Get out your financial calculators, spectacles, and your pocket protectors because we are going to have some fun with this column. We are going to create a product. Of course I am being somewhat facetious because there’s much more that goes into “creating a product” than just the numbers, such as: Non-forfeiture requirements, state filing, illustration parameters, surrender charges, MVAs, utilization rates, etc. I do not pretend to be an actuary, but I am about as “actuarial” as a sales guy can be. My wife tells me that’s like being the tallest elf.

Regardless, this elf is going to show you the not-so-basics of creating an indexed annuity with a “cap” based on today’s (October 7, 2022) interest rates and options prices. The purpose of this is to not make everybody into actuaries but rather to enable you to easily answer many questions about these products by having a deep understanding of how they are created.

Here is the product we—the insurance company—are going to create. This will be a 10-year indexed annuity that utilizes an annual reset S&P 500 strategy. This strategy has a “cap” that we will need to figure out based on today’s interest rates and options costs. This product will have a seven percent commission to the agent. Furthermore, we—the carrier—have shareholders that require a “return” on the company’s capital to the tune of eight percent (more on this later).

Agenda:

- Determine how much we, the insurance company, can get in yield when we invest that client’s money.

- Based on our IRR requirements from the shareholders, how much of a “spread” do we shave off the top of the yield that we are getting in bullet point number one above.

- We then take what is left of the difference of number one and number two above and that determines our call option budget.

- We take our call option budget, and we buy and also sell call options based on today’s option prices. Based on the pricing of call options, you and I will be able to identify what cap rate a person can get in today’s environment. Sounds pretty cool huh?

1: How Much Yield Do We Get?

First off, when a carrier takes a client’s $100k (example), that carrier will invest almost all of that money in the bond market. Although a lot of folks use the 10-year treasury as “the benchmark” for the yield rate, a better benchmark is the Moody’s Baa bond yield. This is because carriers generally invest more in corporate bonds than they do in Treasury bonds. Why? Because corporate bonds provide a higher yield. For instance, an index of “investment grade” corporate bonds might represent a 5.99 percent yield. This is much better than the 10-year Treasury bond that is currently yielding 3.88 percent. Thus, the reason corporates are favored over Treasuries.

Now that the insurance company knows that it can invest their money and earn approximately six percent on this money that is going into their “general account,” the carrier needs to allocate that money between the bonds and the call options. The bonds will be purchased to guarantee the money grows back to $100,000 every single year, regardless of what the S&P 500 does. This is how the carrier is able to support the policy guarantees. The call option chunk will give the indexed annuity the “link” to the stock market in the up years. Again, Bonds=Guarantees and Options=Upside.

2: The Carrier’s Cut

Before we calculate how much money goes to bonds and how much money goes to the call options, the carrier takes their cut… This is where the “carrier spread” comes in. That is, the carrier shaves a little off the top of that six percent (technically 5.99 percent in our example). That “spread” is how the carrier makes money. How much spread does the carrier require? It depends…

Our carrier has shareholders that require them to make a certain amount of money on the carrier’s capital. And make no mistake that putting a case on the books costs a carrier capital. Afterall, the carrier has to pay for the administration, paperwork, and the big one, agent commission. This is why if you have ever seen a carrier grow “too fast” they will shut off new sales.

There are various measurements on the amount of money the carrier makes off their investment, such as Return on Investment (ROI) and Internal Rate of Return (IRR).

To simplify this, let’s say that we, the carrier, pay $7,000 to put our $100,000 on the books, or seven percent. This is simplified because our agent commission is seven percent and there are technically more expenses than that but bear with me! If the carrier shareholders demanded an eight percent internal rate of return over the 10-year life of our product, what annual income would be required for the carrier to achieve that? If you put this in your financial calculator, it would require $1,043 per year to the carrier (PV=-7,000, N=10, %=8, FV=0, solve for PMT). In other words, by the carrier “investing” $7,000 of their own money, in order to get an eight percent return over the 10-year life of the product, that carrier would need 1.043 percent ($1,043) off the top of our six percent. Hence, a spread of 1.043 percent. (Note: In corporate finance you learn that if the IRR is greater than the carrier’s “cost of capital,” it is a project that is worthwhile. Hence, if a carrier borrows money at six percent and gets an IRR on that money/capital at eight percent, that is a product that has a positive “Net Present Value” and is good!)

For our example, let’s simplify the above and say that the carrier’s yield is six percent and the carrier spread that is required to keep the shareholders happy is simply one percent. No need to get crazy here with the decimals.

3. Calculating the Call Option Budget

After the carrier takes its one percent off the top, we have five percent to play with for our client and their $100,000. This is where we need to divide the money between the bonds and the call options. The bonds need to guarantee $100,000 at the end of every year to—again—support the policy guarantees. So, what dollar amount needs to go into the bonds—earning five percent—so that those bonds in the general account grow back to $100,000 at the end of the year? Hint: The correct answer is not $95,000! The correct answer is $95,238. Thus, if you add five percent to $95,238, you will get $100,000. So, if the insurance carrier is investing $95,238 in bonds, what are they doing with the other $4,762? Call options. We have arrived at our call option budget.

Review:

What have we done so far? So far, we have designed the commission level on the product at seven percent. We also calculated how much the carrier needs in spread to make the shareholders happy, and we have also arrived at our call option budget of 4.76 percent that will soon determine the cap. (Note: All of these calculations revolve around the interest rate of six percent—technically 5.99 percent. This is why indexed annuity pricing has gotten better over the past year.)

4. Buying and Selling Call Options to Arrive at Our “Cap”

So, we have $4,762 to buy call options that link our client’s $100,000 to the S&P500. That is a call option budget of 4.76 percent of our $100,000. So, the first thing we want to do is look at the prices of call options on the S&P 500 (SPX). We want this call option to give us all of the upside of the S&P 500 between now and 12 months from now, because our product is an “annual reset.” (Note: My discussion is going to be largely about percentages. The exact dollar amounts to link the client’s $100,000 would be just a function of buying multiples of what we are talking about below. The exact dollar amounts are not important. The call option budget percentages are important.)

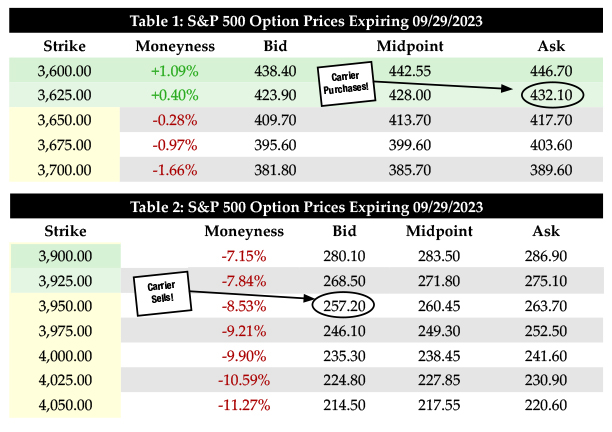

Table 1 represents five rows—out of hundreds of rows—that represent today’s (10/8/22) option prices for an S&P 500 option that expires approximately one year from now. Because we want this option to give us growth on our client’s money from where the market is today (3,639), we need to find the “strike price” that is close to that number. In other words, we want to buy an “at the money” call option. So, we need to see what options sellers are “asking” for these options. It appears that we can buy an option for $432.10 on a S&P 500 value of 3,625. This call option represents a whopping 11.92 percent (432.10 divided by 3,625) of the “Notional Value” that is linked to the market! We have a problem here because our options budget is only 4.76 percent.

No fear, there is a solution here. That solution is that we can buy this option but then immediately sell another option that will give us back approximately 7.16 percent. This will ensure that our net options cost is only 4.76 percent. In other words, by us buying an option for 11.92 percent and selling one for 7.16 percent, our total net cost will be our options budget of 4.76 percent (11.92 percent-7.16 percent=4.76 percent).

So above, let’s buy the “at the money” option for 11.92 percent of the “notional value.”

Selling a Call Option

As you can see in the options pricing tables, the higher the “strike price” on call options, the cheaper they are. It is because the “strike price” represents the point in time where the option purchaser actually starts making money. Hence, “in the money.” So, if we are selling a call option, we want to go as far down the “strike price” as we can. This is because when the market increases to that number, that is the point that we will be giving the upside to somebody else! Ideally, we would just purchase the option that we already did above and not have to sell a call option. However, we don’t have the large call option budget to do that, therefore we must sacrifice some upside. So, let’s go down the list and see what we need to sell. We need to produce about $259.55 (7.16 percent of 3,625) so that we net out to our 4.76 percent budget.

We found something close! We can sell an option for $257.20 at a strike price of 3,950. What does this mean?

- We netted out to a cost of $174.90 (Paid $432.10—Sold $257.20). This represents something very close to our call option budget—4.82 percent (174.90 divided by 3,625)

- We just created a product with an approximate “cap” of nine percent. This is because we are participating in the upside of the market starting at 3,625 and handing off the upside “participation” in the market once it crosses over 3,950. 3,950 is approximately nine percent (8.97 percent technically) higher than 3,625.

What we have just done is created an indexed annuity that:

- Guarantees the client’s money will never be lost. This is because the carrier has the bonds that grow back the money to $100,000 every year, assuming rates stay the same.

- Gives the shareholders their IRR, assuming rates stay the same.

- Gives the carrier a 4.76 percent call option budget to buy the call options after they expire every year, assuming rates stay the same.

- Gives the carrier upside potential of nine percent that they can pass through to the client in the form of a “cap.”

- Pays the agent a seven percent commission.

Although my calculations are my own calculations and not specific to a carrier, the product I just explained with those caps, commission rates, etc, really does exist today. So, those calculations are not pie in the sky.

Technically, one of my favorite products is the same as what I laid out here, except the A-rated carrier just announced a cap increase to 10.5 percent for premiums over $100k! How can they do that? Numerous ways. Maybe the carrier is demanding less spread for themselves. Or maybe the carrier is able to get investments at higher yields than my six percent. Both of these would mean more call option budget.

I am fully cognizant that this was a three-coffee article for you to read, but I promise you, if you are serious about indexed products, this article will help you in the future when it comes to answering questions about “How do the carriers do it?.”