” under IRS §101(g); others qualify as “long-term care insurance” under IRS §7702(B). The chronic illness products do not require broker LTCI certification, which makes those products “simpler” than §7702(B) products.

While stand-alone (and linked-benefit) individual LTCI products generally offer annually-increasing coverage to try to maintain purchasing power in the face of inflationary increases in the costs to provide long-term care, WS combination products have a fixed benefit. For example, if a 30-year-old employee buys a $100,000 death benefit, she will have a $4,000 monthly benefit for chronic illness (assuming the benefit features described above). That $4,000 benefit would have much more purchasing power if she needs care in the next few years than if she needs care 50 years from now.

Stand-alone LTCI is still popular in executive carve-out programs. Executives can more easily afford to continue coverage after termination of employment, hence appreciate the value of compound benefit increases. Income tax advantages encourage employer-paid coverage, particularly for executives, and tax advantages may increase in the future if income tax rates rise or if such LTCI coverage permits opting out of future state LTCI programs. Because of tax advantages and employer premium payment, higher unisex prices for men are less of an issue in the executive carve-out market. Two stand-alone LTCI insurers offer unisex pricing with as few as 2 to 5 (varies by jurisdiction) employees buying, an approach that caters to this market.

State-run LTCI programs: We discussed state-run LTCI programs in the July/August issue and prior years’ articles. Washington state’s “Washington Cares Fund” (WCF) stimulated tremendous market demand in the state of Washington, causing WS sales and distributions to vary greatly from historical trends in 2021 and 2022. However, the Washington Cares Fund and other potential state-run programs appear to have had little impact on 2023 WS sales.

Availability of coverage: As few people younger than age 40 buy stand-alone LTCI, some insurers have raised their minimum issue age to avoid anti-selection and to reduce exposure to extremely long claims. One insurer limits the maximum age to 69. Such age restrictions can discourage employers from introducing a program (even a carve-out program if they have executives or spouses too young to be covered).

Younger employees who are ineligible for coverage may still benefit from a program because their elders are often eligible for WS stand-alone LTCI programs. However, one contributor no longer offers WS LTCI to non-household relatives. Reduced availability for such relatives does not have much impact on sales, because typically 99 percent of worksite sales are to employees or their partners. Thus, even if a program is available to elder relatives, it is not likely to meaningfully address the negative impact of employees being caregivers.

With increased remote work, more employers have employees stretched across multiple jurisdictions. Eligible non-household relatives might live anywhere. However, insurers may not offer a product in jurisdictions with difficult laws, regulations, or practices, such as slow policy form approval. It can be hard to find a product which can cover everyone unless LTCI is sold on a group policy form and the employer does not have individuals in extra-territorial states. Combination products also run into jurisdictional issues because some jurisdictions do not allow LTCI benefits to exceed the death benefit and/or do not allow death benefit restoration.

Increasing hurdles for coverage have discouraged brokers as well as insurers. Some employee benefit brokers are reluctant to embrace stand-alone LTCI because of declinations, the enrollment effort compared to typical group coverages, certification requirements, their personal lack of expertise, etc. These issues could be mitigated by LTCI specialists forming relationships with employee benefit brokers.

Support for Employees who are Caregivers: Various programs offer LTC-related services to employees and their families. Regardless of whether the employee is insured or the relative is insurable, they may be able to access information, advice, services, and products that make caregiving more efficient, more effective, safer, and less expensive. Enabling employees and their families to have better LTC experiences and to use more (not necessarily 100 percent) commercial care should boost productivity at work. Some of these programs are packaged with WS LTCI.

STATISTICAL ANALYSIS In addition to fundamental industry changes, distributions may vary significantly from year to year due to different participants, shifting distribution within an insurer, and changing market share among insurers. Our sales distributions reflect only stand-alone LTCI. Two insurers reported their number of new employer cases as well as the number of new worksite sales. Combined, they averaged 5 applications per new employer case, which seems to confirm the executive carve-out concentration in our data.

Aggregate Sales Table 1 shows the number of sales and premium in the worksite market by year. As noted above, the worksite market is in decline, with the exception of 2021 due to sales stimulated by the WCF. The shrinkage of the stand-alone WS market is underscored when you consider that nearly two-thirds of 2023 WS premiums came from FPOs on past years’ sales.

Table 2 shows WS sales as a percentage of total LTCI sales. As the market shrinks, the impact of FPOs on past sales becomes larger. FPOs account for WS being a higher percentage of premium (5.9 percent) than policies (5.4 percent). Removing FPOs, the WS premium is 3.2 percent of the total. The 2022 percentages are slightly inflated due to runout sales in Washington.

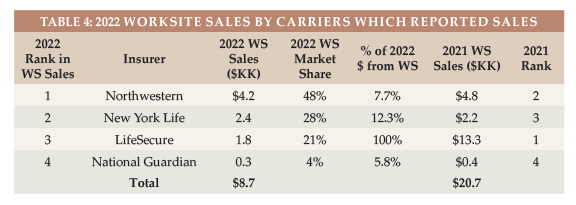

Market Share Table 3 shows the insurers’ reported WS sales, including FPOs and new sales to worksite cases issued in prior years. Excluding FPOs, New York Life would have been in the lead, followed by LifeSecure.

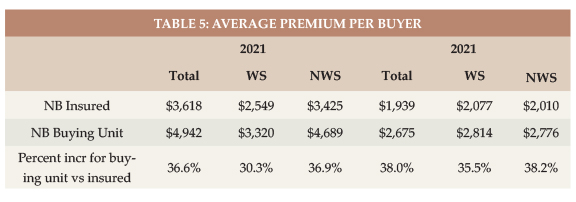

Average Premium Per Buyer Table 4 shows the average premium (without FPOs and without single premiums) per new insured for WS contributors, for WS participants (insurers which provided distributions), and for the NWS market. The total WS market has a lower average premium than those WS carriers that provided distributions. When comparing the WS market to the NWS market, influences such a younger average issue age drive the lower WS average premium.

Table 4 also shows the average premium per buying unit for insurers that provided distributions (a couple comprise a single buying unit). The average premium per buying unit is higher because there are fewer buying units than insureds. The ratio between average premium per buying unit and average premium per insured life is consistently lower for WS sales, because more WS buyers are single and because spouses are less likely to buy in the WS. However, Table 4 likely understates the difference because our WS distributions reflect a higher concentration from the carveout market, which has a lot of couples who both buy.

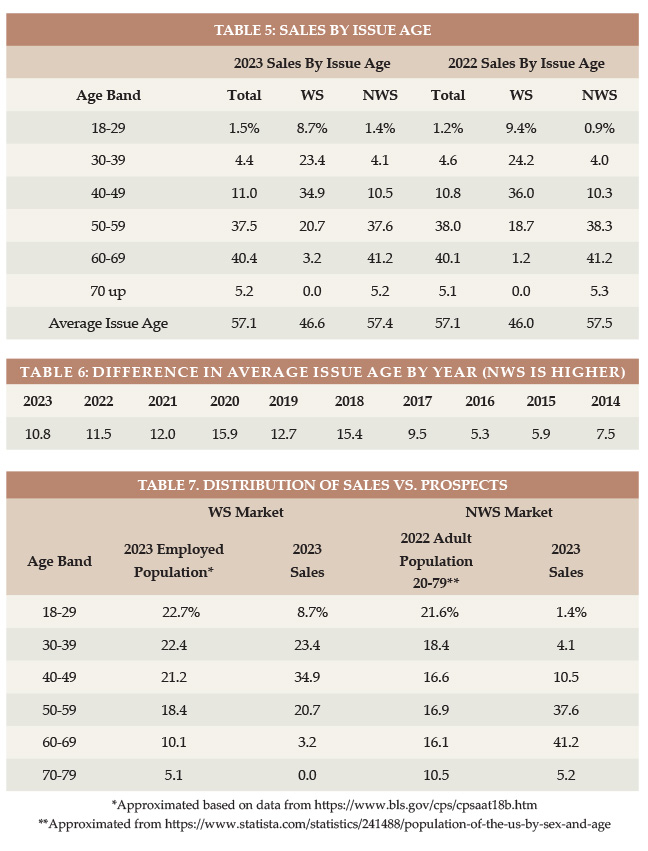

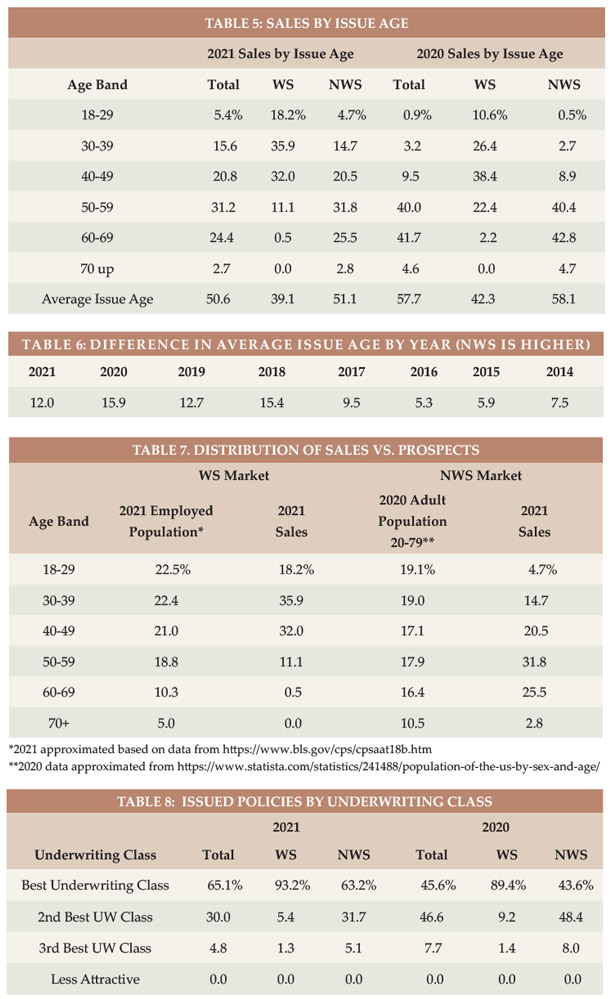

Issue Age In reviewing the balance of the statistical presentations, we urge you to be selective in how you use the data because it is not representative of the entire WS market as explained above.

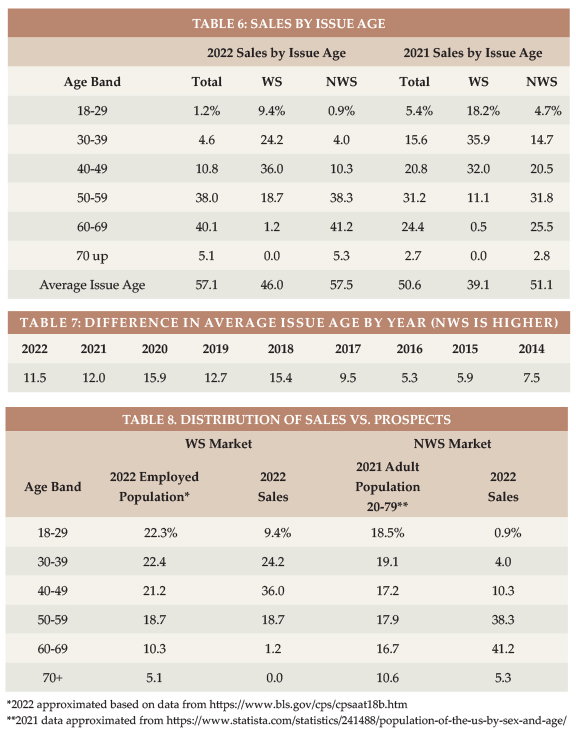

Table 5 shows the distributions by issue age and Table 6 shows, by year, how much older the average age NWS buyer is than the average age WS buyer.

Table 7 displays the relative age distribution of workers ages 18+ compared to the age distribution of purchasers in the WS market and the age distribution of adults 20-79 compared to the age distribution of purchasers in the NWS market. If the percentage of sales in a particular age group is higher than the percentage of population in that age group, we can conclude that LTCI is more appealing to that age group, the industry gets in front of that age group more, and/or more of the applicants in that age group qualify for coverage. In the WS market, the industry is particularly effective with ages 40-49. In the NWS market, the industry is particularly effective for ages 50-69.

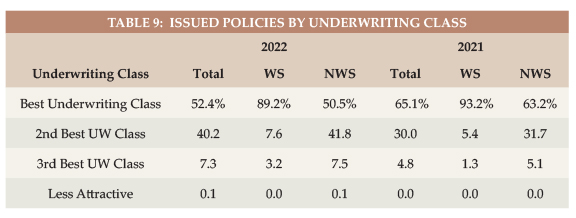

Rating Classification Three of our seven contributors do not offer a “preferred health” discount, so the bulk of their sales are in their best underwriting class. They are also the insurers providing WS distributions, which contributes to the high percentage (92 percent) of worksite policies issued in the best underwriting class, as shown in Table 8.

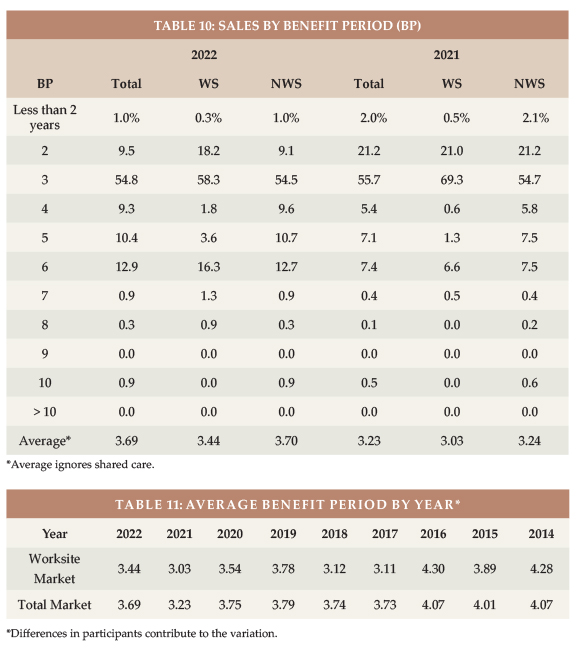

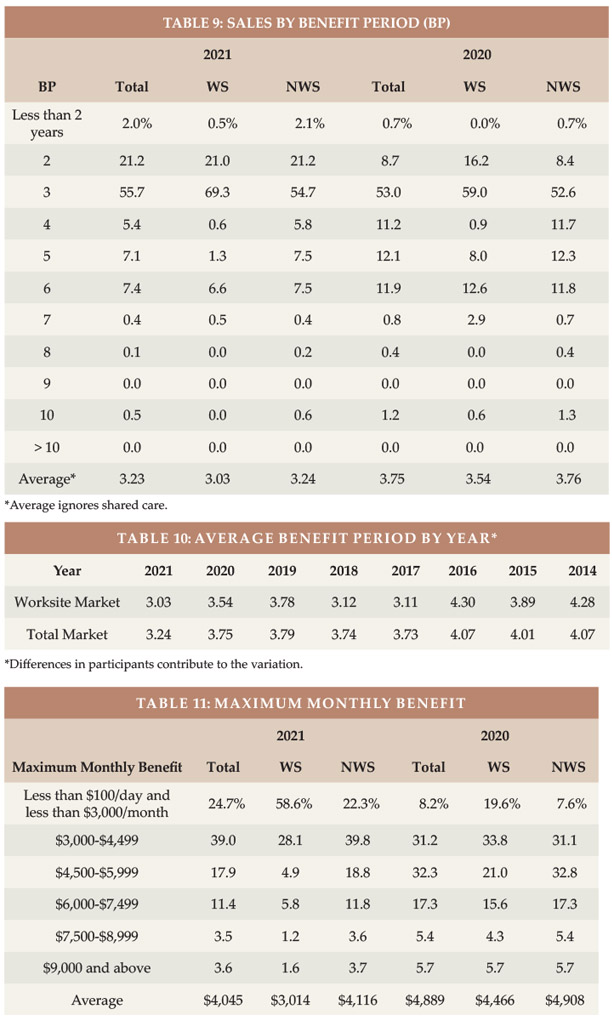

Benefit Period The WS average benefit period is low for core/buy-up programs and somewhat low for voluntary programs. Executive carve-out programs sometimes have longer benefit periods than the NWS market. In 2023, the WS market, for the first time since 2016, had a slightly longer average benefit period than the total market (see Table 9). Table 10 shows the results by year. Note that these statistics ignore Shared Care which, in effect, lengthens benefit period and is more prevalent in the NWS market.

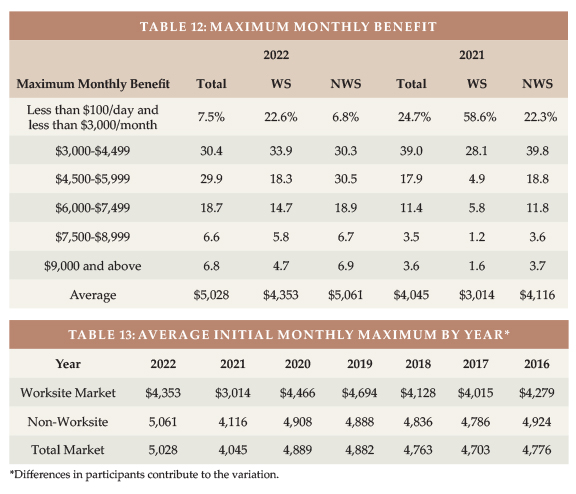

Maximum Monthly Benefit To calculate the average initial monthly maximum, we presume an average size in each size range shown in Table 11. While the WS market had a slightly longer average benefit period in 2023 than did the NWS market, it had a smaller average initial monthly maximum. Table 12 shows that the initial maximum monthly benefit hit record high levels in 2023. The WS initial monthly maximum varies more over time than the total market because of participant changes and how many core/buy-up plans were sold in a particular year.

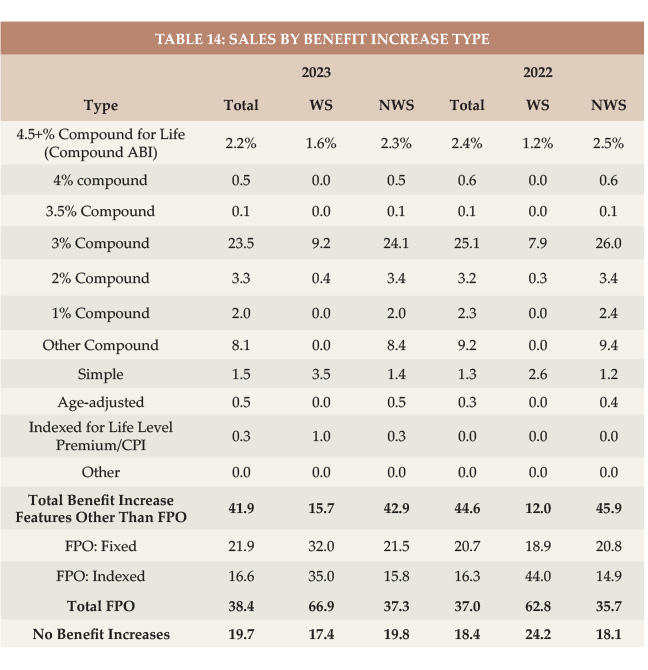

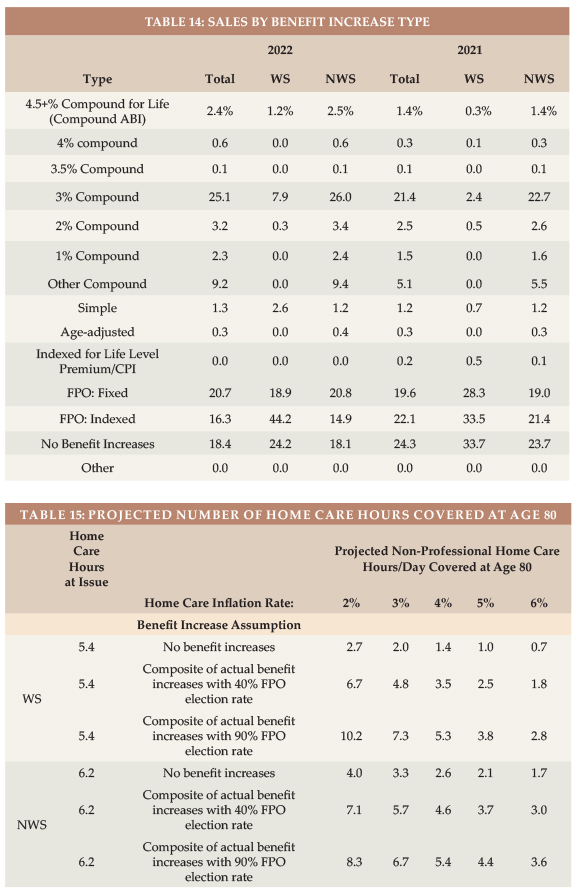

Benefit Increase Features As shown in Table 14, 10.8 percent of 2023 WS sales had compounding of three percent or higher, compared to 9.1 percent in 2022. Of the 2023 WS sales, 17.4 percent had no increase feature and 67 percent had a FPO feature.

In the NWS market, 26.9 percent had three percent or higher compounding compared to 29.2 percent in 2022. While three percent or more compounding is dropping in the NWS, it is increasing in the WS market, albeit still much less common in the WS market.

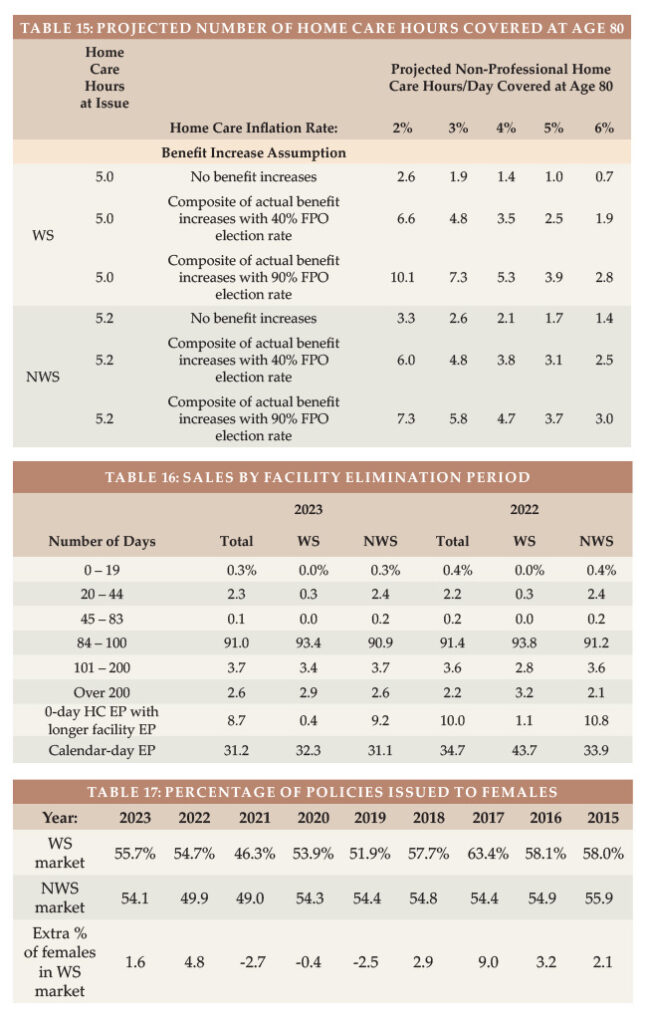

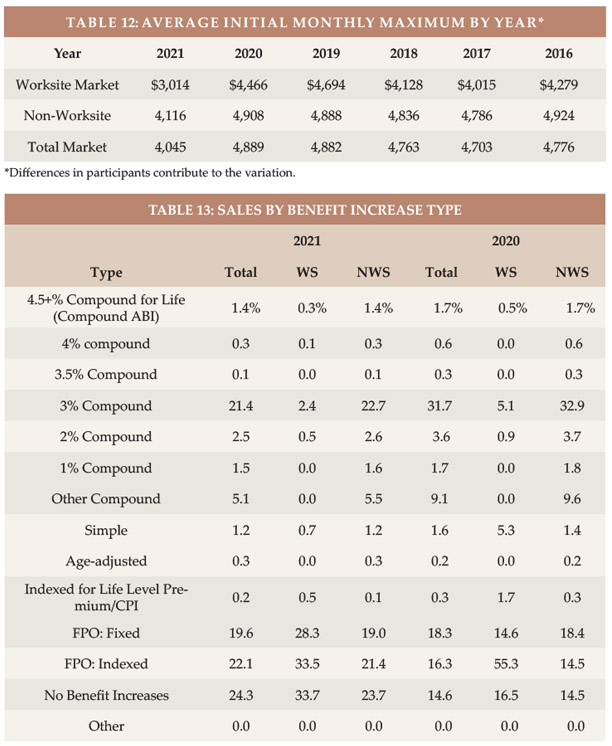

Future Protection Based on a $33/hour cost for home health aides (the median cost according to Genworth’s 2023 Cost of Care Survey), the average WS initial maximum daily benefit of $166 would cover 5.0 hours of such care per day at issue, whereas the typical NWS initial daily maximum of $173 would cover 5.2 hours of such care per day, as shown in Table 15.

The number of future home care hours that could be covered depends upon when care is needed (we have assumed age 80), the home care cost inflation rate between now (age 47 for WS and 57 for NWS) and age 80 (we have calculated with 2, 3, 4, 5 and 6 percent inflation), and the benefit increases provided by the LTCI coverage between now and age 80.

Table 15 shows calculations for three different assumptions relative to benefit increase features:

The first line presumes that no benefit increases occur (either sold

without any benefit increase feature or no FPOs were exercised).

The second line reflects the average benefit increase design using the methodology reported in the July/August article, except it assumes that 40 percent of FPOs are elected (intended to be indicative of “positive” election FPOs, in which the increase occurs only if the client elects it) and provide five percent compounding.

The third line is like the second line except it assumes 90 percent of FPOs are elected (intended to be indicative of “negative” election FPOs, in which the increase occurs unless the client rejects it). It also assumes the FPOs reflect five percent compounding.

Table 15 indicates that:

Without benefit increases, purchasing power deteriorates significantly, particularly for the WS purchaser as younger buyers have more years of future inflation prior to claim onset. For example, with a flat benefit, the number of covered hours of home care at age 80 drops to 1.9 hours for the average WS purchase age if there is three percent inflation. The average NWS buyer would have 2.6 hours of care (rather than 1.9 hours) at age 80 if they had no benefit increases and inflation was three percent because the average NWS buyer is older (and secondarily, buys a larger daily benefit).

The “composite” (average) benefit increase design assuming that 40 percent of FPO offers are exercised preserves purchasing power better than when no increases are assumed. The average WS buyer gains buying power over time if the inflation rate is two percent, being able to pay for 6.6 hours at age 80. But if the inflation rate is four percent, this drops to 3.5. The average NWS buyer generally does better because of a higher issue age, more robust benefit increase features and a higher initial maximum daily benefit. However, the WS market has more FPOs, so when we assume 90 percent FPOs election, the WS market does better. It also does better with 40 percent FPO election and a two percent inflation rate because we presume a full five percent FPO will be exercised.

Assuming that 90 percent of FPO offers are exercised, the average WS buyer would have at least as much coverage at age 80 as at issue if the inflation rate is less than four percent. The average NWS buyer has increasing purchasing power unless inflation averages four percent.

Table 15 underscores the importance of considering future purchasing power when buying LTCI. Please note:

a) The average 2023 WS buyer was 10 years younger at issue than the average 2023 NWS buyer, hence has 10 more years of inflation and benefit increases in Table 15. The actual inflation rate to age 80 is not likely to be the same for today’s 47-year-olds as for today’s 57-year-olds.

b) Individual results vary significantly based on issue age, initial maximum monthly benefit, and benefit increase feature, as well as the inflation rate and the age at which the need for care occurs.

c) By the median age of starting to need care (about age 83) and the median age of needing care (about age 85), more purchasing power could be gained or lost.

d) Table 15 does not reflect coverage for professional home care or facility care. According to the 2023 Genworth study, the median nursing home private room cost is $320/day, which is currently comparable to 10 hours of non-professional home care. However, the inflation rate for facility costs is likely to differ from the inflation rate for home care. From 2004-2023, Genworth’s studies showed the following compound growth rates: private room in a nursing home (3.1 percent), assisted living facility (4.3 percent), home health aide (2.7 percent), and home care homemaker (3.1 percent).

e) Table 15 could be distorted by simplifications in our calculations. For example, we assumed that the FPO election rate does not vary by age, size of policy or market and that everyone buys a home care benefit equal to the average facility benefit.

Partnership Program Background When someone applies to Medicaid for long-term care services, most states with Partnership programs disregard assets up to the amount of benefits received from a Partnership-qualified policy (with some policies, IN and NY disregard all assets). Partnership programs exist in 44 jurisdictions (all but AK, DC, HI, MA, MS, UT, and VT), but MA has a similar program (MassHealth). The first four states to develop Partnerships (CA, CT, IN and NY) have different rules, some of which have become a hindrance to sales. We are not aware of a Partnership-qualified WS LTCI product in those four states, which is unfortunate because the WS market serves many people who could benefit from Partnership.

To qualify for a state Partnership program, a policy must have a sufficiently robust benefit increase feature. At least 29 jurisdictions have lowered the minimum Partnership-eligible compounding benefit inflation rate to one percent. To facilitate Partnership sales in such jurisdictions, an insurer could lower its minimum size from $1,500 to $1,000 if one percent compounding is included in a core program. The policies would qualify for the state Partnership and case revenue and core sales would likely increase. The premium would be more level by issue age, shifting risk to younger ages which can be preferable for the insurer in a core program.

Jurisdictional Distribution We also examined the market share (based on number of new insureds) by jurisdiction. As was the case last year, the WS market share of five states (AL, AK, HI, NC, & VT) was at least 50 percent higher than that state’s overall market share (e.g., if they had a two percent overall market share, they had at least a three percent market share in WS). This could be the result of a single large case in that state. In 18 jurisdictions (same number as last year), the market share of total sales was at least 50 percent greater than the WS market share, suggesting that there may be opportunity for WS sales in these jurisdictions: CO, DE, IN, KS, KY, LA, MA, MD, ME, MO, MS, NE, NH, NV, OR, RI, SD, and VA. (The 9 bold italicized states were in this list last year.) In 7 jurisdictions (up from 5), our participants had no stand-alone WS sales at all (DC, ID, NM, UT, WV, WY and Puerto Rico).

Click here for a chart of the market share of each US jurisdiction relative to the total, WS and NWS markets, and the Partnership percentage by state. This chart indicates where relative opportunity may exist to grow LTCI sales.

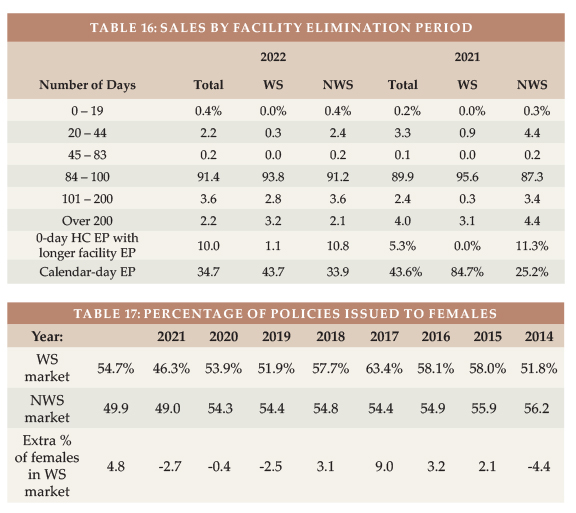

Elimination Period More than 90 percent of the NWS market buys 90-day elimination periods (EPs). For that reason, many WS programs offer only a 90-day EP.

Table 16 shows distribution by EP and how many policies had a 0-day home care feature and a longer facility EP and how many policies had a calendar-day EP (as opposed to a service-day EP). We have reflected that all LifeSecure policies are 90-day EP with a calendar-day definition. Policies which have 0-day home care EP and define their EP as a service-day EP operate almost identically to a calendar-day EP, because people in facilities get daily care.

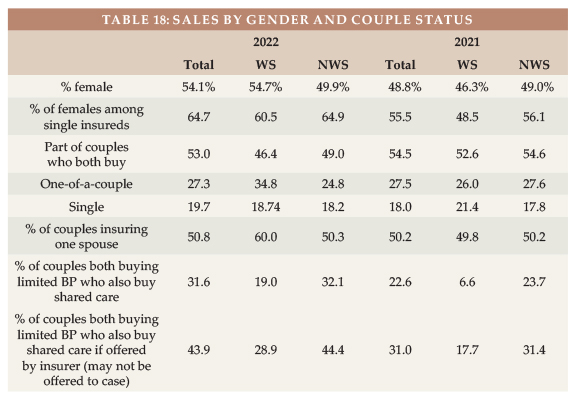

Gender Distribution and Sales to Couples and Relatives Insurers began gender-distinct LTCI pricing in 2013, but unisex pricing continues to be typical in the WS market because of Title VII of the 1964 Civil Rights Act.

Women are 49.9 percent of the US age 20-79 population but have nearly always dominated LTCI sales1. Since 2016, the percentage of female buyers in the NWS has fluctuated from 54.1 to 54.9 percent (see Table 17), except for 2021 when the percentage of females dipped below 50 percent in both the WS and NWS markets because of the higher number of males purchasing coverage in WA. In 2022, the NWS market also had fewer than 50 percent females because of delayed processing of 2021 WA sales, but the Total market reverted to mostly female.

Table 17 also shows that the WS market generally experiences a higher percentage of female buyers (presumably because of unisex pricing), quantifying the above-mentioned “gender anti-selection” compared to the NWS market. To the degree that our WS data is over-weighted to executive carve-out programs, it likely understates the gender anti-selection of voluntary WS LTCI programs. Women make up 46.9 percent of workers but accounted for 55.7 percent of our reported 2023 WS sales2.

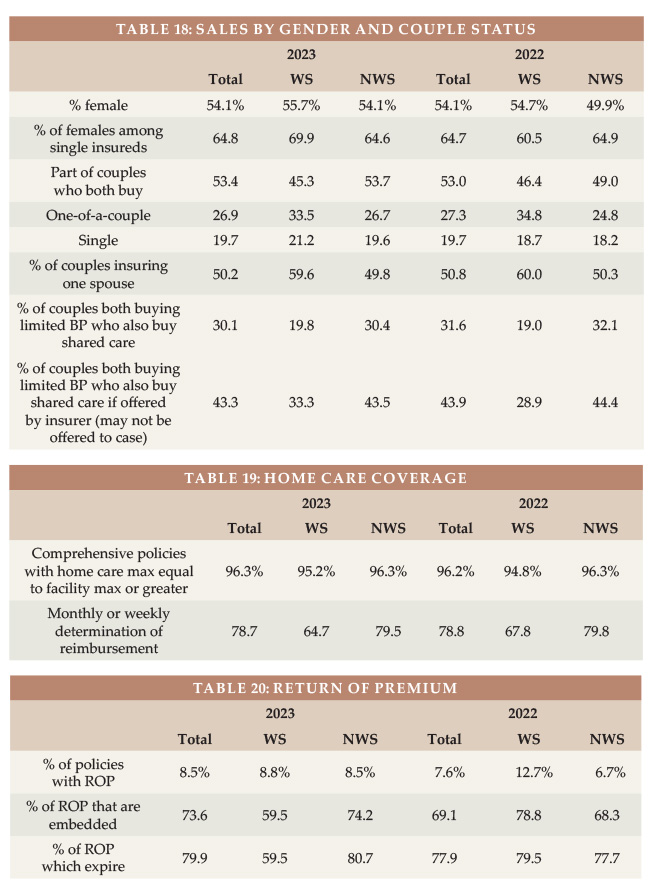

Table 18 digs deeper, exploring the differences between the WS and NWS markets in single female, couples, and Shared Care sales. Our WS data has more couples who insure only one partner (59.6 to 49.8 percent in the NWS market). Shared Care is less often offered in a WS program.

Our limited data with regard to relatives who buy shows that two spouses are insured for every three employees. That’s a high percentage reflective of executive carve-out data. Over time, we have seen about one percent of purchasers are relatives other than the employees and employees’ spouses.

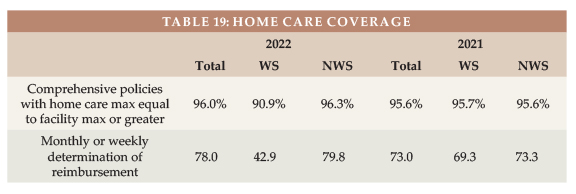

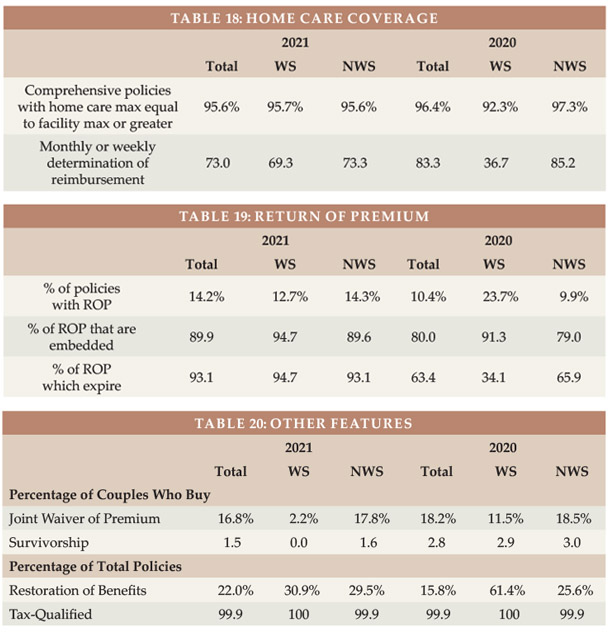

Type of Home Care Coverage Table 19 summarizes sales by type of home care coverage and shows the frequency of monthly determination of benefits. Long ago, WS policies’ home care maximum monthly benefits were 50 percent of the facility benefit; today they are generally identical.

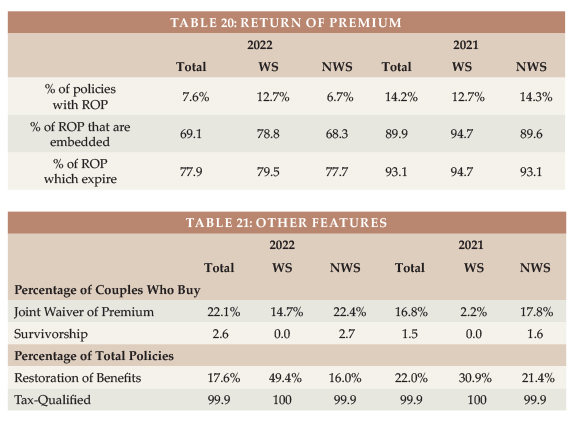

Other Features Table 20 shows that most Return of Premium (ROP) features are automatically included and phase out before death would be likely. ROP with expiring death benefits may provide an inexpensive way to encourage more young people to buy LTCI but does not address the buyer’s concern that they might pay all their life, then die in their 90s without qualifying for benefits.

Table 21 shows lower Joint Waiver of Premium and Survivorship sales to couples in the WS market than in the NWS market. Some products automatically provide Joint Waiver of Premium if a couple buys identical coverage or if a couple buys Shared Care. Employers sometimes are disinclined to add an optional couples’ feature because they are already contributing more money to cover both a married employee and that employee’s spouse than the cost for a single employee the same age.

CLOSING We thank insurance company staff for submitting the data and responding to questions promptly. We also thank Sophia Fosdick and Quentin Clemens of Milliman for managing the data expertly.

We reviewed data for reasonableness. Nonetheless, we cannot assure that all data is accurate. If you have suggestions for improving this survey, please contact one of the authors.

Claims are the lifeblood of any insurance business. If claims are not paid accurately, promptly, and smoothly, no insurance job is justified because all insurance jobs are created fundamentally to pay clients’ claims.

In the long term care insurance (LTCI) industry, there are high-level indicators and detailed experiences that claims are paid well, but there is always room for improvement. As an industry, it is important to optimize results for the consumer and to publicize our success. Criticism, whether valid or not, lives forever on the internet. And people are generally more determined to share dissatisfaction than to describe outstanding service.

Beyond being our mission, favorable claims results are critical to the growth of the LTCI industry (including stand-alone LTCI and all types of combination products, collectively “LTCI” herein). A strong reputation for paying claims encourages producers to recommend that clients consider LTCI, encourages clients to buy and adds meaning to the lives of insurance producers (“producers” herein) and home office staff.

Producers can help by educating clients regarding claims provisions, so clients will know what to expect and also what not to expect. Such education should be refreshed upon periodic reviews. Producers can also help by finding optimal coverage for the client, which can require, among other things, detailed understanding of LTCI policy provisions.

Over time, producers can help clients recognize when a claim might be imminent and can help clients prepare for a claim and deal with their insurer effectively at claims time.

Insurers have a significant challenge. Their responsibility to pay claims promptly and smoothly must be balanced with accuracy. Overpayment of claims can lead to price increases on inforce policies and can encourage individual and coordinated fraud.

Most people recognize that existing processes can be improved. That is evident because even insurers with closed blocks of business have invested a lot of money to improve their claims practices.

In this series of articles we intend to look at many aspects of the claims process, hoping to help the industry improve and market stellar service. We’ve teamed together because we share passion for this topic and because it is daunting and benefits from multiple perspectives. We can do a better job if producers, home office staff and perhaps other readers help. At any time, readers are invited to send questions, comments, examples of favorable or unfavorable claims processing, and suggestions to either or both authors:

Here is one of Claude’s favorite claims experiences: I was about to go on a webinar when I got a phone call from a former associate who had spoken with three sisters whose mother was on claim. Naturally, claim payments were going to the claimant’s husband. But, unbeknownst to the insurer, he had repeatedly refused to pay for his wife’s care, telling his daughters that it was his money to spend as he’d like. As I had only a few moments before the webinar, I quickly left a message for a claims person at the insurer. During the one-hour webinar I saw a flurry of notices in the corner of my screen indicating communication. After the webinar I saw that the bursts of email identified the client; secured information demonstrating that claim payments should go to the daughters; and informed them that the benefit payment had been switched to them. Within an hour, the problem had been fixed!

Certainly, there are a lot of claimants/families who have been frustrated seeking LTCI claims; we’ll address at least some of those issues in this series. However, as we noted earlier, there are some high-level indicators that the industry is doing a good job.

The industry has paid about $225 billion in claims, projecting from the $196 billion as of year-end 2022 reported in the 2024 Milliman Long-Term Care Insurance Survey published in Broker World magazine in July/August, 2024.

The NAIC passed Independent Review (IR) of LTCI claims to help clients get satisfaction if they think their claim was improperly denied because they were deemed not to be “chronically ill”. (For text, see p. 62+ of https://content.naic.org/sites/default/files/inline-files/committees_b_senior_issues_exposure_ltc_model_act_641.docx). Most LTCI insurers extend IR beyond statutory requirements (e.g., to policies issued prior to the effective date of IR). Nonetheless, only a very small percentage of claims go to IR. Steve LaPierre is president of LTCI Independent Eligibility Review Specialists, LLC (LTCIIERS), the largest IR organization. He reports that they upheld the insurer’s decision 98 percent of the time in 2022. It speaks well of the industry that they extend IR beyond legal requirements, that few claims go to IR and that 98 percent of those going to IR are resolved in favor of the insurer.

A 2010 study of LTCI claims payment accuracy for the Department of Health and Human Services1 found that insurers paid 3.3 percent more in claims than the auditors felt was justified under the terms of the contracts. Naturally some claims were erroneously declined, but the auditors found that the questionable claims which were paid* more than offset the claims that the auditors felt were erroneously declined. (*The auditors didn’t say those claims should not have been paid, just that there was not adequate justification in the files.) The study included seven insurers which were responsible for 70 percent of the claims at that time (Bankers Life & Casualty, Genworth Financial, John Hancock, Long Term Care Partners, Medamerica, Metropolitan Life, and Prudential.) Other insurers might have had different results.

It is ironic that we hear so much about the huge rate increases on older LTCI policies (generally those issued before 2010 and worst for those issued before 2000) but we don’t hear the flip side: State regulators would not be approving those rate increases if they were not convinced that the insurers are paying a lot more claims than they expected and will continue to do so.

Our future articles will cover topics such as:

The insurers’ perspective: Challenges they face, actions they’ve taken and areas of potential improvement.

Ways producers can help clients reduce claims, prepare for claims, recognize that claims are imminent and get claims satisfaction.

Key provisions that producers should note. (The importance of such subtleties encourages some producers to outsource LTCI sales. There are many ways producers can have very positive long term care planning conversations with clients, identifying a possible interest in LTCI before introducing their client to a specialist.)

The 2024 Milliman Long Term Care Insurance Survey is the 26th consecutive annual review of stand-alone long term care insurance (LTCI) published by Broker World magazine. It analyzes the marketplace, reports sales distributions, and describes available products. More discussion of worksite sales, including a comparison of worksite sales distributions vs. non-worksite sales distributions will be in Broker World magazine’s September/October issue.