I remember as a kid occasionally being forced to watch old western cowboy movies. That is because, like every other household back then, we only had one TV growing up! Crazy, I know! And unfortunately my dad’s choice of what to watch took priority over mine. Anyway, I remember being perplexed as I would watch a cowboy pull up to a bar and get off his horse to merely throw the little leather “horse leash” one time around the post outside of the bar. I thought, “How does that loosely wrapped small leather string keep those big strong horses tied to the post?” Afterall, the slightest effort by the horse to “unleash” itself would show the horse that it can easily run off.

The reason the horses never tried to pull the leash off the post–even though it would be easy to do–is because they have been conditioned to believe that it is a lost cause. Once upon a time that horse was broken by a real leash that was very much tied down to a very solid post. I once worked for an old cowboy neighbor of mine where I would feed his horses and I once helped him “break” a young horse that had never been tied down and never ridden. For this horse who had not yet been “conditioned” to be tied up, he actually ripped the post out of the ground.

There is also a process for horses to get “broken” when it comes to being ridden. Needless to say, horses aren’t born being comfortable with a 200 pound man crawling on their backs. Conditioning a horse (also known as breaking a horse) is the process of getting the horse to realize that pushing back is more of a risk than just conforming.

Although the horse is likely correct by “just conforming,” that mentality of being “broken” rears its ugly head in many areas of a human being’s life, whether it is in our finances, our work, or our personal life.

Being “Conditioned” With Financial Products

Our brains are one of the most complex things on earth. These little three pound organs between our ears have over 100,000 miles of blood vessels in them. We as humans are the smartest species on earth, outside of maybe a dolphin. Paradoxically, because we are so smart, we can be so “not smart” because we tend to overthink things and allow our brains to condition us to believe that the world is different from reality.

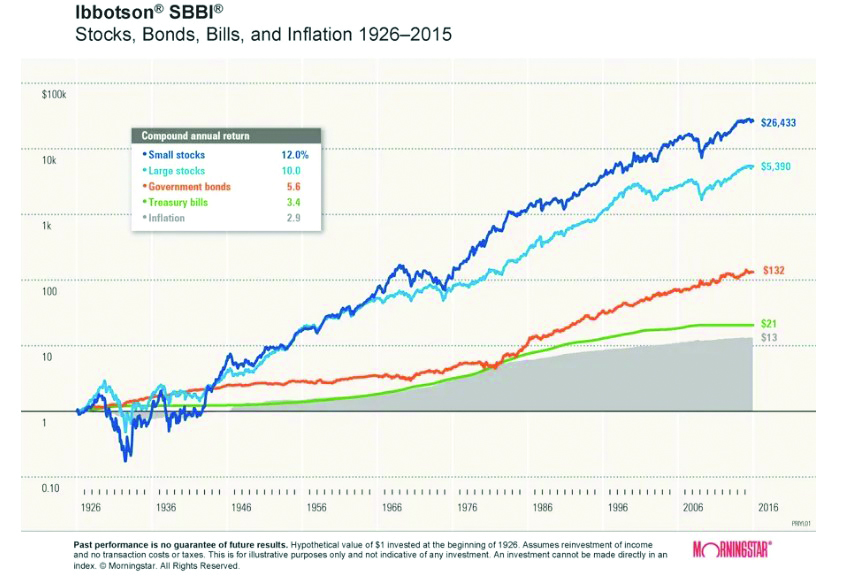

For instance, we have all seen the Ibbotson “Stocks, Bonds, Bills, and Inflation” chart. Of course, when many people look at this chart going back to 1926 they conclude that stocks are the way to go. Afterall, this chart is one of the most widely used charts by money management firms that has ever been created. Over the years I have heard many securities focused folks point at this chart as proof that stocks are the way to go. Well, although I do like securities for those with a long-term time horizon, I don’t focus on the top two lines so much as I do the bottom two lines; Treasury Bills and Government Bonds.

What do the bottom two lines tell me? They tell me that our perception of risk versus risk-free can be warped. Those bottom two lines were the only two lines to not keep up with inflation over the long run. Thus, Treasury Bills and Government Bonds were the only two on this chart to lose money (after inflation) over the long run. Yes, at the beginning of the chart during the great depression, stocks were horrible. However, if you had your money in T-Bills or Government Bonds from 1926 to 1980, you lost money after the effects of inflation. But at least the investor “felt safe” right? Perception is not always reality.

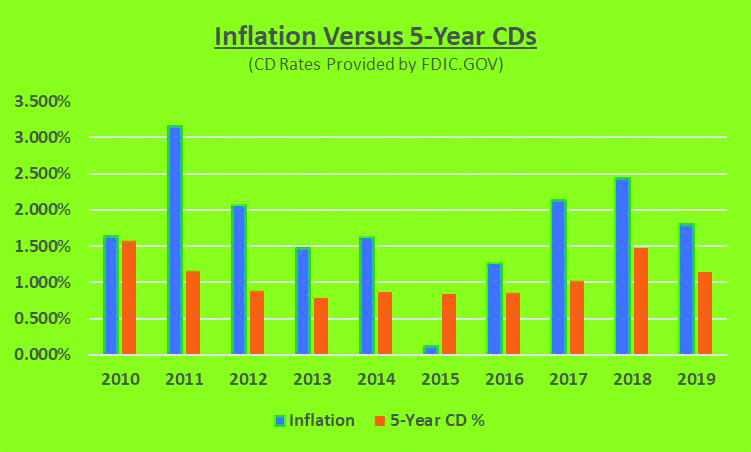

The point here is not about stocks versus bonds. The point is, risk is in the eye of the beholder. I’ve included my bar chart for inflation versus the average 5-Year CD rate over the last 10 years. By looking at this bar chart I would say the orange bars represent a fairly risky place to put one’s money! Yet for decades consumers have always looked to CDs and the massive brick and mortar banks that sell them as “safety.” (You can email me to get a copy of this graph.)

Furthermore, today a five-year “Jumbo CD” is yielding .38 percent per FDIC.gov. Thirty-eight basis points! So, if inflation is two percent over the next five years, you would be guaranteeing yourself a loss of 1.62 percent per year. Risk is in the eye of the beholder and consumers have grown accustomed to believing that CDs, Government Bonds, and T-Bills are “safe.”

Consumers need to know that their retirement savings are equivalent to the horse being tied to a flimsy post with a flimsy leather string. There are other options.

Being “Broken” in Your Career

If you are one of the 30+ million that has recently lost his or her job and has ever contemplated opening your own business, this is for you. Or, if you are a financial professional who is “captive” and has thought about going independent, this is for you. For those of you that have taken this step already, you probably can connect.

Two years ago, October 2018, I decided to leave corporate America after almost 20 years. Some people would have considered me crazy because I had done well in the corporate world and some would have thought of me as a “lifer.” Plus, why would I not continue the corporate route? When you work “for“ somebody you have the comfort of that paycheck that comes in every-other week, right? Conversely, when you work for yourself, you do not have that security blanket.

I would argue that society in America has “conditioned” us to believe that the guarantee of a paycheck is the definition of security and safety in our careers. I would argue that this can be the equivalent to the horse being tied up to a post by a tiny string.

December of 2018 is when I officially created my LLC, CG Financial Group–an Independent Marketing Organization. Around that time I was sitting with a good friend of mine talking about business. Twenty years ago he was an executive for a major transportation company, and he decided that he had enough of what he was doing. He left a comfortable job, a comfortable six-figure income, and started his own agricultural manufacturing business. To say the least, he has done very well from a financial standpoint as well as from a personal standpoint. He has a ton of money, a great family and has been married for a long time.

As we sat in his multi-million-dollar house there was something he told me that I thought was very well articulated. Effectively, he said that we as humans are conditioned to think of risk in certain ways. We are conditioned to think of risk as just uncertainty. We have been conditioned to expect that paycheck every-other week and by not having it we would be fed to the wolves. The “certainty” of a paycheck is the tail that wags the dog. He went on to say the below:

“So many employees go through their careers dealing with the volatility that their employers can subject them to with bad corporate decisions, misguided decision makers, layoffs, pay cuts, etc. All for that guarantee of a paycheck! For those employees that are in debt up to their eyeballs, that paycheck is probably a reasonable security blanket. However, if one has the liquidity, the skills, and the gut feeling that they could make it on their own, it’s a different story. For these folks, to stick with what they have always been “conditioned” to do brings on more risk and less reward than them opening up their own business.”

Of course, I am not suggesting quitting your job today. I am merely saying that this wonderful country we live in has given us luxuries that can skew our perception of risk/reward.

Do you ever wonder why it is that those that came from very little can turn into such a success? Because they have never been “conditioned” or “broken.” One of my best friends is now a very prosperous doctor who grew up in some very rough streets in India where he never experienced the security of a semi-monthly paycheck. Not long ago he came to America and now has several GI clinics across the country. Typically I would say, “He came to America and took risks,” but that would be inaccurate. By him leaving India, where he had no paycheck, to come to America, where he also had no guarantee of a paycheck, was not a “risk” for him because he had not yet been conditioned/broken.