(Part 1 Of 2)

Recently I have been surveying financial professionals across the country on topics related to practice management, annuities, life, and long term care insurance. The purpose of these surveys is to get a better understanding of areas of confusion, training they feel they are lacking, and also what kinds of training they desire. The ultimate goal of my IMO is to then address these areas via videos, whitepapers, and ongoing coaching so that the agents can help consumers more effectively and make more money! (Shameless plug: This online training platform and sales community will be launching March 1, 2021, and it is called “The Retirement Academy”—www.retirement-academy.com.)

In these surveys, there is one particular question about annuities that goes like this: “What areas of annuities could you use more education and coaching on in order to be more effective at selling?” A common response to these surveys has been, you guessed it, around the withdrawal benefit riders (GLWBs). These surveys show that, even if financial professionals understand how the riders work, they may still struggle with how to effectively communicate the value proposition of those riders. I have known for some time that this was one of the top areas of annuity confusion, but these surveys have been an interesting confirmation. It is clear that agents would like more help with explaining the value proposition of GLWB riders in a simple and effective manner.

So, I figure since this month’s Broker World topics are on Retirement, Estate and Legacy Planning, what better item is there to cover than explaining the value proposition of indexed annuities and GLWBs for retirement income! In this article we will discuss how an agent starts the conversation, what the agent should point out to the client, what’s the flow (WTF) of the conversation, etc.

In an effort to make this topic manageable to the readers (and my friend and Broker World publisher Steve Howard) this is a two-part article, with the second half coming in the January column.

Background:

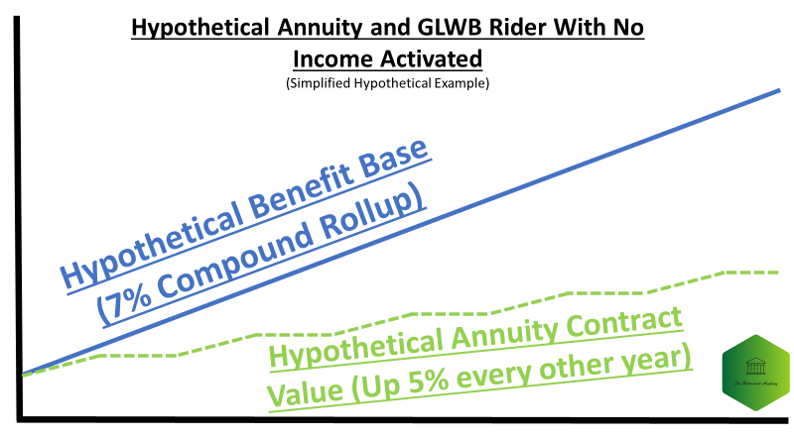

To give a little bit of background on where the issues lie, refer to my simplified illustration below of an example GLWB rider design. This is a greatly simplified visual representation of a rider design that I often use as an example with the numbers removed for ease of viewing. What the numbers and values are doesn’t really matter for this part, but usually I use the example of the blue “Benefit Base” line that the client gets representing their premium plus a “guaranteed benefit base rollup rate” of seven percent. That means that my blue benefit base line would be growing by seven percent per year on top of the premium the client puts in. Usually the premium I use in my examples is the good ole fashioned $100,000. The green dotted line is quite simply the client’s annuity “contract value” based on how the client’s $100,000 actually performs—whether the product has a cap, a participation rate, a spread, etc.

You can see that the green line has some good (five percent) years and some “flat” years. Remember, with indexed annuities you cannot lose value because of a market decline. There can be rider charges however that can slightly erode your contract value/green value, which I leave out in this demonstration for the sake of simplicity. This visual is merely a representation of what the “benefit base” typically does when there are no withdrawals/income being illustrated or “activated.” I will show you a diagram of WDs being activated in a bit.

GLWB Confusion

As the surveys show, there are many financial professionals—from new to seasoned–that experience a lot of confusion around how to explain the three main components of GLWBs:

- The “Benefit Base” value;

- The Payout Percentages of the benefit base that determines the ultimate income; and,

- The ultimate lifetime income at various ages.

To be clear, when I say that there is “confusion” around explaining how these three items work, I am not saying that financial professionals lack the ability to discuss the mechanics. Afterall, most of us understand that #1 multiplied by #2 will equal #3 (benefit base x payout percentage=lifetime income) at the age the client chooses to activate their withdrawals/income. Rather, the confusion lies in how to explain the power of those three values in a logical and linear fashion that allows the clients to recognize the value of what these wonderful riders do!

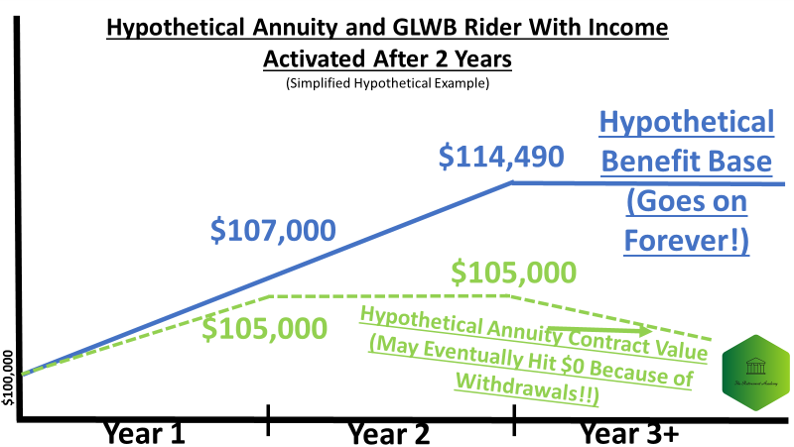

The illustration below is the same except zoomed in and now illustrating income that the client “activates” after the second year (as an example). Once the client activates income from the annuity, she can only take three to six percent (depending on age of client and the product) of the benefit base/blue line per year in order for the blue line to not decrease or disappear.

A payout starting at age 65 might be around five percent of the benefit base, although that is a little on the high end nowadays. This would mean that if the client elects income in the second year and she is age 65, she would be able to get income of $5,724.50 ($114,490 x .05) for the rest of her life. With many products, at the time we “activate” the income the blue line will stop growing and the income level will be a percentage of that static benefit base forever! (Note: There have been innovations in GLWBs in recent years where, even if you are taking withdrawals, the blue line continues to increase.)

Even if you live until age 150 and even if your green “contract value” hits $0, your income of $5,724 will continue forever in our example.

Areas of Objection:

Now, whether in the minds of well-intentioned financial professionals trying to articulate the value of these products or in the minds of consumers, there can often be confusion on the value proposition of the GLWB. Examples of confusion can be:

- Can’t a “financial advisor” give the same amount of income from a stock/bond portfolio? Afterall, the stock market has gone up 10 percent on average since 1926 and only five percent withdrawals seem paltry! Ken Fischer says he can do better!

- Only $5,724.50 in income? That means the client is merely getting back their premium for the first 18 years! That is not very sexy!

- I do not understand the relevance of the “Rollup Rate.” Isn’t that seven percent rollup rate just “funny money?” Afterall, it’s not like you can just cash that value out like you can the green line (subject to surrender charges).

- Don’t these riders cost a lot? Suze Orman says they do.

- How do I, as the financial professional, articulate the mechanics of the product as well as the overall value proposition? What’s the flow (WTF) of an annuity conversation that is effective?

Now that we have laid out the background in GLWB product design as well as areas where many financial professionals would like help, let’s dive in.

(Note: This month’s column will address my thoughts on #1 above. January’s column will address #2, #3 and #4 above. Of course, the overarching intent of both columns is to address #5 above!)

The Re-Anchoring (Confusion Area #1):

As we know from the field of behavioral science—or just plain sales coaching—anchoring is a remarkably effective strategy as we sell and explain complicated concepts. It is because of the power of “anchoring” that it’s been said hundreds of times over the years that:

“Consumers will likely not recognize the true power of annuity GLWBs unless they are educated on the traditional withdrawal rate rules of thumb.”—Me

In other words, I believe that consumers are anchoring their retirement income expectations on the wrong thing and therefore should be “re-anchored” in reality. Hence these consumers should be educated on the fact that William Bengen’s study in 1994 showed that in order to sustain a stock/bond retirement portfolio for 30+ years in retirement, the consumer should take out no more than four percent of their retirement account balance that first year in retirement. Consumers should also be aware of the new updated studies by Morningstar and Wade Pfau that show “rules of thumb” of 2.3 to 2.8 percent.

I am not suggesting an agent go into a big dissertation on these individual studies. I just believe that going over the simplified math—specific to the client’s portfolios—based on these new “rules of thumb” should be done in order to show the power of annuity GLWBs. Heck, even using the old four percent rule of thumb will suffice in explaining the annuity value proposition. By demonstrating this math to the clients, you will be “re-anchoring” their expectations to realistic numbers. And only then do I believe they will realize the true power of GLWB riders. (An example of going over the math with a hypothetical client will be in the January “Part 2”.)

Why Do Consumers Need “Re-Anchoring”?

Re-anchoring is important because consumers are generally unaware of what a reasonable withdrawal rate should be from their retirement portfolio. They have seen the glorification of the stock and bond markets and have likely seen the mountain charts like the Ibbotson SBBI Chart. You know what charts I am referring to—those that show that the stock market has done double digit returns forever and that their one dollar invested back when Adam met Eve would be worth enough to purchase their own private island today. Thus, if a consumer has in their brain that “stocks and bonds” have always performed at seven percent, eight percent, 10 percent, 12 percent…then they will tend to believe that their retirement withdrawal rate is beyond the four percent or 2.3 percent that the research shows. Even if a consumer has heard of the “four percent withdrawal rule,” they may not have had the math laid out for them yet that is specific to their situation.

To demonstrate my points in the previous paragraph, I want to cite a study by Charles Schwab. In their 2020 Modern Retirement Survey they asked 2,000 pre-retirees and the newly-retired about how much money they had saved for retirement and also how much money they expected to take from their retirement portfolios. The answers from the participants were that they had $920,400 in retirement savings (on average), that they planned on spending $135,100 per year from those portfolios (on average), and that they were generally confident in those dollar amounts allowing them to live the retirements they would like.

I would argue that a 14.68 percent withdrawal rate ($135,100 Divided By $920,400) defies any retirement research I have seen! Naturally, Schwab then points out that—contrary to these participants’ beliefs—a $920k portfolio will run out in only seven years (obviously not including interest/appreciation). Clearly, these consumers should have the math explained to them. Even if the consumers understand the new “rules of thumb,” they may be experiencing cognitive dissonance that should be addressed by the financial professional. By doing so you will “re-anchor” their expectations to the new realities of 2.3 or four percent withdrawal rates, which will set you up for the annuity conversation that we will discuss next month.

To hammer home my main point here. Again, I believe the ensuing GLWB conversation will resonate most only after you anchor the client’s mind on the fact that their stock and bond portfolio will likely not last if they are withdrawing at five percent, six percent, seven percent, or 15 percent rates. If you would like more information on those previously cited “rule of thumb” studies, feel free to email me. See you next month!