Something that I don’t think advisers talk enough about is the “death penalty” that the IRS assesses to the surviving spouse. What do I mean by this? Many times when one spouse dies, the surviving spouse generally gets a tax increase. This is because, once one spouse dies, it is not like the “taxable income” to the surviving spouse immediately reduces by 50 percent. And without a 50 percent reduction in taxable income, that generally means a tax increase to the surviving spouse. The bestselling author of The Power of Zero—David McKnight—discusses this a lot, but in the following paragraphs, I want to put numbers to it to demonstrate the various flow that makes up this “tax increase.”

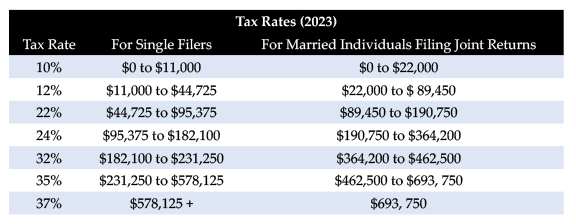

In the chart below are the 2023 federal tax brackets. As you can see, married individuals filing jointly can have twice the taxable income for a respective tax bracket than what a single filer is allowed for that same tax bracket. What this means is, again, unless the surviving spouse is recognizing taxable income that is half or less than what the couple was getting prior to the death, it will generally be a tax increase. (One exception to this is how Social Security taxation works, but that is for a later conversation.)

Let’s give a quick example. (Note: This is fairly simplified and is assuming that Bob and Jill are using the standard deduction as a large majority of Americans do.)

Bob and Jill

Bob and Jill are both aged 75 and have a total retirement income of $100,000 per year. Their income is comprised of the following sources:

- $30,000 (Social Security for Bill).

- $20,000 (Social Security for Jill).

- $30,000 (IRA Annuity Payments from a GLWB (Joint Payout).

- $20,000 (Required Minimum Distributions).

Bob tragically passes away in late December of 2023. What does their joint tax return look like for 2023? We will then compare that to Jill’s tax return for 2024, in order to demonstrate this “Death Penalty.” We will also be assuming the exact same tax brackets and standard deductions in both tax years for simplicity.

2023 Tax Return

(Note: In the year of death, Jill is allowed to file as “Married Filing Jointly” as we do below.)

Income Subject to Tax:

- $42,500 (85 percent of their Social Security Income that is subject to taxation because they made over $44,000 in Provisional Income).

- $30,000 IRA Annuity Payments from a GLWB (Joint Payout).

- $20,000 in Required Minimum Distributions from securities.

$92,500 (Total Income Before Standard Deduction).

Standard Deduction:

- $27,700 (Regular “Married” Standard Deduction).

- $3,000 (Additional $1,500 per person for being over age 65).

$30,700 (Total Standard Deduction).

Taxable Income:

- $92,500 (Total Income Before Standard Deduction).

- -$30,700 (Total Standard Deduction).

$61,800 (Taxable Income Subject to “Married Filing Joint” Tax Brackets).

Total Tax in 2023:

(Note: Tax brackets are “marginal,” meaning that although Bob and Jill are in the 12 percent tax bracket, not every dollar is taxed at 12 percent.)

- $2,200 (The first $22,000 of Taxable Income multiplied by 10 percent).

- +$4,776 (The remaining $39,800 ($61,800 — $22,000) taxed at 12 percent).

$6,976 Total Federal Tax Due.

Now let’s move on to the 2024 tax return and assume the same income to Jill (except for the Social Security on one life that she will lose). Again, this is simplified because we are assuming the income levels per tax bracket remain the same in 2024, although this is unlikely due to the “inflation adjustments” that occur in most years to the brackets.

2024 Tax Return

Note: This is the year after death and therefore Jill is filing as “Single.” She is not a “Qualifying Widow.”

Income:

- $25,500 (85 percent Social Security Income Subject to Taxation. Jill inherited Bob’s $30,000 Social Security payment. Jill’s Provisional Income is over $34,000.)

- +$30,000 IRA Annuity Payments from a GLWB (Joint Payout).

- +$20,000 in Required Minimum Distributions from securities.

$75,500 (Total Income Before Standard

Deduction).

Standard Deduction:

- $13,850 (Regular “Single” Standard Deduction).

- +$1,850 (Additional “Single” Standard Deduction for being over age 65).

$15,700 (Total Standard Deduction).

Taxable Income:

- $75,500 (Total Income Before Standard Deduction).

- -$15,700 (Total Standard Deduction).

$59,800 (Taxable Income Subject to “Single” Tax Brackets!).

Total Tax in 2023:

(Note: Jill is now filing off the “Single” tax brackets. She is now in the 22 percent tax bracket, versus the 12 percent that Jill and Bob were in when they filed “Joint”.)

- $1,100 (The first $11,000 of Taxable Income multiplied by 10 percent).

- +$4,047 ($33,725 taxed at 12 percent. This is the entire length of the 12 percent bracket).

- +$3,316 (The remaining $15,075 ($59,800 minus $44,725) taxed at 22 percent).

$8,463 Total Federal Tax Due!

Summary:

This scenario is actually more ominous than it looks. You may be looking at the difference in “Tax Due” between the two years as being very minimal. After all, Jill is only paying an additional $1,487 ($8,463—$6,976) in taxes. However, there is more to this story than just that number.

Bob and Jill were previously living off of $100,000 in income coming from Social Security, their annuity with a GLWB, and the RMDs coming from the securities. As far as true “after tax” purchasing power, they were “netting” $93,024 that they could spend on travel, food, etc.

Conversely, after Bob died, Jill was only getting $80,000 in income. This is because she lost her Social Security in order to take the higher of the two—which was $30,000 from Bob. That is how survivor benefits generally work. How much was Jill taxed on the income she was getting of $80,000? More than when she and Bob were raking in $100,000! The above tax increase to Jill after she experienced a $20,000 pay cut is certainly a rude awakening to many widows/widowers. The tax situation can be mitigated by looking at items like Roth conversions and cash value life insurance, as David McKnight discusses.

In the end, between losing one of their Social Security payment streams and the tax increase, this meant that Jill was getting a “net” of $71,537 ($80,000 – $8,463). Relative to what Jill and Bob had to spend prior to Bob’s death, this is a decrease of $21,487 or 23 percent!

There are studies that say that when the spouse dies, the survivor will naturally spend less. I often wonder if that is because the surviving spouse truly has a desire to spend less, or because it becomes a necessity to do so in order to not run out of money. My opinion is, it should be up to the surviving spouse if he/she wants to stop spending. At least giving him/her the option would be nice. How do you provide these options? In addition to a “Tax Free Retirement,” I think a life insurance policy to fund that $21,487 annual gap would be a good starting point… But it has to be earlier than age 75.