HomeAuthorsPosts by Charlie Gipple, CFP, CLU, ChFC

Charlie Gipple, CFP, CLU, ChFC

118 POSTS

0 COMMENTS

Charlie Gipple, CFP®, CLU®, ChFC®, is the owner of CG Financial Group, one of the fastest growing annuity, life, and long term care IMOs in the industry. Gipple’s passion is to fill the educational void left by the reduction of available training and prospecting programs that exist for agents today. Gipple is personally involved with guiding and mentoring CG Financial Group agents in areas such as conducting seminars, advanced sales concepts, case design, or even joint sales meetings. Gipple believes that agents don’t need “product pitching,” they need mentorship, technology, and somebody to pick up the phone…

Gipple can be reached by phone at 515-986-3065. Email: cgipple@cgfinancialgroupllc.com.

Last month as I was driving to the grocery store, about a mile up my road the police had completely blocked it off. This may be a common thing in a place like New York City, but in the suburban area of Johnston, Iowa, something bad had obviously happened. A couple of hours later my 18-year-old son learned that one of his classmates and basketball teammates had rolled his car off that road and he (Jok) was in the hospital. The road was not a highway. On the contrary, it had a low speed limit without any intersections, etc. So, we assumed that he would recover from whatever minor injuries he had and be perfectly fine, possibly the next day.

The next day we woke up and my son said, “Jok died.” How he died and how he crashed was irrelevant to us. It was shocking! Even though my son did not know him very well, when an 18-year-old–who had just graduated high school and his life had just begun–dies unexpectedly like that, it sends a shock wave through your heart. The thought of any “kid” dying sends a shock wave through your heart. You all know the feeling. Everybody said he was a great kid with a great family that is obviously devastated.

As somebody who has spent 25 years in finance and insurance, outside of the sorrow that I felt, you know my next tendency. My next tendency was to hope that the family had the resources or had made the preparations to weather the expenses, time off work, grief counseling, etc., that they will soon have to navigate.

Alas, as we all have seen many times, the GoFundMe page popped up a couple of days later. My wife shared it with her friends on Facebook, and I asked her what the situation was. Unfortunately, this situation was similar to many situations that you and I have seen over the years. The family did not have $8,000 or so in cash to pay for the burial services and they were seeking funds from family and friends to help cover the expenses. $8,000 was the “goal” on the GoFundMe page. And again, as we have seen over and over, there was no life insurance on this fine young man. I was, however, pleased to see that the community was generous enough to indeed reach that $8,000 goal.

There are better ways! As I sit here writing this article, I ran the numbers on a $50,000 life insurance policy for an 18-year-old healthy kid, and it is less than one dollar per day, $344 per year. Again, that is for $50,000 in tax-free life insurance coverage, which would go a long way toward covering many expenses in addition to the burial.

This is not a statement about this young man and his family, but a statement about the public in general. Here is the great paradox. The paradox is that my son’s classmates (and my son) all walk around with $200 basketball shoes, $800 apple headphones, $1,000 iPhones, Nike “Elite” sports attire, etc., but yet many of them are uninsured. Being uninsured is fine as long as the resources are there if–heaven forbid–tragedy were to ever happen. However, you and I both know that the average American could not financially handle an emergency needing $1,000, let alone $10k, $20k, $30k etc. Expenses like this are financially catastrophic to many Americans. There are solutions for helping with “catastrophic” situations like this.

Instead of $800 Apple headphones, why would parents not spend one dollar a day to address the risk of this horrible possibility? Because in many consumers’/parents’ heads, the death of a child seems so unfathomable and so far out from realism. It is just not a thought that ever enters their heads, because it is too uncomfortable. This is why it is so important for you–the financial professionals–to do what you do. We all need to tell stories like this and convince them that it is indeed a possibility, even if it makes them uncomfortable. So, keep up the good fight. People need you.

On a bit of a technical note, when it comes to the carriers’ underwriting of life insurance policies on the kids, it is a common practice that the carriers will require that the parents

have at least double the life insurance coverage on themselves for whatever dollar amount of coverage they are getting on the children. For example, if I am getting $50,000 in coverage on my son, I better have at least $100,000 in total coverage on myself. The carriers have this stance because if the parents do not believe in life insurance for themselves, then why get so much on the kids?

Annuities have had three consecutive years of record-breaking sales throughout the country. Consumers are purchasing annuities like crazy… The annuity business is now almost a half a trillion dollar a year business! For consumers that are in the retirement red zone–as in 5 to 10 years before and after retirement–and cannot afford to lose their money due to the stock market but want more upside potential than things like CDs, annuities may be for them. Furthermore, for consumers that want to replicate the guaranteed lifetime income that their beloved pension plans and Social Security provides them, annuities may be for them.

However, even after these huge years for annuities and the fact that consumers that bought annuities are generally happy with them, there are often fear tactics that advisors will communicate to clients when it comes to annuities. The amount of harm done to consumers’ retirement readiness as a result of misinformed “advisors” stating that annuities are bad is beyond measure. There are a few reasons that you have a large group of advisors that will tell their clients that annuities are bad.

Lack of understanding: Many times, the advisor will cite two different things to the consumers to state that annuities are bad. The first is “high fees.” These advisors once upon a time witnessed variable annuities that did indeed have extremely high fees. Twenty years ago, for example, it was not uncommon to find a variable annuity with total fees of 3% to 4 1/2%, which is crazy. However, the world has changed! Variable annuities are now just a minority share of the total annuity business. Now, many annuities have little to no fees. But again, these advisors fail to understand this because they have been living two decades in the past and they have failed to keep up with an extremely fast evolving industry.

Another area of the “misunderstanding” is where the advisor will tell the client that he/she “will lose all control of their money” once they start taking income payments. This is a common fear tactic and again, a result of the advisor living decades in the past. Once upon a time, the only way to get guaranteed lifetime income from an annuity was to “annuitize” the annuity value. This did indeed mean that the control of the money was essentially forfeited. It also meant that the death benefit to the beneficiaries could be limited, or nothing! However, times have changed, and the most prominent way that annuities generate guaranteed lifetime income today is through something called “Guaranteed Lifetime Withdrawal Benefits,” which is very much different than “annuitization.” For instance, with the guaranteed lifetime withdrawal benefits, the consumer is not forfeiting all their control. If they choose to stop the payments, they can. If they choose to cash out the annuity, they can. (Note: There can be surrender charges depending on the year he/she cashes out the annuity.) Also, with these benefits, if a consumer has triggered their lifetime income and only taken one payment, for example, but dies after only one income payment, the beneficiary gets the balance of their accumulation value! It is not like the company “keeps all of their money” if they die, which again is a common misconception.

Gaslighting: For every one advisor that doesn’t understand annuities as I discussed above, there is an advisor that does understand annuities but will still cite the reasons above to stay away from annuities. Why would the advisor be disingenuous like this? Because advisors generally get paid on the assets that they manage. For example, there is one large company that almost invariably charges 1.35% on “assets under management.” Paradoxically, this is actually a remarkably high fee compared to the national average, but I digress. That means that if a consumer has $1 million with that company, then that advisor will be charging $13,500 every year. If you were to move $500,000 out of that company into an annuity, they would lose $6,750 per year. Naturally, these advisors do not like it when money leaves from under their umbrella!

Rosy stock market numbers: Advisors will often cite that because they have a secret formula for the clients that will grow their portfolio by X percent, then by moving money into an annuity the consumer will be missing out on the opportunity for that huge growth. In economics we call this “opportunity cost.” That is, the lost opportunity by moving your money into an annuity in our example. Again, citing 10%, 12%, etc. returns is a tactic often used when the advisor does not want to lose the assets under management. Now, it is undeniable that the United States stock market has done well over the long run. Over the last 100 years large company stocks have averaged about 10% annually. However, you cannot apply that same “100 year” performance to your portfolio if you are in that “retirement red zone.” You don’t have 100 years! Over the long run, the market may do X, but over the short run it can do anything. Also, “averages” don’t matter when you are taking withdrawals because of sequence of returns risk!

Furthermore, and most importantly, let’s play the advisor’s game and assume a rosy stock market. Even assuming a rosy stock market (to a certain extent), the income generated from an annuity oftentimes will eclipse the stock market alternative. When you plug an annuity with a guaranteed lifetime income stream into the same software that the advisors use to model your portfolio performance, you’ll find that many times the annuity enhances the amount of income that the consumer can take in retirement years. Again, even if we did assume that the stock market was going to perform excellent! How is this? Because the guaranteed annuity payments are so high that they oftentimes cannot be replicated by the stock market unless one assumes outrageous stock market performance.

How do I model out what I just said in the previous paragraph? By using “Monte Carlo simulations,” which is the same software that your advisor uses when he explains to you how by keeping your money in stocks and bonds that he will be able to generate X amount of income during your retirement years. If the advisor took the time or had the knowledge to incorporate an annuity into that same analysis, that advisor would be sold on annuities. But alas, annuities won’t provide him/her (the advisor) with a perpetual 1.35% income stream.

To sum this section up, be leery anytime an advisor says they can outperform what an annuity can do, especially if they are throwing out long-term “averages” on the stock market! And remember, by using the same Monte Carlo analysis that the “advisor” uses, we are often able to demonstrate how there is additional wealth that is generated by incorporating an annuity.

I will often hear from a client that there is another advisor throwing shade on my annuity idea. I take this personally. Not because I “need” to sell an annuity. I am at the stage in my career where any one sale will not change my life. I take it personally because the amount of harm done to consumers by being told that annuities are bad is beyond what we can measure. This is not good for our industry and most importantly, not good for retirees!

So, I will often volunteer for a three-way call with that advisor and the client. Facts, math, science, and numbers that I use are difficult to argue against! And my math science and numbers are widely accepted. Monte Carlo for instance. I know that once I get on a call with that “anti-annuity” advisor, there is no way that client will be led astray by that advisor who is desperate to not lose the assets. By the end of the call, 95% of the time the advisor concedes that the annuity scenario is a good strategy. I am not saying that annuities are for everybody or for 95% of the population. I am just saying that if I recommend one to a client, there are the facts, math, science, and numbers that indicate that for that specific client, annuities would benefit them.

Again, facts, math, science, and numbers do not lie and there is an exceptionally good chance that that advisor does not know the facts, math, science, and numbers like I do. Hence, his/her naivety around annuities. The advisor is entitled to their own opinions, but not their own facts, math, science, and numbers.

I was scrolling through my LinkedIn feed and came across a conversation that one of my friends was having with a lady whose profile said she was a CFP® and also a “Fee Only Advisor.” What were they discussing? Annuities! You veterans know how this conversation was going with a “fee only advisor” discussing annuities! This conversation did not disappoint. Below is one of the responses the fee only advisor made, literally cut and pasted:

“Most of them (annuities) never made sense to me. If a client has plenty of assets, the guaranteed lifetime income option would never be used because almost 99% of time you will have to annuitize the annuity. If a client has limited resources, very few choose to go with the guaranteed income option either because you lose the access to the lump sum, which is risky in its own way too. In rare situations, it might make sense, depending on the clients overall asset and income level. To be honest, I’ve only seen 1-2 clients in retirement really annuitize the annuity for guaranteed lifetime income. The majority of them use free withdrawals and kind of treated it as poorly performed investment account. Most of the time, annuities, especially fixed/fixed index were sold to investors who are scared of market ups and downs with very high commissions.”

The above is exactly the talking points that we have all seen from folks like her–anti annuity and usually “Fee Only” advisors. And these talking points are misinformed.

Now, on a website (LinkedIn) where many professionals come together to learn from others, I would typically find this commentary very benign. Afterall, none of us know everything about everything. However, you and I deal with this crap every week coming back to us from our clients that had been communicated to them by another “advisor”! You and I both know that this “Fee Only Advisor” communicates this misinformation with their clients every time the annuity conversation comes up. As a result, this misinformation is perpetuated and consumers that need annuities are now convinced that annuities are bad. So, to folks like this: It is OK to be ignorant. As a matter of fact I will help people like her overcome her ignorance on annuities because that is what I do. However, communicating this same ignorance to clients is very harmful.

Where is she wrong? First off, most annuities that are offered to clients for guaranteed lifetime income are not offered with the intention of annuitizing the contract. Annuitizing the contract does indeed–as she said–forfeit a good amount of control. Furthermore, the most prominent lifetime Income annuities today have “Guaranteed Lifetime Withdrawal Benefit” riders that are merely withdrawals from the contract that are guaranteed to last forever, even after the accumulation value hits zero. If one dies before spending down their value, the balance goes to the beneficiary. If one wants to cash out at any time, they can. Beware of surrender periods however. This “Fee Only Advisor” is living 25 years in the past when GLWB riders didn’t even exist and “lifetime income” was achieved only through annuitization (GMIB riders for xample).

I also love it that somebody who is likely charging her clients 1% to 1.5% on assets into perpetuity is citing “high commissions” on annuities. Over a 10-, 15-, or 20-year period of time, she would have likely charged her clients multiples of what the commissions would have been on an average annuity.

Don’t Be a One Trick Pony

Lastly, I love the stock market because “over the long run” there have been very few vehicles that have created as much wealth as the US stock market. However, I also love index annuities with GLWB riders. With that, I view our obligation to our clients to not be a one trick pony.

For instance, for a 46-your old client, many securities professionals (Note: I am an IAR myself) would say it would be completely stupid for that client to have any of their money in an annuity with a guaranteed lifetime withdrawal benefit. They would say that over the “long run” the stock market will accumulate to a value so large that the resulting income at retirement cannot be replicated by an annuity.

That thinking is actually false in a majority of the situations. This is where I would punch the data into my simulations (Monte Carlo) and illustrate what a guaranteed lifetime withdrawal benefit would provide this 46-year-old at say age 65 and compare that to even some fairly rosy stock market assumptions. Well, even while considering rosy stock market assumptions, if the annuity with a guaranteed lifetime withdrawal benefit is projected to provide more lifetime income, then why wouldn’t that 46-year-old put a chunk of their money in an annuity?

The Fee Only Advisor would likely say that I am just trying to rip off that 46-year-old client by giving them a bad product so I can get my “big fat commission.” Well, that Fee Only Advisor will have a tough time with that one because last year it was me that was that “46-year-old client.” I did this analysis on myself and bought that index annuity for $200,000. Did I rip-off myself? Nope. In fact, that annuity will provide me and my wife with $44,000 per year income at my age 65. Joint Income! That is important because my wife will likely live forever. With my genetics, on the other hand, I don’t even buy green bananas anymore. But I digress.

If I can demonstrate that the income in the annuity exceeds what a rosy market projection would do, the only objection left that I can see some “Fee Only” rep giving me is, “But with my wizardry, I can manage your money and give you an even rosier stock market scenario versus the already rosy scenarios you ran. And by the way, I am a fiduciary.” Puke! Ignorance is bliss, unless you are sharing your ignorance with consumers. Then, that is not bliss, that is flat-out harmful. If you are a “Fee Only Advisor” then don’t be closed minded and have an annuity “agent” you can refer your clients to if those clients need an annuity. Conversely, annuities aren’t for everybody! So, if you are “insurance only,” it may be smart to have a Registered Rep or an RIA/IAR where you can refer business to.

This intentionally idiotic title has many of you saying, “Because he’s 31 years older than Jake Paul! Duh!” Of course that’s true! However, I would argue that even if Mike was still in his 20-year-old body today, that his mindset would inhibit his performance versus who he truly was 40 years ago. Allow me to explain and then draw a corollary to our business.

As I write this article I am somewhat disappointed that I wasted my Friday night watching this very boring Tyson vs. Paul boxing contest on Netflix, even aside from the technical glitches! However, the ladies fight was a great match. But I digress. I had hoped that Mike Tyson would knock out Jake Paul. I like Mike Tyson as he gets older, and he is the GOAT (greatest of all time). However, I have been a realist and understand that Mike Tyson is 58 years old, and Jake Paul (at age 27) is in the prime of his life physically. Father Time has an undefeated record. And Jake Paul is actually a great athlete not to be taken lightly! My friends thought I was crazy when I said that Jake Paul was going to win, much to my chagrin. Jake did indeed win by unanimous decision.

(Note: Many folks believed the match was “rigged.” Whether it was or not is not the point. Either way, my comments below are hard to deny.)

Me believing that Mike Tyson was not going to win had less to do with his physical abilities and more about his mindset as he has aged. Afterall, I have recently seen the training videos where he’s still destroying the heavy bags at lightning speed. Those training videos led many to say, “The old Tyson is back, and Jake Paul is in trouble!” I never bought into “Mike Tyson being back.” My lack of confidence in Tyson was not because of his aging physical abilities, but because his body language is completely different than what it used to be, which is insight into his psyche that used to drive him to knock people out. Again, what drove Tyson to kill his opponents when he was 20 years old was just as much about his psyche as it was his physical abilities, although his physical abilities were clearly superior. (I am obviously not a psychologist, but here is my view.)

In short, Mike Tyson does not have the killer instincts like he used to, even though leading up to this fight he convinced millions that “the old Mike is back.” Wrong! His body language, whether at the weigh-ins, photo sessions, on his way to the ring, or even while he is in the ring, is not as laser focused on his prey as the 20-year-old Mike was.

Thirty years ago, as he was entering the ring, or already in the ring, he only looked in one of two directions: Directly at his prey, or to the ground as he was contemplating how he was going to destroy his prey. It was internal, deep down in his gut. He wore all black, not looking around at what others were saying about him or cheering about. You knew that he was internally processing (maybe in an unhealthy way) what he was going to do to his opponent and how he was going to achieve his goal. He was hungry.

Today Mike’s body language tells me that he has lost this mindset when it comes to boxing. As far as body language, it is almost like Mike Tyson has become more concerned about other things than just achieving the “goal” of knocking somebody out. He’s looking around at his surroundings and not so much laser focused like a lion about to attack a bunny rabbit. When they ask for his commentary on what he is going to do to his opponent, he kind of shrugs his shoulders and says something fairly benign and non-convincing, almost like he doesn’t believe it himself. The 1980s and 1990s Mike Tyson made comments that you know he believed in his heart and gave some of us children nightmares. Do I dare say that today’s Mike Tyson seems self-conscious? Or certainly more “conscious” of things other than destroying his opponent.

However, why should he really want to absolutely kill somebody? Afterall, he has hit the pinnacle of the business, made millions of dollars, and has nothing to prove to anybody, certainly not to a 27-year-old kid (Jake Paul). He has become domesticated. Sometimes already hitting your “goals” will make you domesticated.

I bring all this up because once you have achieved high levels of success in our business and hit your “goal” you can become “domesticated.” Hence, the reason why we should continue to make new goals. I launched CG Financial Group, an IMO for independent agents, six years ago. As time has gone by, I hit a lot of goals that I set for my business. Every time I hit a goal, there was an inclination for me to say, “Let’s take a little break because I’ve earned it.” The fire burns out a little. This is called getting “fat and happy,”

Because I try to self-reflect a lot, I know when I am feeling “fat and happy” and therefore have made conscious efforts to quickly remedy this mindset along the way. You cannot let yourself get fat and happy, at least when it comes to doing something that you want to continue to grow. Naturally, Mike Tyson is a 58-year-old guy that no longer wants to beat people up, which makes it OK for him to be “fat and happy.” Conversely, I bet when it comes to your business and your growth aspirations, you do not want to get “fat and happy” and stagnant.

I have found that setting continuous goals and extending out the goal post is important for me in order for me to not become “domesticated.” Feeling “uncomfortable” is needed. If you continue to set goals for yourself and have a laser focus on that prey/goal, it is impossible for you to lose your edge. Again, I’m not suggesting that Tyson should be obsessed with being the world champion again, I’m just drawing the psychological corollary to why Tyson is not as “good” of a boxer as he used to be, aside from the fact that he is forty freaking years older!

When it comes to setting and hitting your goals, be that 20-year-old Tyson, don’t be self-conscious, don’t care about what those around you are saying about you, don’t get comfortable, don’t get “fat and happy,” and keep moving forward.

As an Independent Marketing Organization, I have never been more excited than I am now to be in this business. What is “this business?” Helping our agents help their clients with annuities, life insurance, and long term care.

Today the oldest baby boomer is 79 years old and the youngest is 61. Yes, I know! Another baby boomer statistic! Every time I hear the tired statistics of a baby boomer hitting retirement age every X minutes, I am reminded of the story of the Irish band, U2, playing in Dublin. Their lead singer, Bono, stopped the show and started clapping very slowly and firmly. He then emotionally yelled to the crowd, “Every time I clap my hands, there is a child in Africa that dies.” At that point somebody yelled from the crowd, “Then stop clapping your damned hands!”

Although I poke fun at the constant baby boomer statistics we hear, there is merit to it and I see it every day. The number of 401k/IRA/CD/etc. transfers is much more prominent than I have ever seen. Furthermore, the dollar amounts are larger than I have ever seen. Reading statistics in the news is one thing, but actually experiencing the statistics is eye opening. I am witnessing the “opportunity snowball” getting bigger and bigger as time goes by!

The wealth that is moving around is huge! Baby boomers own over 50 percent of our country’s wealth: $80 trillion. With annuity sales, I remember when $100,000 in an annuity was a decent case! Now that is well below the industry average FIA sale. The annuity industry had its third consecutive record-breaking year with sales well over $400 billion! With long term care sales, I used to be paranoid while presenting a $20,000 per year long term care premium to a client, thinking they would pepper spray me after hearing the number. Then, I realized that many times they understand the long term care risk and therefore don’t blink an eye with that size of premium. What about life insurance? I don’t need to tell you that life insurance is one of the most efficient ways for these baby boomers to pass on wealth and offset taxes for the next generation.

Offering the above three product lines, annuities, life insurance, and long term care should excite you today! These three products can be viewed as helping your clients in chronological order:

Stage 1, Annuities: The annuity helps them once they hit the “retirement red zone” to protect their money and/or guarantee a lifetime payment stream.

Stage 2, Long Term Care: Later in life there is a 7 in 10 probability you will have a long term care event. Whether the client has non-qualified money or is all “qualified” there are solutions available to leverage those dollars.

Stage 3, Life Insurance: Passing on a tax-free death benefit to the next generation.

I also look at the baby boomer statistic (10,000 baby boomers per day retiring) a little deeper. Many of those baby boomers retiring are also your competition, other agents! The average agent is over 60 years old. Some are retiring and some will stick around. For those sticking around, the opportunities are huge. All of this wealth moving around will be left to fewer advisors/agents to manage. This should be exciting if you don’t plan on retiring anytime soon.

With all of the above said, here are the opportunities in product as well as practice management that you can leverage:

Annuities: With where interest rates have gone, accumulation indexed annuities have S&P 500 caps in the double digits! For guaranteed income (GLWB) annuities, the payout rates have never been higher.

Long Term Care: Today over 90 percent of the long term care business is in the “hybrid” space. That is, annuities/LTC hybrid and life/LTC hybrid. Work with your IMO, like yours truly, to understand these awesome products. For instance, there is a product where you can move over qualified money into a hybrid long term care policy. How do we do that with pre-tax money? That is a conversation for another day.

Life Insurance: Carriers are getting much better with accelerated underwriting and the rest of the application process. This will continue to improve your experience and the client experience.

Technology: Related to #3 above, whether annuities, long term care, or life insurance, the E-App solutions that exist are fabulous and continue to get better! Doing away with paper apps can be a way to literally cut your time dealing with paperwork by 75 percent.

Volatility: I as well as many Wall Street money managers believe that 2025 is going to be a volatile year in the stock market. Volatile markets are almost always good for fixed and indexed annuity sales. Watch for the volatile markets and call your clients when they happen.

Seminars: Seminars are back after the COVID fiasco! My IMO is getting registrants to seminars for less than $25 per household. That means for $1,000, you should have 40-50 registrants! Gone are the days of buying pallets of “mailers” of which 99 percent will go in the trash! There are more efficient ways to market for seminars. CG Financial Group has mastered this process. Three seminars that are very popular are: Social Security, Long Term Care, and Estate Planning.

Virtual Meetings: The nation is now your playground, versus just your local area. Consumers are embracing Zoom calls more than they ever did. This means that you are no longer confined to just marketing in your local area. Learn best practices in selling virtually.

Planning Software and Processes: I believe that consumers like buying into “processes” more than “products.” In other words, if you have a process that the consumer can go through in various steps that incorporates software with nice visuals, you will build credibility and trust. Of course, the product is plugged into this process. Selling a product is often transactional. Selling a process is often consultative and nurturing. CG Financial Group has some remarkably successful agents that will walk a consumer through a process that takes five to eight meetings/calls. Sound tedious? Well, in the end, they are getting $1 million plus annuity sales quite consistently.

Social Media: In a world where social media “influencers” are becoming more prominent than Hollywood movie stars, why would you not leverage the same apps to be a financial “influencer?” By leveraging social media, you have the ability to market to millions of consumers, for free. Make videos. And while you make them, remember, perfection is the enemy of progress.

Work with your IMO: Many agents like to “go it alone” without realizing that a good IMO can help you in areas you never thought of. There is so much innovation taking place that what we all knew last year is almost outdated this year. Things are moving quickly. Work with your IMO to keep up to speed, and be coachable.

Fortunately, I am extremely optimistic as I see more opportunities in this environment than I do challenges. However, if I were to think of our next year and the challenges that may arise, I would point to a few areas:

Interest Rates: We have been spoiled lately, and I do not want us to go back to 2015-level caps and participation rates. However, it is always a relativity game. As in, annuities will almost always be higher than CDs.

Inflation: Everything is so dang expensive! For agents to stay in business, they need to be smart with their money, especially right now.

Regulations: New administration or not, our industry has always headed toward a more regulated and more litigious industry. So, take good notes in client meetings and get a CRM (Customer Relationship Management) System to keep track of correspondence.

Paperwork: Related to #3 above, paperwork with all three product lines (annuities, life, long term care) is only getting worse. As are the carriers’ requirements for the annuity suitability forms to be perfect… Again, e-applications can change your life!

Anti-Insurance Sentiment: With the recent killing of the United Healthcare CEO and also with many folks that were impacted by the California fires complaining about insurance companies, I am concerned about the reputation of “insurance” and “insurance companies.” We all need to continue to tell our success stories in order to offset the negative stories. [CG]

My dad died in 2006. Although my dad had many flaws, to me and my brother he walked on water. He was incredibly good to me and my brother growing up and taught us how to hunt, fish, cuss, deal with life’s ups and downs, and taught us a relentless work ethic. He owned an underground construction (water, drainage, sewer), and concrete business and was one of the toughest guys that I’ve ever known. He worked every day until he died at age 62, which was in 2006.

Anyway, if you know his blue-collar hard headed type, you know that sometimes evolving with the times can be difficult. For instance, I was telling my wife the other day that if dad was still alive during the height of the Covid pandemic where there were vaccine mandates, mask mandates, etc., that I’d be very curious how he would have fit in. You know what I’m talking about. That’s not a political statement; it’s just me saying that he probably would not have “complied” very well because he had strong and independent beliefs, but you always knew where you stood. You know the type of person I am talking about.

This type of person often gets stuck in their own ways. Again, he had his flaws as many of us do! However, as I grew older, I realized that my dad was a much smarter and a much more complex guy than what meets the eye. For instance, I was immensely proud of him when I learned that he had actually bought a laptop computer as well as a sewer pipe camera, where instead of having to dig up sewer lines to see what the issue was, he used technology! Go figure. It was actually a fairly sophisticated set-up 20 years ago, whereas today you just buy something and “Bluetooth” it to your phone. He bought a van where the TV, laptop, electrical wiring, etc. were housed. It looked like an FBI surveillance vehicle, not that I know what that looks like. As a guy who dropped out of high school to start his own business, he was now using computers and fairly sophisticated equipment! It was crazy to me that somebody as hard headed as him would get out of his comfort zone to learn modern technology when before this his giant calloused fingers had never even touched a computer keyboard. But he understood that he had to adapt with the times or be a victim of “creative destruction.”

I’m writing this article because I was reminded of this with the East Coast “Port strike” that took place in early September. It has been “sidelined” for 90 days while they negotiate. I’m not going to give my opinion on anything other than the “automation component” of the strike.

One of the items that the union is requesting is that the port employers do not automate the docking/undocking functions. Naturally, by automating this would mean that computers and machines would replace the jobs of the employees. Well, if using computers and machines is the more cost effective and efficient way to do it, then I find the demand of not automating very far-fetched. In a capitalist society, for somebody to request that employers turn a blind eye to automation—which is equivalent to attempting to halt aging—is a crazy request.

Automation is inevitable. If the employers do not automate, then there will be other similar businesses that will open up, they will automate, and because their pricing will be better (because of a more efficient business) the non-automated companies will subsequently go out of business. At that point everybody at the obsolete company loses their jobs! Again, automation is inevitable and keeping out automation is like trying to keep my head dry with my hand in a rainstorm. The rain eventually seeps through. Automation will happen and it must happen.

How does this relate to our business? It very much relates to our business. I say this lovingly, but if you are very much “hard headed”—like me and like my dad—you might find yourself sticking to what has always worked. We hear this all the time; people stick to “what they are comfortable with and familiar with.” But is the “familiar” the most efficient? I try to force myself to get out of my comfort zone every day.

Simple example, if you are an agent that still prefers paper applications, electronic applications can shave off 75 percent of the time it takes to complete the application. That’s right, instead of an hour to complete an application, maybe it’s only 15 minutes. Go through the learning pains on the front end to be efficient over the long run.

Or what about a CRM system? Do you just have your clients stored in your memory bank? Or, are you using a CRM system that not only stores their information but also alerts you when special dates arrive? That is innovation/automation.

What about new products and product lines? Are you “stuck” with old products that you are comfortable with, or do you look to what the latest and greatest is? Annuities are better than they have ever been. Linked Benefit/Hybrid LTC products are better than they have ever been. Partner with an IMO where you can continue to learn about these new developments.

Efficiency and automation can also include leveraging what other people are doing. For instance, I have 400 agents that I work with across the country. I do monthly client webinars on long-term care planning, Social Security planning, estate planning, retirement planning, etc. I invite agents to invite their clients to my webinars where the agents are almost guaranteed appointments by the end of it, because the clients connect with what I say. If I’m already doing the webinar, why would the agents not take advantage of that? That is a form of automation/efficiency.

There are many other examples in our business that I could cite where we need to get out of our “comfort zone” so we are not victims of evolution, or on the bad side of “creative destruction.”

It’s important that we run businesses as efficient as our competitors so that we are not “automated” out of existence. I myself know how hard this is, as somebody that is “old school” in many different ways. I still read the Wall Street Journal via the paper version versus the tablet/phone version. And, of course, I love my “Print Version” of Broker World!

I once spoke to an agent that had called me up to discuss a YouTube video where he saw me discussing Annuity GLWB (Guaranteed Lifetime Withdrawal Benefits) riders and how they have never been more lucrative from a standpoint of the levels of guaranteed lifetime income that they are currently offering. He was a novice with annuities and was wondering if I could answer a few questions to help him understand how these GLWB riders worked. I was happy to take his call.

However, we got off on the wrong foot as one of the first questions he asked and the way he asked it lacked integrity. He asked me this: “Hey, just between me, you, and the fencepost, are these things really very good for the clients?” Almost like he wanted me to “come clean,” change my stance, and tell him that these GLWBs were not that good after all.

What was my response? I sarcastically said, “No, they are not. I only say they are good in all of my agent training and client meetings that I have been doing since the GLWB invention around 20 years ago because I am only trying to make money by selling snake oil.” He immediately understood that I was being sarcastic.

I then went on to tell him that if I did not wholeheartedly believe in a product or a strategy then I would not discuss it as a feasible strategy. (Note: I would hope that he would view his responsibilities to his clients the same way, but I digress.)

I tell that story because there are some that genuinely believe in what they are selling and some, well, not so much. Similar to how politicians often spout out information to tow the party line when there is no way in hell that politician actually believes what they are saying. For politicians, it’s almost like getting the vote is the end that justifies the means of telling lies. I would like to say that in finance/insurance there are no “salespeople” that view the end sale as justifying their sales pitch, even if they are “selling” something in a disingenuous way. To believe that mentality does not exist in finance/insurance would be extremely naïve.

Effectively, what the agent was asking me was, “Do you really believe in these GLWBs that you are saying are great?” My answer is, I would die before I pitched products and strategies that I did not have 100 percent belief in.

But those previous paragraphs are just words right? How do you know if somebody genuinely believes in what they are offering? If they own it themselves!

Now, I am not of the belief that you need to own a product for you to be 100 percent genuine about selling that product. I have heard that before from some folks and I think that is flawed. For instance, when I was 30 years old discussing GLWB annuities, I did not own one. I was too young to own basically any GLWB that existed! Besides, imagine if car salespeople had to own all the cars that they sold to truly demonstrate a belief in those cars. That would require a lot of money and a big garage! Furthermore, we are not always in the demographic group that we are selling to.

Well, at a ripe age of 46, I am now entering the “demographic group” of those that buy the GLWB annuities that I have been preaching about for decades. And, they have never been better from an income standpoint than today. So, what did I do? I bought a GLWB annuity because I believe in having a chunk of my portfolio in “longevity insurance.”

What we did was put a small chunk of our portfolio into an annuity with a GLWB that will provide the highest “joint lifetime payout” for me and my wife. The payouts would start around 15 to 20 years from now.

Thoughts That Went Into My Analysis. Pros and cons of buying a GLWB today.

Pro: GLWBs started in the Variable Annuity space in the early 2000s. Over that period of time, they have never paid higher levels of income than today. That is over two decades! Today’s high payouts are not the norm, but the exception.

Pro: GLWB payouts are starting to get adjusted down because of interest rates. A couple decades from now, I don’t want to look back and say, “I should have locked in some money during that lucrative time.”

Pro: The next couple of decades could be treacherous in the stock market, where I have a large chunk of my money. It would make sense to “lock in” a guaranteed income stream with a small chunk of our money.

Pro: My wife has great genetics. She may live forever! So, locking in for a “Joint” lifetime payment may be a winning proposition for us. The longer she lives, the more money she gets from the carrier.

Pro: Based on cash flow analysis, if we both live to life expectancy, we will have “internal rates of return” on the income of well over six percent. If we/she lives forever, the sky’s the limit! Six percent is not a bad “bond alternative” return.

Pro: By “locking in” with some of our portfolio, we can be more aggressive with the rest of our portfolio without worrying about financial ruin should the markets plummet.

Con: It is possible that interest rates go up over the next couple of decades and there will be better products at the time. It may have been better to wait.

Con: It is possible that our “securities portfolio” continues to do well over the next couple of decades, which makes it an “opportunity cost” to put money in a GLWB today.

Con: If we want to change our mind, there would likely be surrender charges.

Con: We will likely never run out of retirement dollars if we just left the money in a stock/bond portfolio and drew from it, along with Social Security and Pensions.

The last bullet point is important because many people believe that if you have enough money, where running out of money in retirement is not an issue, then GLWBs are not necessary. That is flawed. Even though I will not “need” to take income from the annuity 15 years or 20 years from now, I will indeed force myself to activate my income. Why? Because that is the way I would get a potential six percent, seven percent, eight percent “internal rate of return” on that money I put into the annuity. I want to get into the insurance company’s pockets as much as possible. As a matter of fact, activating income in 15 years will yield me a larger rate of return than waiting until 20 years. Will I need income at age 61? No, but I want that cash flow, like a dividend.

The balance between the “Pros” and “Cons” above is why I opted for a small chunk of our portfolio to go into a GLWB, at least at this stage in life. By the way, the balance of those “pros” and “cons” is also why carriers limit the amount of a client’s Investable Assets to go into annuities.

In part one of the series, and in last month’s edition, we discussed how it is perceived that whole life insurance is very rigid because the structure of the base policy “generally“ requires the premium be paid for the duration that the product was designed for. But then I countered that argument by discussing the various nonforfeiture provisions, the most popular one being “reduced paid-up insurance,” at least for the cash accumulation sales. For instance, one of my favorite products is a “Pay to age-75” product. However, I will often do a “seven pay“ design where at the end of that seventh year we do a “reduced paid up policy” where no other premium is required. You can also have dividends pay premiums if dividends are robust enough. So again, the thought that whole life requires premium to be paid is false.

In this article I would like to discuss very briefly the various dividend options and have a more in-depth conversation around the fifth dividend option, Paid Up Additions. In article three we will discuss term riders for cash accumulation sales and then bring it all to a conclusion with a case design example.

First, what is a dividend in a whole life policy? This is cash that is returned to the policyholder of a participating whole life policy whereas the policy holder has several options on what to do with that cash. The dividends are usually paid to the policyholder on an annual basis. Dividends represent the carrier having better experience than what was priced into the guaranteed components of the product. The three areas that can “outperform” the guaranteed components in the policy that generally make up a dividend payment are as follows: 1. Investment management. 2. Expense management. 3. Mortality experience.

Dividends are generally not guaranteed and therefore can generally be found in the non-guaranteed column of the whole life illustration. As said in the previous paragraph, a whole life policy has guaranteed provisions, but can also have non-guaranteed provisions like dividend assumptions. (Note: The guaranteed provisions in whole life are usually more robust than the guarantees in IUL. Hence, one of the reasons that one may prefer whole life over IUL.)

Dividend options:

Cash: This is quite simply where the insurance company sends the client the check representing the dividend payment. Dividend payments are generally tax-free as long as they have not exceeded the cost basis in the policy.

Premium reductions: It is possible that your policy gets to a point to where the dividends can pay the premium going forward. That would be while utilizing this option.

Accumulate at interest: This is where your dividend stays with the insurance company and accumulates at a rate that the insurance company determines.

Reduce an outstanding loan: If you have a loan against the policy, you can use the dividends to pay down all or a portion of that outstanding loan.

Paid up additions: The big one. This is where we will spend a good chunk of the remaining article because the paid-up additions dividend option is what I illustrate about 99 percent of the time for our agents.

Paid up additions: Paid up additions are not just a dividend option. This is also a rider you can choose where you can add premium above and beyond the base policy. That additional premium can purchase paid up additions. Usually, this dividend option along with allocating a large chunk of one’s premium payments to the PUA rider is what is done in high cash value cases. We will discuss more about product design in the third (of three) article.

Paid up additions are additional “slivers” of paid-up whole life insurance coverage on top of what you already have with the base policy. This is why when you look at the non-guaranteed side of the whole life illustration you will see the death benefit increasing year-by-year as the dividends purchase PUAs over time. Conversely, the guaranteed death benefit column does not increase. This is because the guaranteed side of the ledger typically does not include dividend payments. Alas, dividend payments are usually not guaranteed.

Although we discussed that PUAs increase the death benefit over time (without evidence of insurability by the way), that is not the main reason people love PUAs! They love PUAs because PUAs are like miniature single premium whole life policies. What that means is, the single premium design of PUAs beef up the overall cash value in the policy! Remember from our first article, the PUA lives by the same rules as the base policy whereas the cash value has to equal the death benefit by age 121 (usually). So, common sense would tell us that if we pay just one premium (PUA), that one premium had better start out as a higher cash value number than the “Pay to age 75” base policy. Afterall, the “Pay to age 75” base policy will have multiple premiums going in over time. As a matter of fact, the cash value as a percent of premium of a PUA payment is often 95 percent or so, depending on the client. Versus the base policy, which can commonly only have 15-25 percent of cash value in that first year relative to premium.

So then, can we just buy all PUAs and have the entire policy have immediate 95 percent of premium as cash value? No!

OK then, what percentage of our premium can we put into PUAs so that we have a cash value Machine? This will be our case study for the next article.

In addition to running an independent marketing organization where I help four hundred agents with their annuities, life, and long term care business, I also have a small group of high-net-worth clients I work with. Here, I help them with their retirement planning, estate planning, tax planning, and long term care planning. This is also where I work with securities and “assets under management” as an investment advisor. In doing so, I always pay close attention to where the current interest rates are as well as what I believe the secular trend will be.

Obviously, I am not alone here as there are multi-trillion-dollar money managers that analyze interest rates in order to buy bonds while yields are high, especially if they expect yields to drop in the future (to oversimplify). Why do they do this? Because of the inverse relationship between prevailing yields and the market value of the bond that you currently hold. As many of you know, if one holds a bond today that offers a high interest rate, if interest rates drop tomorrow, that bond would have likely increased in value leading to more wealth for the current bondholder. Bonds 101.

I mention all of this because, although somewhat theoretical when applied to index annuities and GLWBs (guaranteed lifetime withdrawal benefits), I want to share with you what goes on inside of my head when I think of the similar scenario of having an indexed annuity with a lifetime withdrawal benefit rider while interest rates decrease.

In the June edition I typed an article entitled Indexed Annuities: My Paranoia Of Product Extinction where I discussed that annuities with guaranteed lifetime withdrawal benefits are priced extremely generous today and agents and consumers need to take advantage of the current offerings while they exist. Sure enough, since then we have witnessed a few major players decreasing their payout factors on those guaranteed lifetime withdrawal benefits, for the exact reasons I prognosticate in the article. (Note: if one understands the actuarial mechanics behind these products, they can usually predict the moves that the carriers will make with their product pricing, certainly much better than how one can predict the stock market.)

Although somewhat theoretical, let’s draw a link between how bonds increase in value when rates drop and how you could “intrinsically” increase the value of a client’s retirement portfolio by putting them in annuities today with the payout factors decreasing down the road. The last few paragraphs of this article will be me giving you an example of the increased “intrinsic” wealth that your clients, who are locked into a high GLWB today, will get once the payout factors decrease as a few carriers have done.

The technical reason that bonds increase in value as interest rates increase and decrease is because of this: The market value is the cash flow that you will receive from that security discounted back to today’s date by a “discount rate.” The discount interest rate is basically just the new rate in the new environment that we are in.

Let’s use an example: Yesterday, you put $100,000 into a bond that will give you six percent ($6,000 per year) in interest on your $100,0000 investment over the next 10 years, then return your $100,000 of principal back to you at the end. Today, what is the “market value” of that bond? The answer is, it depends. If prevailing rates are still six percent today, then it does not take a financial calculator to tell you that if you discount back a future benefit of $6,000 per year, plus $100,000 at the end, then the “market value” is $100,000 today. This is assuming the discount rate/current rate is based on six percent.

However, let’s assume that interest rates decreased to 5.5 percent since “yesterday,” when you bought the bond. Now what is the market value of your bond? When you discount back that $6,000 per year income plus the $100,000 at the end by the 5.5 percent rate, $103,768.81 is the current “market value” of your bond! We are now $3,768.81 wealthier because we owned an instrument that gives us the same fixed income, even while interest rates dropped! Inflation/costs of living probably dropped as well even though you had the same $6,000 per year coming in to buy those goods and services! Of course your bond is more valuable then! (Note: Technically, the bonds increase and decrease in value based on supply and demand, but it is this bond pricing formula that is the “guiding hand” of that supply/demand.)

Now, let’s say that you are a 55-year-old couple with $100,000 and you put your money in an indexed annuity that will pay you a guaranteed lifetime payout of $15,155 per year, starting at age 65. Again, on both of your lives. Yes, this product exists right now! How long will that income stream of $15,155 come in? Statistics show that age 92 is the life expectancy of one person out of a couple. I would actually argue higher because of “adverse selection”—the notion that healthier than average people buy longevity insurance—but I digress.

When you look at the cash flow analysis, you will find that the internal rate of return on this cash flow going from age 65 to age 92 is around 6.6 percent. The internal rate of return can be defined as, “the amount of return an investment would have to return on an annual basis in order to generate that level of income.”

So, our $100,000 that we used to buy this annuity “yesterday” is going to effectively yield us 6.6 percent, based on the last person living to age 92. However, what if interest rates are such that the carrier has to drop the payouts where the new internal rate of return on new policies for the same scenario is not 6.60 percent, but rather 6.1 percent? Hence, a 50-bps decrease. What would theoretically be the market value of the future income stream on that client’s annuity? $109,646. Our annuity is now 10 percent more valuable just because interest rates decreased. By the way, what I just explained is also how market value adjustments work in increasing and decreasing rate environments.

Now, I am not suggesting that the client is techincally $9,646 richer on his/her personal balance sheet because interest rates have decreased. What I am saying is, this is a technical way to look at the value of the future stream of income they will receive. This is the lens in which the “technicians” on Wall Street view the value of fixed income assets. If there was a secondary market for GLWBs, this math is what would be utilized.

Furthermore, this is not all theoretical BS, because if you think of interest rates lowering, it is often because the costs of goods and services have subsided (lower inflation). This means that you technically can purchase more with your $15,155 payment stream than you could if rates otherwise remained the same. Hence, your annuity is more valuable.

However, for folks purchasing the annuities after rates have decreased, needless to say, they will not have a $15,155 payment stream and they will not see their “theoretical wealth” increase like those folks that got in while the getting was good!

The following analysis on GLWBs versus the Four Percent Rule has been updated to today’s GLWB offerings.

I recently saw somebody write about how we should not compare annuities to the four percent rule. Although I agree that there needs to be additional disclosures and education in the annuity part of the conversation, I disagree with not comparing the two.

Re-Anchor Clients in Reality, Not Fairy Dust I believe that consumers tend to “anchor” their retirement income expectations on the wrong thing and therefore should be “re-anchored” in reality. For instance, consumers should be educated on the fact that William Bengen’s study in 1994 showed that in order to sustain a stock/bond retirement portfolio for 30+ years in retirement, the consumer should take out no more than four percent of their retirement account balance that first year in retirement, adjusted each year thereafter for inflation. Consumers should also be aware of the new updated studies that show “rules of thumb” of 2.3-2.8 percent. (Note: When using these comparisons versus annuities, it is important to discuss that annuities generally do not have “inflation adjustments” as the four percent rule incorporates. More on that in a bit.)

This “re-anchoring” is important because many consumers know that the S&P 500 has gone up double digits on average for the last century and therefore overestimate what withdrawal rate they should utilize. They have seen the glorification of the “stock and bond” markets and have likely seen the mountain charts like the Ibbotson SBBI Chart. You know what charts I am referring to; those that show that the stock market has done double digit returns forever and that their $1 invested back when Adam met Eve would be worth enough to purchase their own private island today.

Thus, if a consumer has in their brain that stocks and bonds have always performed seven percent, eight percent, 10 percent, 12 percent, then they will tend to believe that their retirement withdrawal rate is beyond the four percent that the research shows. Even if a consumer has heard of the four percent withdrawal rule, they may have not had the math laid out for them yet that is specific to their situation. It is important to explain to those that love their stocks and bonds—as I do—that even though the S&P 500 could average 10 percent over the coming years, it does not mean they will not run out of money by taking only four percent of the retirement value from their stock and bond portfolios! How is this possible? Because of the sequence of returns risk that the stock portion can subject the client to and the low interest rates (still) that the bond portion can subject the client to. And because of these two risks (sequence of returns and low rates), a client should not overestimate what their portfolios can do as far as withdrawal rates. If you would like a graphic that helps you explain “sequence of returns risk” to your clients, email me.

To demonstrate my points in the previous paragraphs, I want to cite a study by Charles Schwab. In their 2020 Modern Retirement Survey they asked 2,000 higher net worth pre-retirees and newly-retired retirees about how much money they had saved for retirement and also how much money they expected to take from their retirement portfolios. The answers from the participants were that they had $920,400 in retirement savings (on average), that they planned on spending $135,100 per year from those portfolios (on average), and that they were generally confident in those dollar amounts allowing them to live the retirements they would like.

I would argue that a 14.68 percent withdrawal rate ($135,100 divided By $920,400) defies any retirement research I have seen! Naturally, Schwab then points out that—contrary to these participants’ beliefs—a $920k portfolio will run out in only seven years (obviously not including interest/appreciation). Clearly, these consumers should have the math explained to them. Even if the consumers understand the new “rules of thumb,” they may be experiencing cognitive dissonance that should be addressed by the financial professional. By doing so, you will “re-anchor” their expectations to the new realities of 2.3 percent, 2.8 percent, or four percent withdrawal rates, which will set you up for the annuity conversation that I will discuss.

I am not suggesting an agent go into a big dissertation on these individual studies. I just believe that going over the simplified math—specific to the client’s portfolios—based on these new rules of thumb should be done in order to show the power of annuity GLWBs. Although generous, using the old four percent rule of thumb will suffice in explaining the annuity value proposition. By demonstrating this math to the clients, you will be re-anchoring their expectations to realistic numbers. And only then do I believe they will realize the true power of GLWB riders.

The GLWB Conversation Here is what my conversation looks like (many times) that I will walk our hypothetical client through.

Let’s say our 63-year-old has $100,000 in a stock and bond portfolio. I start by discussing how this 63-year-old may have the expectation that her $100k grows by five percent or so per year between now and retirement in two years. Well, based on her $110,000 (not including compounding) value at that point, what withdrawal should she take in her first year of retirement? This is where I discuss the four percent withdrawal rule, which usually surprises them because their “anchoring” is off, as we discussed. I also discuss the reasons for the withdrawal rate being only four percent, as we also discussed earlier in this article. But then I will show her $100k growing to $110k in two years at retirement. If the client wants us to assume a 20 percent return over two years, fine! I will do that instead. The math still works.

By the end of the two years, her $100k has grown to $110 k. That is when we figure the first-year withdrawal, which comes out to $4,400. Again, that $4,400 is supposed to increase with inflation, per the four percent rule.

That $4,400 is assuming everything goes correctly. That is, that she gets 10 percent appreciation between now and age 65, and also that the four percent is indeed sustainable over her 30-year retirement.

That is when I will switch to the annuity. On one of the industry’s top annuities/GLWB riders right now, her $100,000 will “rollup” by 10 percent simple interest rate for two years, then that value of $120,000 will have a payout factor of 7.5 percent for a 65-year-old. (Note: Technically this 10 percent rollup is not limited to just two years. It depends on when she activates income, which in our example is two years.) That means that there will be a $9,000 payment starting two years from now, guaranteed for life! That payment will go on forever. This GLWB payment is 105 percent higher than what our four percent withdrawal rule will provide. And you don’t have the “hoping and praying” with the annuity. Usually at this point in the discussion, the responses are in three different areas:

Seems too good to be true! How can the company do that? This is a topic for another article.

What if everybody lives forever? Will the company go out of business? Again, a topic for another article.

But what about inflation? The four percent rule includes inflation, and the annuity does not. Let’s discuss.

Level Annuity Payment Versus Four Percent with inflation Although I believe we are being generous to the situation by using the four percent rule instead of the more updated and lower rules of thumb, it would be disingenuous to not explain the lack of inflation on the level payout GLWBs. (Note: There are some GLWBs that have increasing income, but let’s leave the conversation to the level income for now.)

This objection about annuities not having inflation included, versus the four percent rule is a reasonable objection, as inflation adjustments can be crucial. As a matter of fact, the “inflation rule of 72” says that a 3.5 percent inflation rate—for example—will chop the purchasing power of a dollar in half in only 20.5 years (72/3.5 = 20.5 years). Meaning that $9,000 would only have the purchasing power of $4,500 in 20.5 years assuming 3.5 percent inflation.

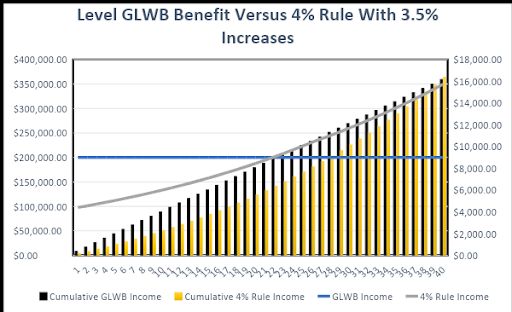

So then what provides the highest “cumulative income,” our GLWB or the four percent rule example? Included is a graph from a spreadsheet I created to show what provides more income—the $9,000 (GLWB) without inflation adjustments or the $4,400 (four percent rule) with inflation adjustments. (Note: For the inflation adjustments, I assumed 3.5 percent.)

As you can see in the chart, the inflation adjusted four percent rule annual income crosses over to where it is more than the $9,000 in the 22nd year! You can see the two lines crossing over. The dollar amounts represented by the lines are in the right axis.

Now, what is more important however is, what is the “cumulative income” from each strategy over a period of 40 years? That is represented by the bars and the left axis labels. As you can see, the Cumulative GLWB Income (Black Bar) stays higher than our cumulative four percent rule all the way through the 30-year retirement. As a matter of fact, it takes approximately 40 years for the four percent rule to catch up to our annuity income on a cumulative basis. In year-40, $364,776 is the cumulative income from the four percent rule at that point in time and $360,000 is the cumulative income from our annuity. So, in this example, only if the client lives beyond age 105 will she have garnered more income from the four percent strategy than our annuity.

Lastly, this analysis is being generous to the four percent rule because we are not incorporating the “time value of money” of the amount of excess GLWB payments we got above and beyond the four percent rule in the early years. Technically, those excess dollars reinvested would equate to even more than what our “cumulative” black bar is actually showing.

Clearly, there are other scenarios that we could run that can benefit or degrade the story on either one of the two solutions. For instance, we could run the four percent rule assuming a much higher return than 10 percent over two years, for example 20 percent. We could have taken into consideration capital gains taxes on the four percent rule of thumb versus income taxes on the annuity. But then we could also apply the “time value of money” to the excess annuity payments on the annuity. We could also use the 2.8 percent withdrawal rule. Or, one could add different inflation rates, etc.

In the end, and with all of this said, the story should be that consumers need to anchor their expectations reasonably and also that annuities have a great place in many consumers’ portfolios with or without inflation.

")