(Part 2 Of 2)

This is the second article of a two part “mini-series” on discussing “what the flow” (WTF) of an annuity conversation should be like. Afterall, based on CG Financial Group’s surveying of agents, discussing annuities with GLWB riders is an area where agents would like some further “refining.”

As discussed last month, there are five areas that financial professionals cite as areas they would like help explaining.

- Can’t a “financial advisor” give the same amount of income from a stock/bond portfolio? Afterall, the stock market has gone up 10 percent on average since 1926 and only five percent withdrawals (example) seems paltry! Ken Fischer says he can do better!

- Only $5,724.50 in income on a $100,000 premium? That means the client is merely getting back their premium for the first 18 years! That is not very sexy!

- I do not understand the relevance of the “Rollup Rate.” Isn’t that seven percent rollup rate just “funny money?” Afterall, it’s not like you can just cash that value out like you can the contract value/green line (subject to surrender charges).

- Don’t these riders cost a lot? Suze Orman says they do.

- How do I, as the financial professional, articulate the mechanics of the product as well as the overall value proposition? What’s the flow (WTF) of an annuity conversation that is effective?

Objection Bullet Point #1: “Can’t A Financial Advisor Do Better?”

To jump right into bullet point #1 above, here is my belief that bears repeating: Consumers will likely not recognize the true power of annuity GLWBs unless they are educated on the traditional withdrawal rate rules of thumb.

By educating consumers on these rules of thumb, you can “re-anchor” their expectations to reality and the fact that traditional withdrawal rate “rules of thumb” at retirement are anywhere from 2.3 percent to four percent, depending on which study you want to go by.

Many consumers know that the S&P 500 has gone up double digits on average for the last century and therefore overestimate what withdrawal rate they should utilize. Well, even though the S&P 500 could average 10 percent over the coming years does not mean the client will not run out of money by taking only four percent of the retirement value from their “stock and bond” portfolios! How is this possible? Because of sequence of returns risk that the “stock” portion can subject the client to and the low interest rates that the “bond” portion can subject the client to. And because of these two risks (sequence of returns and low rates), a client should not overestimate what a “financial advisor” can do as far as withdrawal rates. If you would like a graphic that helps you explain “sequence of returns risk” to your clients, email me.

Following are a few diagrams I use to help educate consumers on what their “financial advisor” might do as well as what an annuity might be able to do.

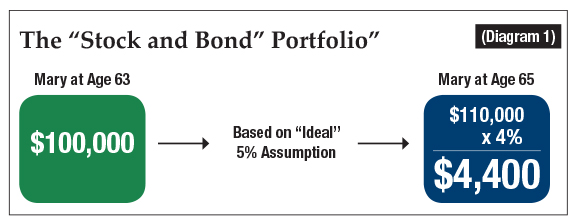

I first educate them on the old four percent withdrawal rule of thumb, (see diagram 1) even though that is being generous as the pundits are saying 2.3 percent to 2.8 percent is more like it today! I rationalize with them by drawing the diagrams on an “example” 63-year-old wanting to retire two years from now. Our 63 year-old has $100,000 in a stock and bond portfolio.

I discuss how this 63-year-old may have the expectation that her $100k grows by five percent or so per year between now and retirement in two years. Well, based on her $110,000 value at that point, what withdrawal should she take in her first year of retirement? This is where I discuss the old four percent withdrawal rule, which is contrary to popular belief. I also discuss the reasons for the withdrawal rate being only four percent. Hence, sequence of returns risk and low interest rates. But the end result of this diagram is a payment of $4,400. But that is only if her expectations Actually happen!

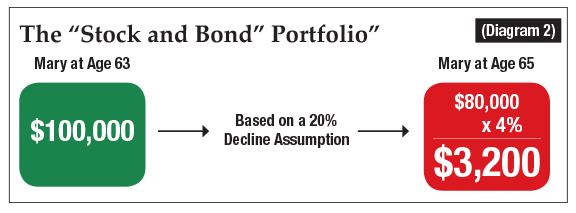

I then draw a second diagram (see diagram 2) that demonstrates the possibility of her expectations not coming true. As in, maybe between now and two years from now her portfolio loses 20 percent, versus gaining 10 percent that she had hoped for. This means she only gets $3,200 a year in income, a 27 percent pay cut relative to her “expectations.”

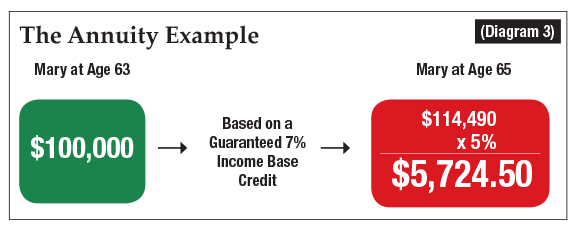

Lastly, I draw a diagram (see diagram 3) using the example GLWB rider that I showed you in last month’s column. This GLWB rider gives a “rollup rate” of seven percent per year then a payout factor of five percent at age 65. This particular rider is able to guarantee her 30 percent more income ($5,724 versus $4,400) than what she “hopes for” in her securities portfolio. No ifs, ands, or buts!

Usually, the response by the time I get done with the third diagram is, “How is that possible?” or “It seems too good to be true.” That is where I discuss longevity credits with her. (Email me for my conversation points on longevity credits.)

Objection Bullet Point #2: “Only $5,724 in income?”

We already discussed why these “rules of thumb” are so low—because of sequence of returns risk and also low interest rates—and why a guaranteed payment of $5,724 is quite attractive. However, if the client is only getting their premium back over 18 years ($100,000 divided by $5,274), they may question the worth of these riders.

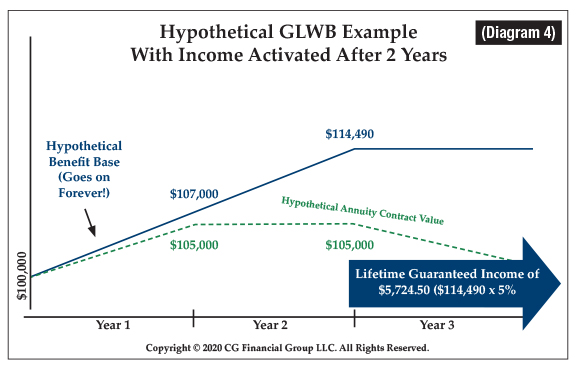

This is where I discuss with them (diagram 4) that I showed you last month. Their contract value (dashed green value) is still available to them and still gains interest based off the index, although it likely will be reduced if withdrawals are taken out. Note, many consumers think annuities are just locking them into a “lifetime payment.” Obviously not so with the innovation of GLWB riders that began almost twenty years ago with VAs!

I then discuss with them that all we are doing with a GLWB rider is buying an “insurance policy” on their longevity. And that insurance policy is what gives us that additional blue “Benefit Base” line.

Objection Bullet Point #3: “Isn’t that blue line just “funny money”?

This is a good question because a carrier could just do away with the “Benefit Base” and the required algebraic formulas, and instead just list payout percentages for certain ages and deferral periods. An example would be our 63-year-old having a guaranteed payout factor at age 65 of 5.72 percent ($5,724 withdrawal on her $100,000). Some carriers have in fact taken this route! However, for marketing reasons or what have you, the bulk of the carriers use the benefit base rollup and payout factor design.

I have two responses to the “funny money” question:

- I don’t care if the benefit base is “funny money” if the end result is that the client is guaranteed a very large withdrawal amount after the calculations are done. It is also important that agents not market the “Benefit Base” guarantee of seven percent like that is a liquid “contract value.” Lawsuits.

- When I explain the blue “Benefit Base value,” I draw a comparison to cash value life insurance. It goes something like this.

“Now the blue elevated value is a value the insurance company gives you in addition to your green “contract value.” This is the longevity insurance you are paying for. Do you get to just “cash out” that blue value? No. Instead, there are various rules the insurance company mandates you follow in order to get that blue value. Kind of like cash value life insurance where you have your “cash value” that you can cash out and you also have another value that is usually higher than your cash value, right? Except that “blue value” on the life insurance policy is the death benefit and, as we all know, you need to follow certain rules for that death benefit to pay out, correct? (Chuckle) Yes, you must die! Well, for this blue value on the annuity, you don’t have to die. The insurance company just says that you cannot take any more than five percent per year of that blue value out in order to not have the blue value/blue line decrease. That is the main rule you have to follow.”

Objection Bullet Point #4: “Suze Orman says annuities cost a lot”

Most indexed annuities without GLWB riders have no fees. The high-fee objection has its roots in the variable annuity world where subaccount charges, M&E, and rider charges can very easily get above three percent.

Now, if you are adding a GLWB to the indexed annuity, a common fee might be one percent. What I have found is, if you have done a good job explaining the diagrams above, old rules of thumb, blue line versus green line, etc., a one percent fee per year should not be a huge hurdle for that client that is concerned about outliving their money. If they do take issue with the one percent, it may not hurt to put the risk of outliving one’s money into perspective:

- There is an 18 percent chance you will total your car over your life. You buy auto insurance to hedge that risk!

- There is a three percent chance your house will burn down over your life. You buy homeowners insurance to hedge that risk.

- Morningstar says there is a 52 percent chance today that a stock and bond portfolio will not last a 30-year retirement by using the “old” four percent withdrawal rule. Why not hedge that risk as well? Afterall, there aren’t many things more important than not outliving your savings.

Objection Bullet Point #5: “How do I, as the financial professional, articulate the mechanics of the product as well as the overall value proposition?”

We all think differently, process information differently, and speak differently, but I hope these articles at least gave you ideas on how you should articulate the GLWB conversation as well as ideas for “napkin diagram drawings” that you can use with your clients.