Question: Where do fish keep their money?

Answer: In riverbanks.

Question: Why are some fish at the bottom of the ocean?

Answer: Because they dropped out of school.

Question: What keeps a dock floating above water?

Answer: Pier pressure.

(See Footnotes for more jokes about Water1)

Jokes stem from the art of slightly bending familiar and simple things. Stories, like jokes, help us see something with fresh eyes.

I am an avid fan of Jesus. For one thing, I admire his use of stories in communicating truths. His stories drew from examples that his audience knew with great familiarity. Sowing seeds. Vineyards. Bushel baskets. Lamps. Rocks, thorns, good soil. Two brothers. Mustard seeds.

“Then Jesus asked, ‘What is the Kingdom of God like? What shall I compare it to? It is like a mustard seed, which a man took and planted in his garden. It grew and became a tree and the birds of the air perched on its branches.’” (Luke 13:18-21)2

As an independent financial professional you can significantly improve your powers of persuasion by tapping into this same principle. This article takes something everyone is familiar with—water—and presents possible parables using water that might help independent financial professionals communicate important financial principles.

We will consider these examples:

- The Water Cycle

- Water Will Always Find an Outlet

- Water’s Own Level

- Flowing Like Water

- Dripping Like a Faucet

- Standing Water

First Parable: The Water Cycle

The water cycle begins when water evaporates from the surface of oceans and lakes, rises into the atmosphere, cools, and condenses into rain or snow in clouds, and falls again to the surface as precipitation. “The water falling on land collects in rivers and lakes, soil, and porous layers of rock, and much of it flows back into the oceans, where it will once more evaporate. The cycling of water in and out of the atmosphere is a significant aspect of the weather patterns on Earth.”3

Scientists take frequent and detailed measurements and make models to predict changes in Earth’s water cycle.

Application: Money Cycle

As paper currency is deposited with a Federal Reserve Bank, the quality of each note is evaluated by sophisticated processing equipment. Notes that are still in good condition continue to circulate. Bills that are worn, torn, or marked in any way are taken out of circulation and destroyed. This process determines the lifespan of a Federal Reserve note.

Money Cycle varies by denomination and depends on a number of factors, including:

- How the denomination is used by the public.

- How often the denominations are used as a store of value.

- What bills pass most frequently between users.

- The notes that are most often used for transactions.

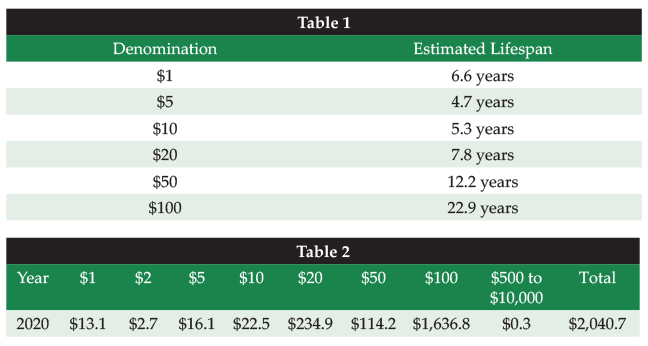

Lifespan of Federal Reserve Notes4

The Federal Reserve Board is the issuing authority of U.S. currency (see table 1) and is therefore responsible for ensuring that there is enough cash in circulation to meet the public’s demand.

“Table 2 shows the value and volume of U.S. currency in circulation calculated in billions. As of December 31, 2020, there was $2,040.7 billion in circulation, totaling 50.3 billion notes in volume.”5

(How can there possibly be $2.7 billion in circulation in two-dollar bills? Who is hoarding them?)

Point: Like scientists monitoring the water cycle, so the Federal Reserve Board monitors money in circulation.

Second Parable: Water Will Always Find an Outlet

Water always finds a way to move from wherever it is toward sea level. Water continuously changes from one form to another as it moves toward its true purpose. It follows the path of least resistance. For example, water always flows downhill. It is usually easier for water to move around a rock unless the water has enough energy. In certain instances water will move the rock rather than go around it—because it is easier.

Application: Money Follows the Path of Least Resistance

In financial matters, friction is a major influencer. People will repeat what worked previously even if the results were less than optimal. Change requires an investment of time and energy in order to gain better understanding of alternatives. Change of any kind is only so much friction.

People are generally passive decision makers rather than active decision makers. Most people choose the simplest means of saving, investing, planning, and giving when activating their own (perceived) best interest.

Example: Roth Conversions

Most people do not have enough tax diversification. Tax diversification means having investment assets in each of the three types of accounts that have different tax consequences: 1) taxable accounts; 2) non-qualified annuities, traditional IRAs, and other tax-deferred accounts; and, 3) income from permanent life insurance, Roth IRAs and other tax-free accounts.

Also, wise retirees utilize bracket management. Using this strategy, they can control their tax rate in retirement. Tax rates can fluctuate during retirement years. In a year when retirees are in a low tax bracket, they can take more money from their qualified plans or traditional IRA. When they find themselves in a high bracket or want to avoid jumping into the next tax bracket, retirees can take tax-free distributions from a permanent life insurance product or Roth IRA.

For reasons of tax diversification and bracket management, a Roth conversion may make great sense for your clients, but they will stay in traditional IRAs unless you can guide them from passivity to activity.

Point: Without wise planning, proper allocations, and wise distributions of money, money will seek the path of least resistance—resulting in retirees paying higher taxes unnecessarily.

Third Parable: Water’s Own Level

Everybody knows that “water seeks its own level” but very few people know why water seeks its own level. Three factors:

- Atmospheric pressure.

- Water pressure depending on depth.

- Water’s density.

Water pressure is primarily a function of its depth. If two bodies of water have equal depths their pressure will be equal. Consider a tube shaped like a U. Fill both sides with water. Because the water in both tubes is at rest at the bottom, the pressures in both tubes will be equal. Pouring water into one tube raises the water in the other until the pressures equalize. This is true whatever the density of water or whether or not there is atmospheric pressure.

This principle is best seen using something called “Pascal’s Vases.” You can use four glass tubes of varying shapes, all having the same height, that are all connected at the base. You pour water into any tube and regardless of the shape or volume, the water level is the same in each tube, proving that water’s pressure is dependent upon vertical height only.

Application: Money Seeks Its Own Level

The old saying, “money begets money,” is true in some regards. “Beget” (verb) means “to give birth to; to bring about.” If someone has money, it can be used to get more money through investment. This explains why the “rich get richer.”

As an independent financial professional (IFP) you can help your clients to think in terms of vertical height. Vertical height of money comes from pouring more money in and keeping money from leaking out. Clients build wealth over time. This column of money gains greater pressure, and when the money fills one need, it flows over to the next need, and eventually, into dreams.

Using a Pascal Vase analogy, one tube could symbolize paying off the mortgage, a second could be college savings, another retirement, a fourth could be a summer home, and additionally, a legacy plan could help the client give significant money away.

Point: The IFP helps clients build the vertical height of wealth in four ways:

- Keep more income through wise tax planning.

- Save more money.

- Invest more money.

- Give more money away.

Fourth Parable: Flowing Like Water

“Water is the driving force of all nature.”—Leonardo da Vinci

Water is a flow resource. It is best when moving. It is always behind life in all its forms. It is also an easy resource to waste.

Consider how many of us have formed water-wasting habits.

- Taking baths and long showers. Think of it this way: The average American shower uses 17.2 gallons of water and lasts up to eight minutes—that’s a lot of water.

- Laundry loads that are only half full.

- Washing dishes with running water.

- Running the water while brushing teeth.

- Overwatering the lawn.

Application: Stop Spending Money Like Water

We often use the phrase, “spending money like water.” We use this to describe someone who spends too much money in a careless way, who spends freely, or spends lavishly.

There is a Japanese proverb: “Getting money is like digging with a needle; spending it is like water soaking into sand.”

Let’s face it. We all waste money. We could all use a little accountability.

Debra Pangestu wrote an excellent article entitled, “How to Stop Spending Money: 7 Tips and Tricks to Curb Your Overspending.”6 In the article she used this list as her outline:

- Understand Your Spending Triggers.

- Track Your Spending.

- Stick to Cash and Stop Relying on Credit Cards.

- Forget Your Credit Cards—Literally and Figuratively.

- Set Short-Term Financial Goals.

- Learn How to Budget Money.

- Give Every Dollar a Job.

She wrote, “In many cases, knowing how to stop spending money has to do with identifying the emotional and psychological triggers that cause us to spend. If you remove those triggers, you’ll remove the temptation and opportunity to overspend.”7

Point: Every IFP is inclined to show respect to each client and is hesitant, therefore, to criticize spending behavior. But the best tool an IFP yields is accountability. Perhaps the most important step the client needs to take in order to achieve financial success is to get a better hold on spending.

Fifth Parable: Dripping Like a Faucet

According to the U.S. Geological Survey’s (USGS) Water Science School, “There is no scientific definition of the volume of a faucet drip.”8 The scientists at USGS concluded, after conducting several experiments, that the volume of a faucet drip, one drip of water, equals 1/4 milliliter (ml). Using that estimate, they calculated the extent of wasted water from a single dripping faucet as follows:

One gallon = 15,140 drips

One faucet, ten drips a minute = 14,400 drips per day = 347.2 gallons per year!

The rate of loss is too small to cause alarm. The annoyance of the drip is worse than the cost. Or so it seems.

Application: Letting Money Slip through the Fingers

CNBC Select spoke with debt-relief attorney Leslie Tayne about the common ways people waste money.9 Ms. Tayne founded Tayne Law Group, a New York-based debt relief firm. Her mission is to help people to analyze their spending habits and recognize when they spend when they do not need to. Unnecessary spending drags our budgets down. It often takes the help of an independent financial professional for people to break the habit of spending on things they can easily live without.

Examples:

- Paying for Identity theft insurance if their credit cards come with built-in protections from fraud.

- Making minimum credit card payments when they can afford more.

- Paying for unused memberships and subscriptions.

- Paying for convenience.

According to USA Today, the average adult in the USA spends $1,497 per month on nonessential items. That’s roughly $18,000 per year on things we can all do without.

“The tendency to splurge consistently on nonessentials is causing Americans to skimp on other important items. Case in point: A good 38 percent of Americans claim they can’t afford to fund a retirement plan because they don’t have enough money. Meanwhile, 35 percent say they can’t afford a life insurance policy, 28 percent can’t afford to pay off credit card debt, and 26 percent can’t afford car repairs.”10

Point: Nobody purposes to waste their money. Successful people are busy people. They are wary of accountability in their personal lives because they experience oversight daily in their working lives. Facts reveal that help is needed. It takes effort to finally call the plumber to fix the leaking faucet. It takes an IFP to help people assess their spending habits, seriously consider what they actually need, and make hard choices to stop the spending drags on their budgets!

Sixth Parable: Standing Water

The Centers for Disease Control and Prevention (CDC) publishes warnings about the disease threat and other dangers associated with standing waters.11

- Standing water can be a dangerous drowning risk for small children.

- Standing water often contains contaminants that can lead to illness.

- Exposure to standing water can cause wound infections, skin rash, gastrointestinal illness, and tetanus.

Healthy water is flowing water.

Application: Idle Money

According to Investopedia: “Idle funds refer to money that has not been invested and is, therefore, not earning interest or investment income. Idle funds are simply funds that are not deposited in an interest-bearing or investment tracking vehicle, that is, are not participating in the economic markets. These funds are often thought of as “wasted” funds since they do not appreciate in any manner.”12

How does idle money cause damage to one’s financial strength? When inflation is rising, the idle funds are in effect losing value as they are not even growing at the pace of rising costs. In addition, people everywhere are struggling financially. Charities regularly run short on funds. Underutilized funds (idle money) anywhere could be the difference in another person’s very existence.

Lynne Twist wrote a book entitled, “The Soul of Money: Transforming Your Relationship with Money and Life.” Here is a quote germane to this issue:

“Money carries our intention. If we use it with integrity, then it carries integrity forward. Let your soul inform your money and your money express your soul. Money flows through all our lives, sometimes like a rushing river, and sometimes like a trickle. When it is flowing, it can purify, cleanse, create growth, and nourish. But when it is blocked or held too long, it can grow stagnant and toxic to those withholding or hoarding it.”13

Point: Every IFP has the opportunity to make the world a better place by addressing the presence of idle money sitting in each client’s portfolio. The possibilities are endless for such funds to move from stagnation to unimagined prosperousness and productiveness.

Summary

Water is an amazing substance.

- The heat capacity of water is more than twice the heat capacity of natural mineral and rock material. Oceans tend to even out temperature differences on Earth.

- Water is the best all-around solvent. More solid substances dissolve in water than in any other liquid. Because of this, living things are made mostly of water.

- Water is never used up: It gets recycled over and over again, constantly moving between the plants, animals, rivers, and seas on earth’s surface and atmosphere.

Money is a remarkable aspect of human society.

- Human beings need money to pay for such things as shelter, food, healthcare bills, and a good education.

- Money is a universally recognized medium of exchange.

- Money provides freedom.

- Money empowers dreams.

- Money enhances the feeling of security.

- People need to save enough for the future to ensure they will have enough available when they no longer trade their labor for money.

For the independent financial planner, there is no better way to help people understand financial ideas than through the use of stories. Stories require something familiar. It is hard to find anything more universally familiar and appreciated than water.

Footnotes:

- https://kidadl.com/funnies/puns/water-puns-and-jokes-that-will-have-you-crying-with-laughter.

- Holy Bible, New International Version®, NIV® Copyright ©1973, 1978, 1984, 2011 by Biblica, Inc.®

- https://gpm.nasa.gov/education/water-cycle#:~:text=The%20water%20cycle%20describes%20how,to%20the%20surface%20as%20precipitation.

- https://www.uscurrency.gov/life-cycle/data/life-span.

- https://www.uscurrency.gov/life-cycle/data/circulation.

- https://www.mymoneycoach.ca/blog/how-to-stop-spending-money-7-tips.html.

- Ibid.

- https://water.usgs.gov/edu/activity-drip.html.

- https://www.cnbc.com/select/ways-people-waste-money/.

- https://www.usatoday.com/story/money/2019/05/07/americans-spend-thousands-on-nonessentials/39450207/.

- https://www.cdc.gov/healthywater/emergency/extreme-weather/floods-standingwater.html.

- https://www.investopedia.com/terms/i/idlefunds.asp#:~:text=Idle%20funds%20refer%20to%20money,participating%20in%20the%20economic%20markets.

- “The Soul of Money: Transforming Your Relationship with Money and Life” by Lynne Twist, W. W. Norton & Company; Reprint edition (March 14, 2017).