Some of my fondest memories as a kid have to do with being on the lake in a boat enjoying water sports. So once I had kids it became a burning desire to torture them as I drove the boat and they held on to the tubes for dear life. So, we bought a boat!

It is no secret when I say that buying a boat, in addition to the SUV that is required to pull the boat, costs a small fortune. Buying one of those items costs a small fortune let alone both of them. So, here is a thought: Wouldn’t it be nice if my Suburban also worked as a boat to spare me the cost of buying the boat and the hassle of hauling the boat around? If my Suburban came with the “Amphibious Option?” Even if that option cost a little more, it would probably be cheaper than buying a boat in addition to the Suburban. Unfortunately, GM does not offer that option yet.

Although the life insurance industry has not traditionally been known for innovation, this is an area where we have innovated beyond vehicle manufacturers (sarcasm). The “amphibious” option is indeed available with life insurance policies and annuities when it comes to long term care coverage.

Below, I want to highlight a particular product/strategy that I like. I call this product “the amphibious life insurance product.” Although I am discussing one of my favorite products here—which I can share with you if you email me—it is not about this specific product but rather the concept. Afterall, this is not the only product and rider out there of this kind. I will not name names in order to remain compliant with the carriers.

Case study: You have a 50-year-old male that would like some level of life insurance coverage in order to provide an inheritance to his kids. This client is also concerned about the expenses associated with long term care/chronic illness that he will likely experience in his later years. You, the agent, believe that $300,000 in life insurance coverage would do the job. You will also look to a product that will provide a large long term care/chronic illness benefit should he need care.

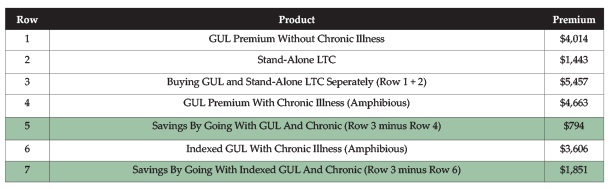

When one of my agents comes to me to ask for help in scenarios like this, one of the first things I will do is check life insurance prices across the entire industry for this particular client. To do this, I will run a report to find a list of the lowest cost policies that will guarantee his $300,000 in death benefit that will be guaranteed forever. “Forever” is defined as to age 121. This will be a starting point for how much the “SUV” costs, to use my previous analogy. Nine times out of ten the product I am highlighting will be in the top three from a price standpoint. Using our 50-year-old male (standard health) who is seeking $300k in death benefit, the product I am referring to is the #2 in lowest premium, at $4,014 per year. Again, that is just for the death benefit coverage—the SUV. This is our starting point.

However, how do we make this product “amphibious?” Where that entire $300k applies not just to death benefit coverage but also to long term care coverage? The answer to the question is, we would add a chronic illness rider to the policy which comes at an additional cost. What I tell clients is, “The old-fashioned life insurance tells you that there is only one way to get the death benefit; you have to go and die, which is not fun. However, by adding this rider, it will give you an additional trigger where you can activate the death benefit during your life. It’s life insurance, not death insurance!” Effectively what the client is doing is they are upgrading their SUV by adding the “amphibious” option that applies not just to death but also to long term care.

By adding this rider you can point to the $300,000 death benefit and tell that client that the $300,000 will be paid out—whether in life or after death. I also like the riders that do not cost any additional premium. However, the “discounted death benefit” upon chronic illness does not allow us to tell the client with certainty that they and/or their heirs will get the entire $300,000. The actual chronic illness benefit can be uncertain with many of the discounted death benefit riders because the actual cost to the client is experienced on the backend, at claim time. The rider I am discussing has no “discount” at claim time.

How much does this guaranteed universal life policy cost with the “amphibious option?” $4,663. In other words, by adding the chronic illness rider, we added $649 ($4,663 minus $4,014) to the premium. That is what it costs to upgrade our SUV to also work as a boat. Illustration Details: For this rider, I chose a maximum acceleration of $8,000 per month for the chronic illness payout. That would give us a 37.5-month benefit period, calculated by dividing the $300k death benefit by $8,000.

Even after adding the additional cost of the chronic illness rider, the premium on this policy is still within the top seven GUL policies in the industry—at least in this exact example.

So, the death benefit coverage on this product is exceptionally low cost but what about the cost of the chronic illness rider? Instead of adding the chronic illness rider to our policy, what if we bought a stand-alone LTCI policy with similar benefits? What would that LTCI policy cost per year in premium? $1,443, or $794 more than the cost of our chronic illness rider. Illustration Details: The long term care policy I illustrated provides an $8,000 per month benefit for 36 months. There was no “37.5 month benefit period” so I went as close as I could. Also note, I chose no inflation options to make it apples to apples. This is technically a $288,000 benefit pool, calculated by $8,000 per month times 36 months.

As I summarize everything in the spreadsheet, by going with the one life product, plus the chronic illness rider, the premium is cheaper than the total premium of the life policy plus the LTCI policy. The savings is $794 per year in premium. With that said, it is important to understand that you cannot market chronic illness riders as “long term care,” as that is prohibited. Also understand that stand-alone LTCI policies are much more “modular” and have many more options (inflation, elimination periods, partnership, etc.) than chronic illness riders. In other words, if I turn my suburban into a boat, I will likely be limited in how my suburban performs on the water relative to if I bought an actual boat. Needless to say, a Suburban is not an apples-to-apples comparison to a boat!

In my perfect world, everybody would have the means to buy an LTCI policy that provides at least $8,000/month benefits, with long benefit periods, and five percent lifetime inflation. However, considering we do not live in a perfect world, this strategy can provide immense value to those consumers that need death benefit coverage and also lower-cost alternatives to the fully-loaded long term care options that exist.

One more thing: You can also look to the “indexed GUL” policy that this company has. This can be a strategy to further bring down the price. Assuming a 3.25 percent illustrated rate on the indexed life policy, as well as current policy charges, what is the premium it would take to carry our $300k policy out to 121? Only $3,606. That number includes our chronic illness rider that will provide $8,000 per month of benefits for 37.5 months. For the skeptical folks (like me) that are wondering if the death benefit is guaranteed if the market were to be down forever and COI charges were to increase to the max—the death benefit is guaranteed to age 86 as long as the premiums are paid.