Who’s Selling What? To Whom, How And Why?

The relative and apparently inexplicable success or failure of long term care insurance sales has persisted as a frustrating mystery for too long. The ability to reliably gain additional sales momentum and build upon successful sales results continues to defy the most empirical or deductive reasoning. The industry has repeatedly tried to examine prospective consumer predispositions to buy and then subsequently carefully examines consumer rationalizations of those who have taken definitive action to protect themselves and their families. Unfortunately, as you hold this kaleidoscope up to the light, we seem to have forgotten that it is the advisor that has the greatest influence and understanding of the patterns finally projected.

Last year, Oliver Wyman and Ice Floe Consulting, LLC, embarked on a joint effort to uncover and understand attitudes and opinions of the agents and advisors who, despite these challenging times, continue to discuss long term care planning with prospects and clients. The research reported in this article has been supported by a wealth of industry friends. Insurance companies, distribution organizations, professional associations and the media have stepped forward in an effort to enhance our understanding of the future of the long term care planning market utilizing all the tools at hand to help leverage care provision alternatives.

Refinement of the Who is Selling What? To Whom, How and Why? Survey was provided by the following insurance companies:

- John Hancock

- Lincoln Financial

- Mutual of Omaha

- Nationwide

- New York Life

- Northwestern Mutual

- Pacific Life

- Transamerica

- Securian

National professional associations that stepped to the plate to support the effort include:

- NAIFA

- NAILBA

Industry trade media support came from:

- Broker World magazine

- Center for Long-Term Care Reform

- NAILBA Perspectives

And of utmost importance, was the support and marketing efforts put forth by our colleagues on the distribution end of the equation, including:

- Art Jetter & Co.

- Borden Hamman

- CPS Horizon

- Long-Term Care Insurance Partners

- The Marketing Alliance

- LTCR

- MasterCare America

- National Brokerage Agencies

- National Associations of Independent Agencies

- National Long-Term Care Network

- The Brokerage, Inc.

These companies and organizations helped us create a representative sample supplementing the generic master list of 400,000+ licensed life and health agents we would reach out to.

We need to emphasize that the current survey data is specifically agent/advisor centric. The desire to be vicariously present at point of sale helps us identify successful sales techniques and further product innovation. The sales success focus began here in Broker World magazine in May 2004 with the release of “The Producer’s Perspective on Long Term Care Insurance.” Hagelman Consulting facilitated this original work at the height of stand-alone sales with help from LIMRA and the Society of Actuaries. Changing the focus to the advisor’s views of what convinced the consumer to buy did provide an alternative perspective prevailing consumer research. In previous surveys when consumers were asked the most important considerations when purchasing long term care insurance, they identified their excellent judgement in financial matters to protect their assets. Advisors however overwhelmingly identified the consumers’ personal experiences with caregiving as the greatest factor in buying.

The transition over the last 15 years to a world in which 90 percent of all long term care insurance planning solutions are defined as combo life demanded a return to the agent’s perspective. It is our hope that with the continued support of our many long term care planning colleagues that on-going successful analysis from this viewpoint will become a permanent feature of ongoing research into best practices for sales success.

There is much data present in survey responses that helps us understand current practices and perhaps redirect product offerings by fine tuning sales efforts. Highlights of survey findings include:

- An equal proportion of respondents start the long term care planning discussion by leading with a long term care need and those who incorporate it within an overall financial planning process.

- 85 percent of respondents were over age 50

- 59 percent were 60 plus.

- 75 percent focus on an upscale market.

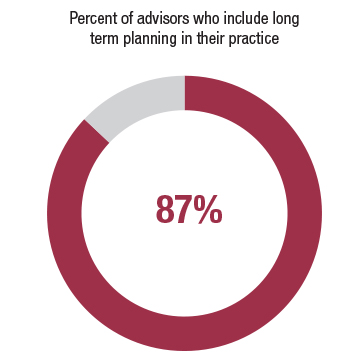

- 87 percent include long term care planning in their practice.

- Only 12 percent of those surveyed described themselves as exclusively long term care specialists.

- Survey respondents equally preferred stand-alone and combo as their product preference.

- Although there does seem to be a degree of confusion as to product features, particularly the difference between IRC 7702B and IRC 101g riders, 85 percent claimed to be comfortable discussing all product options.

- The greatest product comfort level is with stand-alone policies.

- The greatest discomfort is with chronic illness accelerated death benefit riders.

The 2019 LIMRA Combo Life Report found that 59 percent of all long term care insurance planning options sold included “zero premium riders.” In our survey:

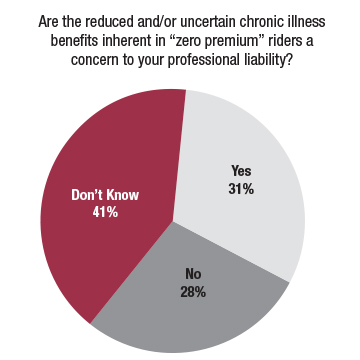

- 67 percent of respondents do not believe these riders help them close more sales.

- The remaining 33 percent consider it an important feature.

- Concern over IRC 101g ADBR’s utilizing the discount or lien method of benefit access raised concerns over professional liability.

Respondents indicated that little happens until the long term care planning conversation is initiated.

Consumer awareness enhances a proactive sales effort.

As previously mentioned, 81 percent of respondents proactively engage consumers in a long term care planning discussion. However:

- 26 percent stated that consumers raise the issue first.

- 42 percent indicated that consumers raise the issue more frequently than they do.

- 40 percent indicated that consumers frequently ask specific questions about “financing” the long term care risk.

Understanding consumer buying pre-dispositions that facilitate a sales opportunity, as perceived by advisors, points to the prospect’s prior personal experience.

The second most expressed consumer motivation was a desire to avoid dependence. Protecting assets was a distant third.

One of our survey’s primary missions was to determine what “power phrases” get consumers to “yes.” They include:

- Peace of mind.

- Desire to age in place.

- Concern pertaining to the high cost of care.

- Personal knowledge.

- Running out of money.

Best practices as it pertains to policy review provides an optimistic marketing landscape for future sales opportunities.

Policy review is a balancing act between existing policy performance and enhancing quality long term care or chronic illness benefits.

Perceived quality of benefits, at the point of need, is an important aspect of current sales. Policy features that most enhance consumer purchasing interest are:

- Available policy features and options

- Premium rate guarantees

- Inflation protection

- Company experiences with long-term care insurance

- Joint policy or benefit pool

- Financial ratings and reputation

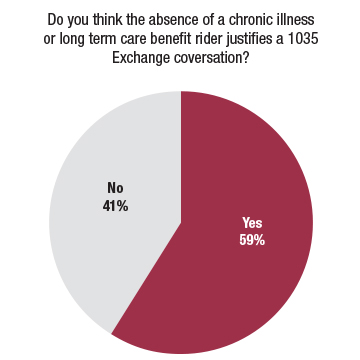

We have witnessed the market shift to combo life policies. With this comes an increased awareness and understanding of the value of a 1035 Exchange.

Additionally:

- 85 percent of respondents consider adding a chronic illness or long term care benefit rider is in the policyholder’s best interest.

- 79 percent say their policy review conversations with existing clients includes adding policy benefits covering long term care costs.

Three additional important takeaways from the survey include:

- Agents/advisors realize that future sales growth will come when products become simpler and more affordable to the middle class.

- Price (affordability) matters as much as meaningful long term care or chronic benefits.

- Agents/advisors value the training they receive from their wholesalers and insurance companies. They want more.

Kudos for making this survey possible goes to Oliver Wyman and in particular Vince Bodnar, Carter Khalequzzaman, Elizabeth Hoch and Angela Cobble.

For complete survey results please go to the Oliver Wyman website www.oliverwyman.com/our-expertise/insights/2020/aug/long-term-care-planning-survey.html or the Ice Floe Consulting website www.ltcauthority.com.