This article is intended for financial professionals that have the wise business practice in helping consumers plan for Social Security, and also for consumers.

For folks that may not be interested in number crunching or those that are not real familiar with financial calculators and cash flow analysis, this article may shed light on if delaying Social Security benefits is worth it. For the layperson, it may sound good when one hears, “If you delay Social Security Retirement Benefits from age 67 until age 70, you will get 24 percent more in income by waiting those extra three years.” Well, is that a good deal or a bad deal taking into consideration “Time Value of Money?” Let’s discuss.

Time Value of Huh?

The concept of “Time Value of Money” is that $100 today is generally better than $100 received in the future, which is a large reason why around 50 percent of folks take Social Security early.

Taking it further, what would you prefer to have—$100 today or $103 one year into the future? That is a more difficult calculation because it depends on what prevailing interest rates are in the economy and if you could turn that $100 today into more than $103 one year from now by investing your $100 today. My personal choice would be to have $100 today because I know that I can invest that into something that would give me a guaranteed rate of almost six percent (Guaranteed Rate Annuity). That means that I could turn my $100 into $106 in a year. (Note: I am not taking into consideration taxes in my example.)

With Social Security analysis, we need to view what we are foregoing today—also known as “opportunity cost”—in order to get X in the future as this: What you are foregoing today is the “investment” in order to get X as the payoff in the future. The lost opportunity—or “opportunity cost”—is an economic term that much of the financial world revolves around.

In other words, if I were to invest $100 today and get $103 back one year from now, then that means the internal rate of return on my money was three percent. That means that if you are given a choice between $100 today and $103 in a year, but can only get three percent on your money, then the $100 today is exactly equivalent to $103 one year from now. Again, simplified because we are not considering taxes on the growth. The decision between $100 and $103 is a toss-up if you can only get three percent.

Another decision that is a toss-up is, if you were offered $100 today versus $106.09 two years from now. Why is that a toss-up? Because if you could invest $100 today at a rate of three percent per year, you would have exactly $106.09 two-years from now after compounding. So again, $100 today is equivalent to $106.09 two-years from now, at least if you could only get three percent on your money. Three percent is the “discount rate” that makes $106.09 two-years from now equivalent to $100 today. It is no coincidence that if you punched into a financial calculator that you are investing $100 and getting back $106.09 two years from now, that the internal rate of return will come back at three percent. Well, again, if I can get a six percent internal rate of return on my money, instead of three percent, then I will choose to take the $100 today. That $100 today can grow to $112.36 two years from now at a six percent rate.

That is how “time value of money” works.

Case Study:

Now let’s get to Social Security. With Social Security analysis, we will use the same logic as above except we are not trading one small payment today for one small payment in the future. We are trading a series of dollar amounts over a number of years for a larger series of dollar amounts in the future. So, the math is more complicated but it is utilizing the same logic.

Let’s take Rob, who has a Social Security “full retirement age” of 67. Rob’s full SS benefit—also known as his primary insurance amount—is $20,000 per year. He has a choice: Does he take his Social Security benefit today at age 67, or delay?

By my 67-year-old delaying filing until age 70, he is giving up total income of more than $60,000 over the next three years. I say “more than” because technically that $20,000 that he would receive today—at full retirement age—is generally increased with inflation. So this year Rob may be giving up $20,000, but next year he may be leaving $20,700 on the table by not filing—assuming a hypothetical 3.5 percent inflation rate.

But what is his tradeoff? The positive tradeoff in waiting until age 70 is that after three years his Social Security payments would amount to $24,800 per year—not including inflation adjustments—instead of the original $20,000 per year. This is because he would have received eight percent per year in “delayed retirement credits” that the Social Security Administration gives us for delaying, which amounts to an additional $4,800 in yearly benefits. Again, it would actually be more than $24,800 because it would technically be inflation adjusted. We will reflect on inflation in a bit.

So, we understand that he would get roughly $4,800 more in Social Security payments, but for how long? And most importantly, is that a good deal? Our 65-year old male has a life expectancy (per the Social Security Tables) of approximately 15 years. Therefore, we can plan on our “approximately” $4,800 in additional Social Security payments going for 15 years.

As we analyze the question of “is it worth it?” think of the scenario as the following analogy: Rob would be paying into an “annuity” for three years to the tune of $20,000 per year plus inflation. That is the “opportunity cost” of delaying. We will assume a 3.5 percent inflation rate because that is the historic long-term average. That “annuity” will start providing lifetime payouts in the fourth year of the additional $4,800 per year that is adjusted for inflation every year. That last point is important. Rob is not “just” getting an additional payout of $4,800 per year. We are getting an additional inflation adjusted $4,800 per year!

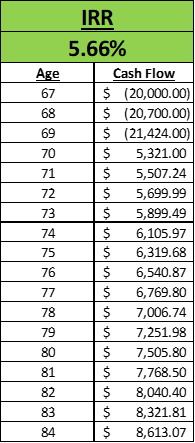

In (Table 1) I laid out the cash flow of our scenario. The parenthesis represents the lost opportunity of $20k per year for three years, which adjusts for inflation each year. Then, at age-70, the benefit that our retiree gets starts rolling in. As mentioned, the $4,800 is adjusted each year for inflation as well. With inflation of 3.5 percent, our $4,800 today will “inflate” to $5,321 three years from now, and so on.

Our ultimate question is this: In our “annuity” analogy, what would the rate of return be on this annuity where we paid in over $60k in return for the additional income? What “internal rate of return” does delaying Social Security provide, at least based on our 67-year-old male, this lifespan assumption, and this inflation assumption? 5.66 percent. Not a bad rate, especially if Rob is receiving his Social Security tax-free. If Rob was in a 22 percent tax bracket, then that is a “taxable equivalent” rate of return of 7.26 percent. Can Rob get that kind of return elsewhere? If he can, then maybe taking Social Security at “full retirement age” is the best option.

\Table 1 is merely some quick IRR analysis of Rob’s decision using certain assumptions. Technically, there are other variables and factors that he should look at as well before making his decision, but we will discuss a few of those in a bit.

Rob Lives Longer than “Life Expectancy”

One such “variable” is, what if he lives shorter or he lives longer?

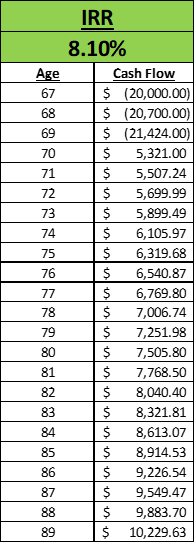

Let’s assume he lives an additional five years beyond life expectancy. (Table 2) is our new cash flow table that shows our internal rate of return as being 8.10 percent! That is a taxable equivalent of 10.38 percent, assuming his 22 percent tax bracket. If Rob has good genetics, he may want to consider delaying!

Other Factors:

- Different Inflation Assumptions: If you think inflation is going to be higher than my 3.5 percent, then the internal rates of return will increase relative to my examples above and vice versa.

- Taxes: If your Social Security is being taxed, as almost 50 percent of recipients’ are, then my “taxable equivalent yield” goes out the window. However, many times, delaying Social Security to age 70 helps the tax situation because you are generally “spending down” your pre-tax dollars in those “bridge years” from age 67 to age 70. This can lead to less reliance on pre-tax dollars at age 70+ that can otherwise add to your Social Security taxation. Said differently and to exaggerate, if you spun down all of your pre-tax dollars from age 67 to age 70, then you would not be taking any of those pre-tax dollars in the years you are taking your Social Security. This means possibly less taxes on your Social Security because your provisional income would be relatively less! Furthermore, by spending pre-tax dollars in your bridge years you are reducing what you will ultimately have to take in required distributions at age 73.

- It’s not just about Rob: Stats say that one of a couple that is in their mid-60s will live until age 92. So, if Rob has the higher SS payment between he and his wife, she will ultimately inherit his benefit. And if she lives until 92, for example, then my IRR number is even larger. The internal rate of return on Rob delaying until age 70—and assuming that his wife lives until age 92—is 8.94 percent, or a taxable equivalent IRR of 11.46 percent.

- Annuity Payments: Let’s say Rob has an annuity where he can start taking lifetime income. Many annuities “reward” you if you delay, like Social Security. So, if at age 67 Rob is deciding among delaying his SS into the future and activating annuity benefits right now or taking SS now and delaying activating his annuity payouts into the future, that could be some interesting analysis. For example, if the IRR on delaying an annuity payout is greater than the IRR on delaying the Social Security payout, he may want to consider taking Social Security now.

Retirement Income Software is Invaluable!

This article reflects just a few variables and components of hundreds. Therefore, each consumer should work with a financial professional that has the planning software that will project how much each filing scenario will give them over their lifetime, on an after-tax basis and after inflation basis. Then and only then will a consumer feel confident that they made the right choice. It’s better than flying by the seat of our pants. If you are a financial professional and want to learn more about software (or Social Security in general), feel free to contact me.

If done correctly and in a manner that reflects “time value of money,” you will see that the difference between filing correctly and filing incorrectly can be a difference of tens or even hundreds of thousands of dollars.