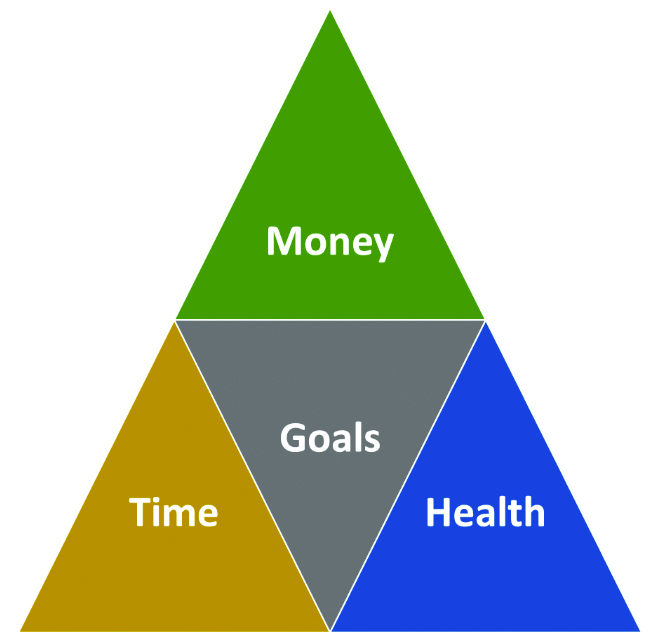

In the distribution world of life insurance and annuity products, it is our duty as product bearers to help advisors determine which products are appropriate for specific clients and help to distinguish what products will have the best chance of achieving the client’s personal and family goals. Everyone, speaking in generalities, has a combination of time, health, and money that serve as driving factors for product suitability and design. Time and health are deteriorating factors, whereas money, in the form of wealth, can be either deteriorating or improving depending on the level of planning. As we know, wealth has the ability to transcend our own mortality, or it can be squandered and taxed away. Either scenario has countess historical examples. Time, health, and money can help determine the risk, insurability, and flexibility of the product universe for which clients are suitable. Their goals help to determine what product and design is utilized within that universe.

Given that the topic for this Broker World issue is retirement, estate, and legacy planning, I think our simple lead-in analysis above is fitting. And knowing how we all have limited time, pun intended, I think we should narrow the scope to annuity and life insurance products for this article. My goal has always been to simplify the language of the discussion in order to help our wholesale professionals engage financial advisors more effectively. We would all be better served to move away from industry jargon and interact in simple, real terms.

The amount of time a client has can be a good determinant of how much risk they can assume. More time, given the historical long-term performance of the markets, lends to variable and market-linked products to maximize accumulation, regardless of whether it is an annuity or life chassis. Having less time, of course, typically cuts down on risk tolerance where fixed or indexed products would potentially be better solutions. The client’s health will be a primary factor for insurability and will likely drive the decision between either an annuity or a life product. We know that life insurance has more favorable tax-treatment for supplemental income and death benefit compared to annuities; however, if the cost of insurance (COI) outweighs the cost of tax (COT), then it may not make sense. Perhaps for a legacy goal, but probably not for income. COI is usually determined by three main factors: Age, health, and net-amount at risk (NAR). For example, a young, healthy person who is looking to buy the minimum amount of insurance, in a standard accumulation design, will have very low COI. In contrast, an older individual with health issues looking for large death benefit coverage will find that COI is extremely high. Advisors and clients have historically perceived life insurance as being too expensive, but it simply depends on the situation and product design. As an example, we’ve demonstrated that over the life of a client, an overfunded VUL policy is virtually the same annualized cost as the leading investment-only variable annuity product on the market today. Annuities don’t require medical underwriting and may be a better option for those on the lower end of the health spectrum, still maintaining a tax-deferred wrapper for accumulation. Additionally, annuities can offer living benefit riders and guaranteed income streams that can bring peace of mind and income security.

Something worth mentioning within this commentary is the new wave of accelerated underwriting that has simplified the client process for permanent life insurance. If a client fits the time (age 18-60) and health parameters, they can get a life insurance policy issued with lab-free underwriting in less than a month in most cases. Albeit there is a money restriction for this, limited to policies under $1 million face amount, but I expect the face capacity for these programs to expand in the coming years. This is especially appealing for the max-funded, minimum non-MEC designs. Just the mere thought of underwriting has turned countless advisors and clients away from life insurance solutions, especially in the wire-house channels where advisors are used to transactional solutions. If we can lessen this burdensome process, it then becomes a pure comparison of the features and tax-benefits between annuity and life products. Finding those HENRYs (High Earners Not Retired Yet) who have the best combination of time, health, and money is golden to financial advisors as they have maximum planning flexibility. Sometimes a LOUIS (Loved One with Unneeded Income Streams) can assist a HENRY in funding an annuity or life policy, as well as policies for themselves. Every advisor has several clients that fit a LOUIS description in their book, and what they need to do is leverage those clients to bring in generation two, the HENRY clients, with a transfer and legacy strategy. (I review all of this in an industry presentation I’ve given at several events that can be viewed and downloaded on the Sales and Positioning page located at the top of www.VULSource.com.)

Having a great deal of money adds flexibility to planning and opens up the product universe, such as private placement annuities and life insurance, in addition to traditional retail products. It also may impact a client’s risk tolerance regardless of how much time they have, but that is certainly case by case. What we have begun to see is a combination of a traditional life sale with a private placement solution overlay: Acquiring the needed death benefit base in the traditional market (synthetic re-insurance), and then using private placement to create a cash value bucket for investment with little underwriting needed. Our friends at Investors Preferred Life, a private placement carrier, have such a unique solution. Lombard is another carrier that is active in this particular space. That is something that could be applied either to the in-force block or with new business, as long as the underlying death benefit base is either traditional GUL or lifetime no-lapse VUL. These are really only for monster sized cases, but it is valuable to have that arrow in the quiver just in case. Obviously, clients with money are more interested in estate and legacy planning to effectively transfer that wealth to the next generation. In the VUL space, we’ve seen a lot of no-lapse guaranteed (NLG) products being sold, where the client is looking to achieve the maximum guaranteed-to-life death benefit for the lowest premium. It’s really a post AG-38 GUL sale disguised as a VUL for all intents and purposes, but those cases are largely placed with Lincoln and Prudential’s NLG products. The IUL space has seen skyrocketing growth over the past five years, and those products are good for clients who don’t want to assume the downside risk of the markets but want upside potential. To apply it to our example, they are clients who have limited time, but are in good health and still desire accumulation. However, we have begun to see an arms race in the IUL space with AG-49 dodging, spreadsheet leaping new features that scare the living daylights out of us. It’s all in the insurance company’s pocket with IUL and there are too many levers they can pull. We simply don’t trust it, and we have the feeling that that market is headed for a massive collision course with the regulators. Unfortunately, that usually happens only after customers get hurt.

Of course, indexed annuities are the sister solution to IUL on the annuity side of the fence. We are also seeing registered annuity products being launched that either are indexed in nature, or are more of what they call “buffer” annuities. That would be similar to the BrightHouse Shield product where it will assume a certain percentage of downside risk in a given time period and has a corresponding cap rate. Great American and other carriers have also launched similar products. We have started to notice the annuity world open up to third-party distribution of those products, which is nice to see for our IMO and FMO partners. We will continue to monitor that world as it develops.

To me, the goal of the client typically comes down to two objectives—either income or legacy planning. It certainly can be both, but those serve as corresponding ends to the spectrum. Legacy planning would include estate planning and final expenses in my view, and income planning would include anything from supplemental retirement income to long term care financial assistance. As a side-note, the combo life and long term care sale has been very popular in the life insurance industry and is picking up momentum. In the VUL space, Lincoln will be adding a long term care rider in 2019 to join Nationwide, John Hancock, and AXA. For a pure legacy objective, a MEC might be a decent design. Our industry likes to demonize modified endowment contracts, but a MEC still maintains the tax-free death benefit status and will allow for a single, lump-sum premium. Most of the variable annuities that were sold historically, the first distributions ended up being death benefit payments which are taxable to beneficiaries. Clients might have been sold on tax-deferral and income, but they ended up using the annuity for a death benefit where life insurance may have been a more efficient solution. If a client has income as a part of their goals, then a non-MEC status is the way to go.

Within the confines of the IRS tax law, life insurance policies can be designed to favor either cash value or death benefit depending on the client need. I like to use the below diagram when talking with advisors on where those premium dollars can go and what goal they can support.

In conclusion, I think it is important for us to talk in simple terms and to evaluate the client’s factors of time, health, and money to determine what risk, insurability, and flexibility they might have. It is ideal to find the client with a lot of time, health, and money, but that isn’t going to be the case for the majority. Health is really the pivoting factor in determining between a life or annuity product as it pertains to our above discussion. Life insurance has better tax-treatment for income and death benefit, but if a client can’t get favorable underwriting then they won’t get a good deal. Wealthy clients have more flexibility in the design and funding of products, and perhaps both an annuity and life solution would be appropriate for serving multiple needs. Having more money also opens up the private placement world, where there are a multitude of options. Financial advisors are all-to-often biased against certain products for one reason or another. Most of that is centered around the perceived cost of the products without a clear understanding of the value they bring. Somehow, we have to communicate to advisors that every product has a rightful place, it simply depends on client factors and their goals.