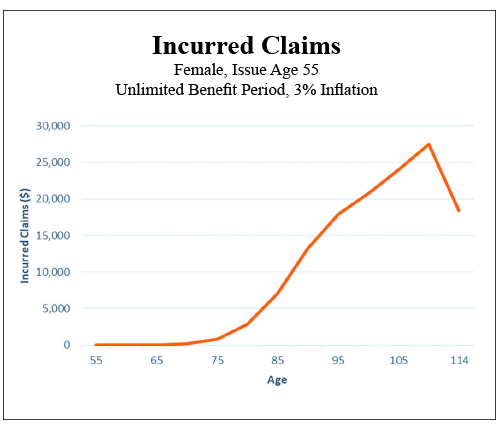

Truthfully this basic mathematical concept has gotten us into more trouble than we have ever acknowledged. On which side of justice do you wish to fall? In the case of chronic illness risk, average or even median numbers can be very skewed and seriously misleading. We do however have to have a target to try to accommodate. The real problem all along has been the nature of the risk itself. You must be disabled to qualify, but you must be healthy to buy. We have never come to grips with all the time in between. All those years of virtually non existent claims have played havoc with our thinking. Please take a moment and carefully review this long term care claim occurrence chart. It looks like an inverted alpine ski jump, with relatively level cross country skiing before rapid acceleration as you begin a blast off into claims in your late seventies ending with the universally required jump of faith into the hereafter. Where is the middle of this? And even if you were to arbitrarily choose one, what would it mean ?

In this environment we have built a failing empire of product that is perhaps Ill fitted to the reality of the risk. We keep selling risk protection measured against “average” quantities of the need for care. What if we simply admit that we do not need a lot of insurance for a lot of years? What if we don’t actually need inflation protection until claims ultimately begin to heat up? What if we didn’t need large daily room benefits until we actually do need them? Is it really all that crazy to suggest that we stop carrying this giant boulder of unneeded risk completely through our income productive and healthy lives? Must we struggle under the weight of risk that is simply not evident? Must we endure this interminable slogging progression to a known and eventually vividly clear risk? It is not just looming over the horizon, it is frankly and almost exclusively smack dab at the end of the journey.

Now let me respond briefly to the actuaries, who are by now squirming in their seats, that I have forgotten that we need all that extra money and that is exactly why the most important ingredient of long term care/chronic illness is the necessity of establishing the required reserves to meet future claims. Let me begin by suggesting that inadequate reserves are already the bane of every dollar of premium on the books, and that reducing perceived versus actual claims pricing might provide commensurate surplus relief and savings. Adequate reserves and carrier solvency do go hand in hand. I would, however, argue that building product to form fit the aforementioned chart does release pressure on the pricing equation.

Now let’s return to the silliness of using averages anywhere near our conversation to reform product offerings and enhance sales. As an example let’s look at the most common statistic used in our seemingly futile attempt to quantify the risk: According to the U.S. Department of Health and Services, the popular prediction for needing long term care services on average is for women 3.7 years and 2.2 years for men—which frankly tells us nothing—as we know from multiple sources that almost all claims range from one day to over 12 years and that half of all claims are over in 12 months. Now you attach any cost of care information you wish and Abra Cadabra! You have a quantification of the problem. (Maybe.) So when you plug in median costs from your favorite cost of care source you should come up with an average problem of $150,000 to $250,000. But the disparity in individual claim size plays hell with the math.

My current favorite statistical quote regarding the moving target is from PricewaterhouseCoopers 2017: The cost of services “a quarter of the time is less than $25,000 and another quarter of the time the cost is over $240,000.” Which says to me most claims are small, with a meaningful possibility of a catastrophic claim, but that the majority are somewhere in between and remain manageable with even a minimum addition of insurance dollars. I’m sure enough has now been said to disturb almost everyone. So once again…

Other than that I have no opinion on the subject.

Serious Flaws

Fairly certain no one will argue with the notion that limitations or restrictions that apply to specific policy benefits can be considered “flaws.” Any benefit that is not complete as presented must be inadequate by definition and therefore “flawed.” What “is” is of course crucial, but what “ain’t” is critical to our professional survival.

A vibrant combo life and annuity market has bubbled to the surface. As predicted repeatedly in this column over the last 10 years. (Sorry, I couldn’t stop myself.) You simply do not want to be the company that does not have a critical illness/long term care combo option. Not having one paints a giant target on the back of any existing coverage. Home office 1035 personnel are vibrating in anticipation. Combo policies have been around forever; truthfully the two birds with one stone story never loses its luster. The corollary truth is equally important: Two risks require two costs. Nobody rides free.

This is specifically why the adherents of supposedly free, no up-front cost, rear-end load, “discount” method chronic illness benefits Fry My Toasties! The obvious bears repeating—there is no free lunch. The entire cost of carrying the additional risk will be deducted from future benefits owed and then some. I recognize it’s fun to let the words, “If you don’t use it—it cost nothing” spill from your lips. Unfortunately the corollary truth becomes if you do need it, you have no real idea what the hell “it” is. That unknown, unidentified and currently unavailable for viewing, is also often sheltered from the light of day by built-in obstacles to claiming in the first place. The most glaring example being a requirement that benefit payment requires a permanent disability. The NAIC has allowed a more HIPAA-friendly definition for several years. The cost to the policy is infinitesimal but the benefit to the buyer is critical. Some companies have gone back and revised their definitions, which should be applauded, and new product is more likely to include the newer language as well—which makes the benefit much more copasetic. But if it’s a “discount” method payment your actual benefit, although more liberally defined as the benefit amount, is still a mystery until you really need the money. I must wonder about the efficacy of carrying sufficient E&O in retirement to be prepared when the “surprise” gets sprung on the uninformed policy holder. Bear in mind that the benefit is unknown until your client comes face to face with the reality of the imbedded shortcomings you let flow under your due diligence bridge unmolested.

I can’t believe I have to say this again: Read the specimen contract and find the flaws! If you cannot guarantee benefits, and hopefully premiums, I must ask, “What were you thinking?”

Let’s approach this calmly and rationally. Your client has agreed to buy protection against the possibility of the need for expensive extended care. It seems fairly clear that you should at least explain what that does cost. If you didn’t pay for it, it seems reasonable that there might be questions as to the validity or quantity of ultimate claim payments. I further suspect nothing should bring you in close contact with nothing, or not much, at the time of claim. Paying a known cost for a known benefit does seem to be a much safer approach. Why not take a hard look at what that net cost actually represents. Please divide the premium into the rider cost. The results might surprise you and be very illuminating to your customers. Most long term care/chronic illness claims are manageable. Doesn’t it strike you that the cost to protect a risk of that magnitude should also be manageable from a cost standpoint?

Why can’t we do this right?

You are at a fork in the road. One direction is a well-lit, newly paved toll road. You know where you are going. You know how long it will take to get there and exactly what it will cost to arrive. The other road is overgrown, dark, with unseen potholes and a dubious end to your desired journey. Again, forgive me…I just can’t see a more obvious decision. A baby pig is in a gunny sack. It can be seen moving and heard squealing. The problem, of course, is that we already know it’s probably the runt of the litter, but it is unknown just how deficient is its size and growth potential. Out here in the country we would not ever buy a “pig in a poke” or frankly have anything kind to say about those who sell them.

Other than that I have no opinion on the subject.