The number of registered investment advisors, or RIAs, in the industry continues to grow along with the percentage of overall assets they manage. As they become more relevant, so does the attractiveness of their business model for many financial professionals currently at broker-dealers and wirehouses. Advisors can join an existing RIA team or form their own. Most of them go “all-in” on the fee-based model, dropping their FINRA licenses along with any reliance on commission-based products. They are regulated by either their respective state or the SEC, which is considered by most as less burdensome than complying with FINRA, but they must adhere to a fiduciary level of care. The world continues to vilify commission-based products prevalent in the insurance marketplace; however, it is hard for anyone to deny the benefits they provide or the solutions they bring to the client planning process. RIAs will continue to have a need for annuity and life insurance products, it is just how they choose to gain access to those products for customers. On the flip side, many distribution organizations are looking for ways to work with the RIA community in a more effective manner. These two forces colliding create opportunity but also some confusion.

Several carriers have begun aligning themselves to this trend by offering fee-based products. At The Leaders Group, we mainly see this with variable annuities, registered indexed-linked annuities (RILAs), or variable universal life insurance (VUL), but there are several fixed solutions as well. Currently, there are numerous advisory annuities with a limited number of life insurance products available. These products require a licensed insurance agent and, if it is a registered product being sold, will also require that agent be FINRA licensed and registered with a broker-dealer. Typically, the RIA doesn’t have anyone on staff that is insurance licensed, let alone FINRA licensed, so they need to outsource that service. That is where this concept of an OID comes into play, or an outsourced insurance division, where sales professionals of an annuity IMO or insurance BGA can engage RIAs in the sale of these products for customers.

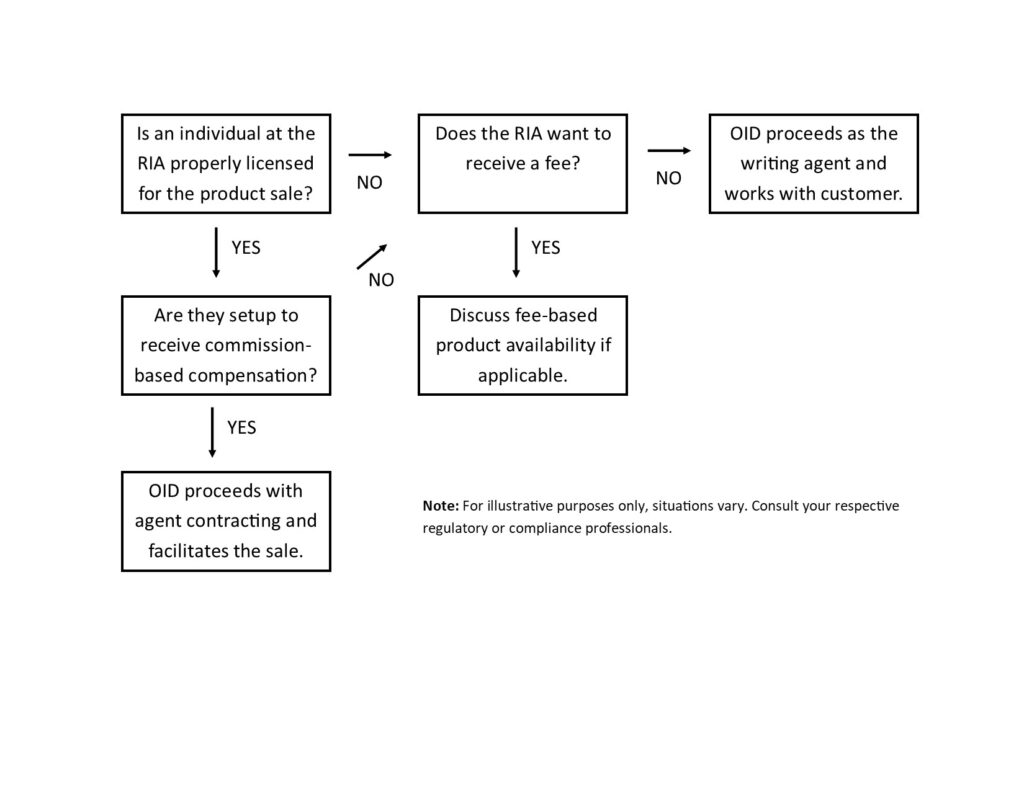

The most straightforward method is for the representative of the OID to be the writing agent and offer the traditional commission-based products to the RIA customers. Retail and/or wholesale compensation is paid to the OID. The RIA can become comfortable with this if they don’t view that relationship as a threat to their business and trust the expertise of the sales individual and organization. Since most IMOs or BGAs don’t engage in gathering assets or managing money for a fee, this is usually a short hurdle to overcome. In this case, the RIA isn’t interested in being compensated for this transaction but can be added as a third-party authorization following the sale to help monitor or manage the product. They may charge a fee-for-service or incorporate another planning fee within the normal dealings with the customer for their time if desired.

Another avenue is for the OID to work with the carrier(s) on a specific fee-based annuity or life product for distribution to the RIA community and engage in an agreement. That agreement can allow for a marketing or distribution allowance to be paid to the OID for business conducted which is not drawn from the product itself. Fee-based products, by their nature, are largely designed without commission structures. Instead, a fee is charged and paid to the RIA for management of the underlying portfolio or product. However, the sale still requires a licensed insurance professional and may require a registered representative. If it requires a registered representative, suitability at the broker-dealer level will occur for the sale which does place a degree of liability on both that BD and the writing agent and is something worth pointing out. Many IMOs and BGAs have a wholesale mindset because that is how they typically operate, and they are somewhat removed from direct liability of the sale. Whereas, in this instance, they are acting directly with the customer as the writing agent (or will be perceived as such by regulators). The considerable volume of registered product sales from some of the more established OIDs can be a challenge at times to manage, but the evolution of technology processes, such as RedTail with a LUMA integration as an example, can provide product comparisons and the necessary customer information electronically for proper suitability review processes to take place. Additionally, education provided to the OID and RIA on the necessary processes and their respective responsibilities is paramount to a successful engagement.

Over the past five years, The Leaders Group has helped many wholesale organizations set up OIDs as well as helped individual carriers set up internal/external sales desks for product distribution. The carriers usually have their own broker-dealers, but they are not built or designed to facilitate the necessary retail suitability review on the individual sales, so they outsource that component to a BD that can take that on for them such as ours.

Some RIAs have staff members who are insurance licensed and/or registered with a broker-dealer. They may have made the proper additions to their Form ADV to disclose the ability to receive commission-based compensation. In such an instance, the BGA or IMO can work with them simply as a wholesale entity as they typically would with other downline agents. For fixed sales, the carrier compensates the retail agent and the wholesale entity separately. For registered product sales it is similar, but the carrier pays the respective retail and wholesale broker-dealers compensation to then pay the associated parties. The dynamics of having both a broker-dealer and an “outside” RIA relationship can be tricky to manage for the RIA organization itself, but there are ways in which to properly navigate those waters. If an independent RIA would like to approach a broker-dealer to get someone on staff registered, there are a very limited number of broker-dealers that would be “friendly” to this relationship without oversight fees or revenue sharing.

The end game is to get to a point where RIA customers have access to the best solutions available, regardless of how the logistics of the sale take place. To do that, the RIA community needs to feel comfortable with engaging OIDs. It is a confusing marketplace but, with proper guidance, it can be a fantastic collective effort operating within the regulatory guardrails. In our review, it is common that a commission-based product may be more advantageous than a fee-based product for a particular customer, so it is important to have an open mind to both configurations. We find this particularly with living benefits or lifetime income product attributes or riders. Of course, the advantage of the fee-based product design is that it allows for the RIA to receive a fee, which aligns incentives to do what is best for customers on an ongoing basis. For the variable life insurance space, we have seen limited product in the fee-based arena, outside of Nationwide’s Advisory VUL which has garnered a vast degree of interest. The VA and RILA space have many solutions available, as well as fixed solutions, which we suspect will continue to expand in scope and quality.