In the current economic climate, characterized by significant challenges in government spending and mounting debt, financial advisors play a critical role in guiding high-net-worth individuals toward sound financial decisions. Recent reports from the U.S. Department of Treasury emphasize the urgent need for strategic planning and shed light on the nation’s alarming financial health and the imperative need for diversifying financial portfolios.

The February 2024 Treasury Statement reveals a stark reality: U.S. government spending has soared to unprecedented levels, far surpassing revenue intake. Shockingly, the IRS has allocated a substantial 63 percent of the individual income taxes collected this past month toward servicing the national debt interest. This trend is alarming. Projections indicate a staggering $350 billion solely for debt servicing through fiscal year 2024, surpassing the collective vital expenditures for veteran benefits, education, commerce, and housing.1

Financial advisors must equip high-net-worth individuals with the necessary tools and strategies to shield them from financial devastation from potential future tax liability. It is indisputable that these considerations are critical for providing clients with the best service. However, there is a noticeable deficit of financial professionals who offer services to their affluent clients for strategically alleviating future tax liability.

We must fill this critical gap by implementing beneficial strategies tailored to the unique needs and objectives of the clients with future tax threats in mind. While there are many strategies financial professionals can consider, I believe these three are worth considering: Estate Planning, Qualified Charitable Distributions (QCDs), and Charitable Bequests.

My goal in this article is to provide the foundational springboard to launch your services to new heights by highlighting the benefits of offering estate planning, presenting solutions to looming tax threats, and providing alternatives for a range of clients since nothing in financial planning is one size fits all.

Many financial advisors overlook estate planning despite acknowledging it as a crucial aspect of financial management, particularly for high-net-worth individuals. As a cornerstone of their financial strategy, estate planning entails a holistic approach to wealth management, tax mitigation, and ensuring the smooth transfer of assets to chosen heirs or beneficiaries. Utilizing trusts, wills, and various legal instruments, estate planning empowers individuals to safeguard their legacy, secure provisions for their loved ones, and contribute to charitable endeavors aligned with their values.

For instance, estate planning can be advantageous for high-net-worth individuals in many vital aspects of their financial well-being:

- Tax Efficiency: Properly structured estate plans can minimize estate taxes, preserving the wealth for future generations.

- Asset Protection: Trusts and other estate planning tools shield assets from creditors and potential threats, safeguarding wealth for heirs.

- Control and Flexibility: estate planning enables individuals to dictate asset distribution, ensuring their wishes are honored even after they are gone.

By incorporating comprehensive estate planning into financial strategies, advisors can help high-net-worth clients secure their legacies, protect assets, and confidently navigate complex tax landscapes. Now that we have highlighted the benefits of offering estate planning, the next step is to consider the solutions to looming tax threats.

One question to ask is how our high-net-worth clients plan on paying for that looming tax bill. The government will inevitably want their money, and their sights are on the top income earners in the country. With the target on their backs, it is vital to consider how these clients are expected to pay those taxes so you can develop the best course of action.

Essentially, there are three popular ways for these clients to pay estate taxes:

- Pay cash: This may not be possible for many families, but once that money is gone, it is gone.

- Sell assets: Homes, businesses, equipment, or other assets may need to be sold to gain liquidity for tax purposes. (Not ideal for family businesses.)

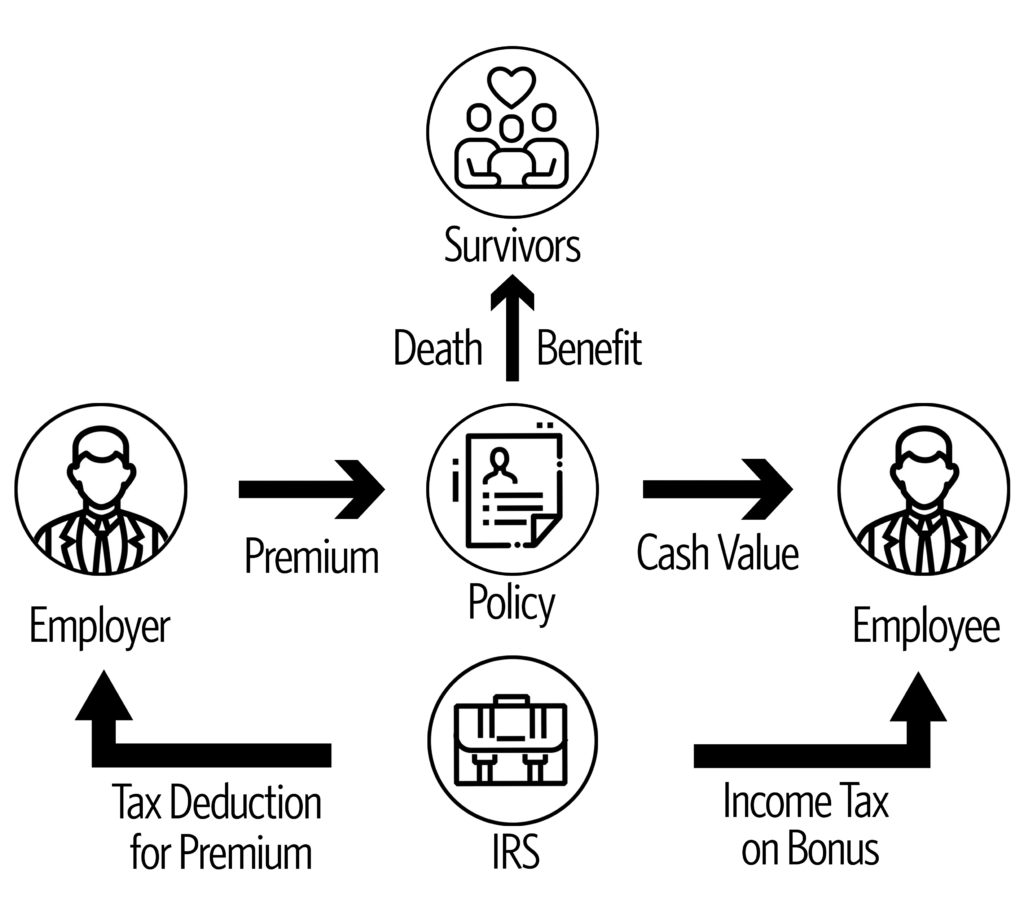

- Purchase life insurance: In most cases, the least expensive of these three options is to take advantage of life insurance proceeds. Additionally, with a properly designed estate plan, beneficiaries will receive a tax-free death benefit from the policy. It might make sense in some cases to create an irrevocable life insurance trust (ILIT) depending on the estate’s value, creating an exemption that removes the insurance policy from being counted as an estate asset.

Furthermore, should the estate beneficiaries lack sufficient liquidity, they might explore borrowing options to cover estate taxes, such as utilizing Graegin loans or section 6166 election.

A Graegin loan offers the chance to utilize an external lender, rather than relying on the IRS, to finance the estate tax loan. This lender can be an outside bank or a related party, such as a family limited partnership or irrevocable gift trust, provided that the loan is genuine.

A Graegin loan has the following requirements:

- The estate must be illiquid;

- The loan must be at a fixed rate; and,

- The loan must prohibit prepayment.

Section 6166 allows an executor to defer the payment of federal estate tax associated with owning a closely held business. These postponed payments can be extended for up to fourteen years and nine months following the business owner’s passing.

Section 6166 deferral is available if the estate meets the following requirements:

- The decedent must have been, at death, a citizen or resident of the United States.

- The estate holds an interest in a closely held business.

- The interest constitutes more than 35 percent of the adjusted gross estate (AGE) and certain other requirements are met.

- The executor elects, on a timely filed estate tax return, to pay a portion of the estate tax and generation skipping transfer tax attributable to the closely held business resulting from direct skips.

For individuals engaged in estate planning, life insurance shields against the threat of potential lifestyle setbacks and is especially crucial when assessing the adequacy of assets to sustain the accustomed lifestyle of surviving family members. Furthermore, considerations extend to covering long term care and end-of-life healthcare on top of other potential curveballs in their financial plan.

Additionally, future earnings represent a substantial asset for those still actively earning income. For example, projecting future earnings of $1 million annually over 25 years until retirement yields a significant value of $25 million, even without factoring in potential income increases. Ensuring adequate life insurance coverage to replace this income secures the family’s future lifestyle and generational wealth, enabling clients to maintain their current residence, fund their children’s education, cover medical expenses, and enjoy life without financial strain.

Now that we have established the benefits of estate planning and the advantages of life insurance, the pivotal question arises: What type of insurance and how much do you need? These are the primary considerations for individuals considering the purchase of life insurance.

There are two popular types of life insurance:

- Term Life Insurance: This covers an individual for a specified number of years. Term life insurance solely offers a death benefit without cash value accumulation. It is often more affordable than permanent life insurance, making it a budget-friendly option. While premiums remain consistent throughout the policy’s duration, costs may rise in later years. Term is a temporary product for a potentially permanent problem.

- Permanent Life Insurance: This is a type of life insurance that provides coverage for the insured’s entire lifetime, as long as premiums are paid as specified in the policy. There are several types of permanent life insurance, including whole life insurance, universal life insurance, and variable life insurance, each with its own features and benefits. This provides a permanent solution for a permanent problem. For many high-net-worth (HNW) individuals, the consideration of a survivorship policy may be advantageous. These policies are typically preferred for healthy couples due to their lower insurance costs and the protection they afford to both individuals. Moreover, the life insurance need is fulfilled through the tax-free death benefit upon the passing of the second or surviving spouse.

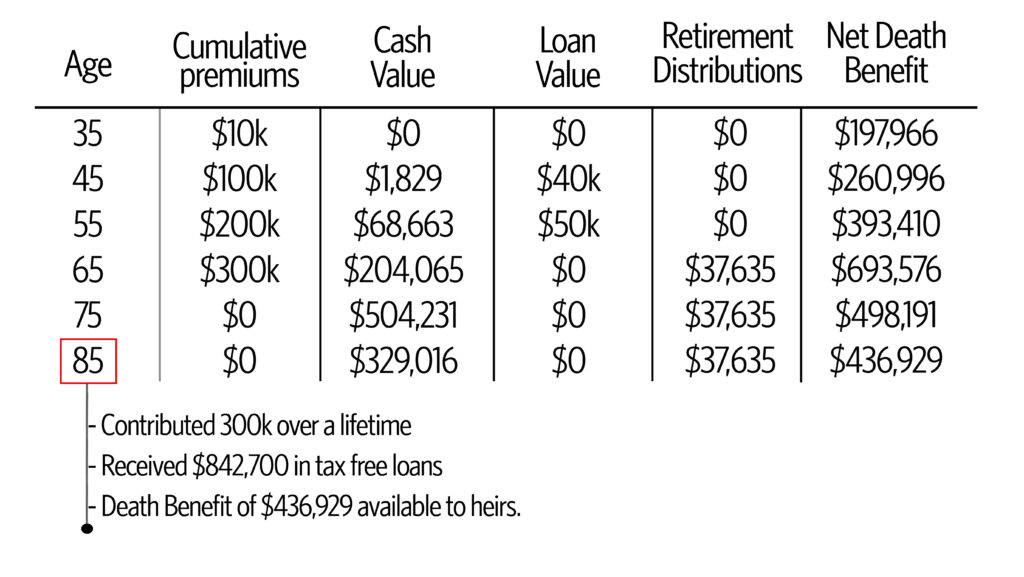

Finally, there is Permanent Financed Life Insurance. Despite sharing the characteristics of permanent life insurance, the financing aspect allows participants to purchase more death benefits and living benefits than they could afford independently. By injecting additional cash into the policy through financing, the cash accumulation within the policy can reach substantially higher levels. With the advent of the greatest wealth transfer in history, premium financing emerges as an exceptional choice for clients with significant assets through gifting insurance to their children and grandchildren.

It’s crucial to acknowledge that premium finance introduces additional risk, particularly if lending rates remain elevated over an extended period and the underlying policy yields fall short of expectations. However, there are advantages to premium finance: The grantor often allocates interest to the trust instead of funding the entire premium, potentially leading to greater tax efficiency. Additionally, the overall outflow to the trust may be reduced compared to a non-financed policy, enabling them to preserve more capital that could generate higher returns elsewhere.

While the insurance policies mentioned are valuable assets in estate planning, it’s essential to recognize that some clients may not meet the qualifications for these policies. For our high-net-worth clients, we often suggest utilizing gifts to acquire ILIT-owned life insurance, which proves sufficient for many. Nevertheless, individuals with significant estates may find that the $18,000 (2024 limit) annual gift per estate beneficiary does not effectively reduce their estate values. In essence, attempting to reduce their estate by $18,000 multiplied by two spouses in the form of annual gifts out of the estate is like facing off with a freight train armed with a BB gun.

Moreover, certain families believe that their heirs will inherit ample wealth but are hesitant to allocate a significant portion of their estate to the IRS. For individuals in this situation, charitable planning becomes a viable option, encompassing various strategies such as Charitable Remainder Trusts (CRTs), Qualified Charitable Distributions (QCDs), and Charitable Bequests.

Qualified charitable distributions (QCDs) and charitable bequests could be attractive solutions for these clients. QCDs enable individuals aged 70½ or older to donate up to $100,0000 directly from their IRAs to qualified charities without incurring income tax on distributions.

Benefits of QCDs for high-net-worth individuals include:

- Tax Savings: QCDs allow individuals to fulfill required minimum distributions (RMDs) while reducing taxable income, potentially resulting in significant tax savings.

- Charitable Impact: QCDs empower individuals to support causes they care about, making a positive difference in communities.

- Simplicity and Efficiency: QCDs offer a straightforward way to donate to charity, benefiting clients and designated charitable organizations directly.

The second alternative worth considering is strategically taking advantage of charitable bequests for clients who want to ensure that future generations are cared for. Charitable bequests offer a powerful means of supporting beneficial causes while preserving family wealth. A charitable bequest designates a portion of an individual’s estate as a donation to charitable organizations of their choice upon their passing. As it stands today, individuals have the option to elect a one-time distribution of up to $50,000 from an individual retirement account to charities through a charitable remainder annuity trust, a charitable remainder unitrust, or a charitable gift annuity. Each of these options is funded exclusively by qualified charitable distributions.2

Benefits of Charitable Bequests for high-net-worth individuals include:

- Legacy Preservation: Charitable bequests enable individuals to leave a lasting impact on causes they care about, ensuring their values endure for generations.

- Tax Advantages: Charitable bequests can reduce estate taxes, resulting in significant tax savings for clients and their heirs.

- Flexibility and Control: Charitable bequests allow clients to retain control over asset distribution, ensuring the achievement of philanthropic goals while honoring personal wishes.

By integrating QCDs and charitable bequests into financial planning discussions, advisors can help high-net-worth clients maximize charitable contributions while minimizing tax burdens and creating legacies of generosity, aligning financial goals with philanthropic values. Implementing QCDs, charitable bequests, and strategic insurance vehicles can considerably expand the value you offer to clients in their estate plans.

At this precarious and volatile point in our economic state, the call to diversify financial portfolios grows louder and more urgent. Now, more than ever, proactive financial planning provides resiliency in the face of threat, security in the face of risk, and peace of mind in the face of the unknown. I hope this article inspires you to consider furthering the solutions and stability you provide clients through the strategic use of estate planning, qualified charitable distributions, and charitable bequests.

Reference: