(Reprinted from the CLTC Digest in cooperation with Certification for Long-Term Care, LLC, www.ltc-cltc.com. Email Amber Pate at apate@ltc-cltc.com for a more than 20 percent discount on CLTC training for Broker World subscribers—just mention code BWMAG.)

Long term care can no longer be avoided as an important part of our financial plans. The concept of the coming extended care wave is being discussed in legislative sessions and among healthcare organizations. Financial advisors and insurance agents are in a unique position to push the conversation forward with consumers in a positive way.

There is no way to stop the aging process—at least not yet. But when it comes to long term care planning, many people take a wait-and-see approach. They don’t want to think about the possibility of needing extended care or how they plan to pay for that care. Some assume they can’t afford an insurance plan so just leave it to chance or their children. Many Americans believe that Medicare will pay for it—a costly and incorrect assumption. Once people face the reality, it is often too late to plan due to health issues or financial resources.

Even those who plan for retirement have not planned for a long term care need. And that’s something that could literally wipe out the retirement savings Americans have worked so hard to build. Helping clients plan before they need care is a wise approach. A good place to start is having a conversation about what to expect when it comes to overall long term care costs.

The Human Toll

Before we address the direct costs associated with long term care, it’s important to understand that there are other considerations. It is also about the human cost in managing stress, lost wages, and job insecurity due to working caregivers having to take off or go to work late or leave early. Some family members wind up leaving the workforce, even though their income is needed for household expenses. And the impact of COVID on long term care is still not fully understood.

The stress of a family member caring for a loved one has been shown to impact a person’s immune system for up to three years after their caregiving ends. This increases their chances of developing a chronic illness themselves.

Other significant points from a recent survey on caregiving in the United States:1

- Although the average caregiving time is 4.5 years, one out of three caregivers reports providing care longer than five years.

- One in five caregivers provide 41 or more hours of care per week (full-time job).

- 36 percent report emotional strain/stress.

- 61 percent report impact on work.

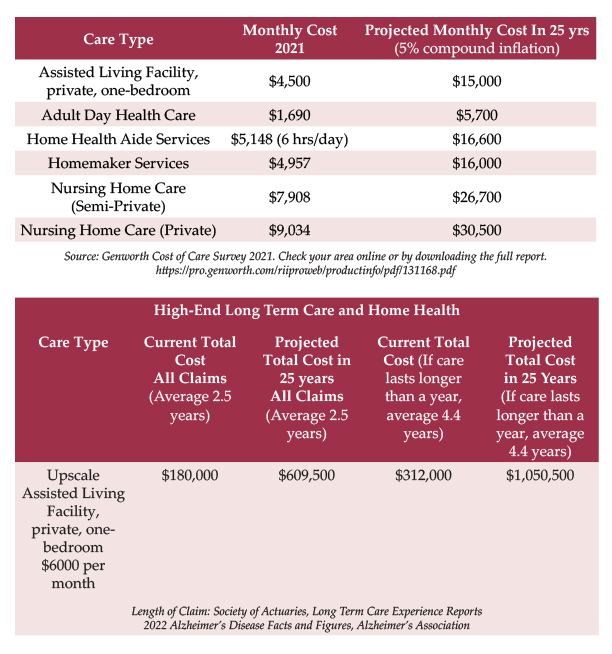

Cost of Care Survey

According to the Genworth Cost of Care Survey, below are the current median monthly cost estimates and projected costs after 25 years. Keep in mind that costs vary widely by state and even by city. (Note: “Median” means half cost more and half cost less. These numbers do not reflect upscale assisted living and nursing facilities.)

Projected Total Cost

The average duration for care is 2.5 years, but for people who need care for longer than a year, the average is 4.4 years (men average 3.8 years and women average 4.7 years). This includes home care, assisted living facilities, and nursing homes. Studies indicate that people aged 65 and older survive an average of four to eight years after a diagnosis of Alzheimer’s, yet some live as long as 20 years.

Since care is typically blended between care locations, e.g., some at home and some in a facility, let’s use the cost of an upscale assisted living facility to project future costs for both types of averages. The cost of the upscale assisted living facility can be derived by adding $1,500 per month to the median cost of $4,500 per month. This amount of $6,000 should also provide for a significant amount of home care, perhaps 7-8 hours per day.

Questions for Your Clients to Consider

There are specific questions that you can ask clients that will help them dive a little deeper into their planning process. These will also highlight areas of concern where it’s clear that they need to start considering putting a plan in place. Once this is achieved, partner with a long term care specialist to help clients work through a comprehensive long term care plan.

Where do you plan to retire?

Are you planning to move out of state? Will you have any family nearby who might be able to assist with your care? Cost of care can vary dramatically by state.

What impact will needing extended chronic care have on your income?

What will happen to your income should you or your spouse require extended care while one or both of you are still working? Relying on Medicaid to pay for long term care means that you and your spouse will be subject to asset thresholds that can wipe out most of your retirement savings.

What impact will needing extended chronic care have on your assets?

Retirees typically use assets for income. What would spending a significant amount of your assets on long term care do to your income?

What type of care do you prefer?

Do you want the option for home health care? Would you want to be able to use less costly informal caregivers? Do you want the option for a high-end assisted living facility, sometimes referred to as a “country club” assisted living facility?

What can you comfortably afford over the long term?

If you’re considering long term care insurance, meaningful coverage can have many benefits. Make sure that whatever plan you choose, you can afford it for the long term. A nice feature of many plans is that the premium is waived when you start receiving benefits. Some plans have guaranteed premium, so you never have to worry about a rate increase.

For the full report, Understanding the Cost of Care in 2022, go to www.buddyins.com and search the Learning Center.

Reference:

1. Caregiving in the United States; National Alliance for Caregiving in collaboration with AARP. May 2020 Caregiving in the US 2020 | The National Alliance for Caregiving

Marc would like to thank Phyllis Shelton for her invaluable contribution to this article. Shelton is the president of Got LTCi, part of a long term care insurance outreach that she founded in 1991. She is widely considered to be a leading long term care insurance sales trainer in the country. As a BuddyIns partner, Shelton leads a highly successful team of long term care specialists.

Shelton can be reached through her website at https://gotltci.com/contact-us/.