Business owners have long been considered by most to be the lifeblood of the American economy. They are what drive our economic growth. Successful business owners really embody three traits:

- Business owners value the importance of protecting their assets.

- Business owners value the importance of mitigating tax exposure and paying unnecessary taxes.

- Business owners understand and value the importance of having access and use to liquidity and capital.

The good news is, although not every one of us may be a business owner we all have access to these principles and strategies within our own portfolio to create our own private reserves of wealth. One just so happens to be properly structured cash-value life insurance. Properly structured cash-value life insurance, when leveraged as your own private reserve strategy, can allow you the ability to make major purchases for big events in your life. It can also allow clients to have access to that cash if needed for unforeseen circumstances. Lastly, it allows clients to have access to position this as supplemental retirement income.

Now, one may ask, “What is needed for this strategy? Or is this a strategy for me?”

The first requirement is the need for life insurance. The second is that you must value the importance of financial protection. There are several benefits of owning a cash-value life insurance plan for your private reserve of wealth. The chart shows of the most common uses.

But what does it look like in action? We’re going to look at a client here by the name of Tom.

- Tom is 35 years old.

- He’s in great health.

- He’s married with two young children.

- Tom maxes out his contributions to his Roth IRA and 401(k) up to the four percent match.

Tom also understands that his 401(k) cannot be accessed until he is 59 1/2 and there could be times in his life that he may need access to capital right away. So, Tom decides to purchase a properly structured indexed universal life (IUL) policy. A properly structured indexed universal life policy allows the contributions to grow on a tax deferred basis, while allowing clients to access that cash on a tax-free basis. If a client were to pass away prematurely, the beneficiaries will have access to the death benefit tax-free.

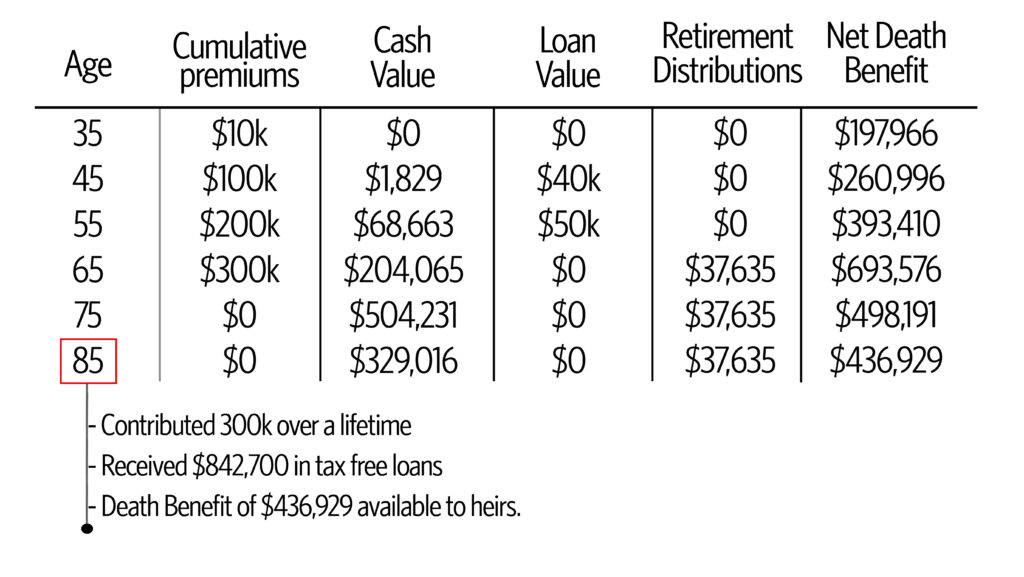

In this example, Tom chooses to contribute $10,000 per year to his policy for 30 years. He decides to take out a $40,000 loan at the age of 45 to start a small business. After that loan, you can see that the cash value in the policy is still $68,000. Ten years later, at the age of 55, he takes out a $50,000 loan because he intends to put a downpayment on a vacation home. It is not until the age of 65 that there is enough cash value in this policy for him to now turn on his tax-free retirement income that runs to the age 100. If we now review the values at age 85, which is life expectancy, we can see the following:

- At 85, Tom has contributed $300,000 over the life of this policy.

- At 85, Tom has received $842,700 in tax-free income benefits.

- At 85, Tom has a death benefit of $436,929.

- Total Value of potential $1,279,629 tax free benefits.

There are some considerations with an indexed universal life policy. These policies are tied to an index and policy performance is important. In addition to policy performance, it is important that clients work with their trusted advisor to set realistic expectations in the form of illustrated rates and work to ensure that the policy remains on track each year by conducting annual reviews. There are an infinite number of ways to fund and structure these policies. However, it is advised to maximum fund an IUL policy, which means purchasing the minimum amount of death benefit and putting in the most amount of premiums that the policy will allow to avoid a Modified Endowment Contract (MEC).

If your clients value family protection, mitigating taxes, and having access to liquidity and capital, I encourage you to reach out to them to see if a private reserve wealth strategy is right for them so they can experience a similar success as Tom did in this example.