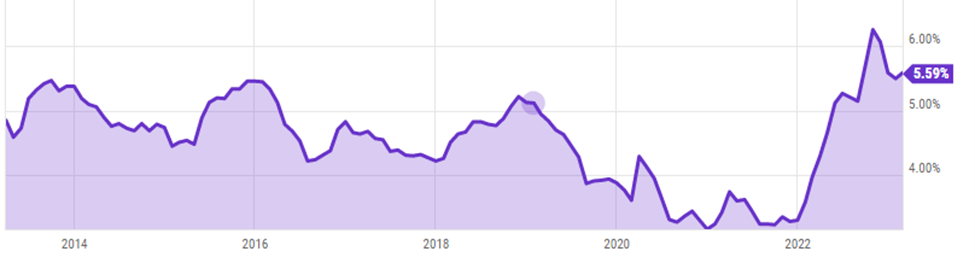

Carriers have better pricing horsepower for annuities than they have had in over a decade. By “pricing horsepower” what I am referring to is interest rates. We all know that the 10-year Treasury Bond yield has increased substantially over the last couple of years. However, a better benchmark to pay attention to for what carriers largely invest in is corporate bonds. Carriers like the additional yield that corporate bonds provide over Treasury Bonds, while maintaining “investment grade” quality. Hence, my favorite benchmark, the Moodys Baa Corporate Bond yield.

Chart 1 shows the interest rates–minus the carriers’ spread–can be viewed as the call option budget for indexed annuities, which ultimately determines the caps and participation rates. Clearly, at the time of this writing with the rate being 5.59 percent, the carriers are able to purchase caps and participation rates that are very high, at least relative to recent history.

For many agents, these rising rates and the rising rates’ impact on annuities is new territory. Because of this, I have recently had conversations with agents about the disconnect between the caps/par-rates on new policies versus renewal caps/par-rates on existing policies.

For example: I recently saw a renewal statement on a client’s policy where the renewal participation rate was 185 percent. Although that seems very high, what was the participation rate on new policies for new clients that want to purchase that same annuity today? Almost 300 percent! Naturally, this disconnect has generated questions from the agents. Let’s discuss a couple.

First, is the carrier trying to “rip off” our clients that are in the old policies?

No. Allow me to explain.

Annuity caps are based on “new money rates” that the carrier is able to invest their dollars in at the time the annuity was issued. And to simplify, the cap on the annuity will remain somewhat tied to those original rates, although there will be some ebbing and flowing as interest rates adjust and also as call option costs ebb and flow. With existing annuities, you see relatively low deviation among the caps/par-rates at issue versus caps/par-rates on renewal. The important thing to note with annuity/new money pricing is, when prevailing interest rates increase, annuity caps on new issues are very quick to respond—like what we have seen over the last year. The downside here is, as interest rates have increased and new issues are looking great, the renewal rates on seemingly identical older policies are not keeping up! Why is this? Because, remember, new money pricing “kind of” anchors the annuity pricing to the original bond rate from when the policy was originally purchased X years ago.

Annuity/New Money Pricing is in contrast to “Portfolio Pricing” that carriers often use with life insurance. With portfolio pricing, the blended rate of the insurance carriers general account (or large “tranches” within the general account) is what determines the cap/par rates on IUL, whether those IULs are new IULs or renewal IULs. Over time, that multi-billion-dollar chunk of investments will slowly go up and down with prevailing interest rates. The overall interest rate of the general account is very slow to respond because the carrier’s general accounts are so large. Those general accounts always have bonds that come to maturity and are being replaced, but only a relatively small chunk at a time.

Furthermore, with the life insurance general account pricing, the carriers are generally able to keep new issue caps/par-rates in lockstep with the renewal cap rates on existing policies, at least for the same generation of product. (Note, it is a common practice for carriers to launch new generations of products where the carriers can more easily disconnect the renewal-caps/par-rates from the new-issue cap/par-rates, but that is a conversation for another day.)

The positive side to “Portfolio Pricing” that most life carriers use is when interest rates are rapidly decreasing. When this happens, there is a significant lag in the amount of time it takes for that giant portfolio to get watered down by the lower rates. For instance, for the longest time we saw IUL caps on new IUL policies hold “relatively” stable while the annuity caps on new issues plummeted because of dropping interest rates. Now the inverse is happening with annuities. Rates are spiking up and new-issue annuity caps are as well. But agents are left wondering why the annuity renewal caps are not increasing as well. It all has to do with the “New Money” pricing that annuities use. So, the answer is , the carriers are generally not playing games by purposely keeping renewal caps low relative to new issues.

Now, with what I just said about annuities, many agents are wondering if it would make sense to “surrender” old annuities to get the better pricing. The answer is, it depends on the scenario. Also, it depends on the carrier. Many carriers have rules such as, “As long as the net loss (after premium bonus is taken into consideration) is less than two percent or three percent, then we will allow you to use our annuity to replace the old annuity.” Of course, that is me paraphrasing.

Also remember, this interest rate environment that we are in is exactly why “Market Value Adjustments” on annuities were created—to insulate the carrier from the bond losses they would have if your clients cashed out their annuities after interest rates have increased. It is no coincidence that the MVA formula in most policies is a similar formula as the formula for bond pricing. With bonds that the carriers are buying, as interest rates increase the value of their bonds decreases. With an annuity, as interest rates rise, the client’s surrender value decreases, all else being equal. The MVA is the mechanism the companies use for passing through bond losses or gains to the clients, at least if the clients are going to cash out their annuity prematurely.

We have all read about the failed Silicon Valley Bank that had to liquidate treasury bonds at a severe loss, which accelerated their demise. This loss in their treasury bond portfolio was because of one thing—rising interest rates that diluted the bonds’ values. If the bank had a way to pass on those losses to consumers, it may have helped. Alas, that is not how bank products work. With annuity contracts however, insurance companies have the luxury of having “MVAs” that provide some insulation against interest rate risk (the risk of rising rates).

So, if you are considering surrendering a client’s annuity to go into a new one, understand that there is a lot to take into consideration such as:

- Market Value Adjustments

- Carriers’ rules on “replacements”

- Losing a “benefit base” that may be very high on the old policy

- Losing an enhanced death benefit

- Fees on the new policy versus fees on the old policy

- Comparing new guaranteed income levels to that of the old policy

- Premium Bonuses on new policies to offset surrender charges on the old

On the last point about Premium Bonuses: There are great premium bonus products out there that may help put the client in a better position than what the client currently owns. These premium bonuses can often offset surrender charges and MVAs. But, there are also premium bonus products that may be inferior to the existing product the client currently owns. Premium bonuses are rarely given because the carrier just wants to be nice. That pricing is always made up elsewhere in the product.