To immediately squash the suspense, you are not going to read this article and see that one type of long term care policy is better than the others. It is solely dependent on what the consumer is looking for that will determine their “best” choice. As I will show you in the included table, each of the three product areas that I will be discussing excels in one area where the other two may not. It is all a matter of what the consumer is looking for.

The purpose of this article is to compare a few of the various options from a numerical standpoint so that, whether you are a financial professional that is not yet “long term care savvy” or a consumer that is looking to address this very prominent risk (long term care), this article is for you.

I will not get into the weeds a whole lot in this article with things like reimbursement, indemnification, shared care, tax deductions, partnership, etc. In this article I wanted to show you how I usually start my analysis of the various long term care options that exist today which, again, is largely about numbers. Usually, after I look at the numbers is when I will drill down from there and get into “the weeds”—which is beyond the scope of this article.

The obvious main reason that people buy long term care insurance is so the insurance company pays a benefit—usually identified as a daily benefit or monthly benefit—if that person can no longer take care of themselves. Common triggers for these benefits to be paid out are: To be unable to perform two of the six activities of daily living for a 90-day period of time or to have severe cognitive impairment.

Although the above reason for purchasing long term care insurance may seem obvious, choosing one long term care product over another usually has to do with much more than just what the long term care benefit is. For instance, one consumer may be concerned about the policy being a “use it or lose it” proposition. Meaning if the consumer just dies without ever needing the long term care benefit, then what would the beneficiary get if anything? Another consumer may be concerned that they may want to change their minds ultimately and not pay for long term care insurance anymore. Can they change their minds without losing everything they put in?

Because of the above concerns by consumers, as well as historically low interest rates for the longest time that have forced insurance carriers to think outside the box, we have had huge product innovations in the long term care insurance space. These innovations are indeed wonderful but could also be confusing to a consumer looking at the various options. Furthermore, financial professionals are oftentimes confused with the various long term care options that exist today. So, this article is to give everybody ideas on how to compare long term care options, at least at a high level. Future articles might get in “the weeds” a little more.

The Numbers: Live, Die, or Quit

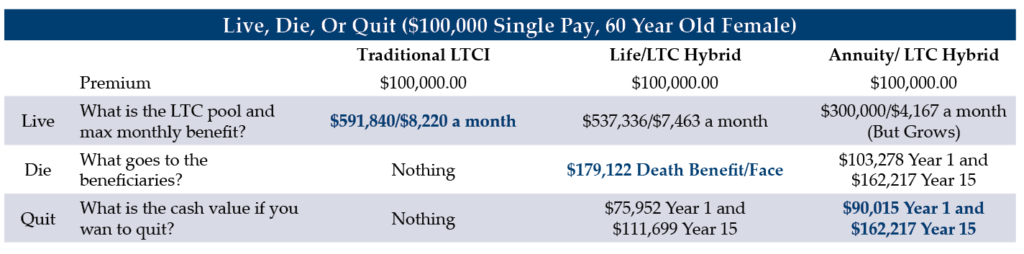

The spectrum that I compare the various long term care options on is the “live, die, or quit” spectrum. In analyzing products, I will plot out—whether mentally or on a spreadsheet like the included chart—the values of each policy across three different objectives.

- Live: If the client lives and needs care, what is the total long term care benefit that can be paid over the client’s life and also the maximum monthly benefit that the consumer can get access to if he/she triggers the benefits?

- Die: What if our client dies without ever needing long term care benefits? Did they waste their premium or is there a death benefit? Example, traditional LTCI has historically been known to be a “use it or lose it” proposition.

- Quit: What if the client wants to quit? For whatever reason he/she no longer wants the policy. Is there a surrender value that he/she can get access to, or was it all for nothing?

I plotted out three different product types across my Live, Die, Quit spectrum. The product types are:

- Traditional Long Term Care Insurance

- Hybrid Life/Long Term Care Product

- Hybrid Annuity/Long Term Care Product

The Lazy Money Scenario

When I ask consumers that do not have long term care insurance how and from what source they will pay for their long term care if they need it (which is very probable), they will usually point to their savings account or certificates of deposit. That is a natural inclination because that is money that is generally more “liquid” than their IRAs or 401ks. That is when I will show them the power of moving that “lazy money” (that is likely not earning much interest) over to one of these products. By doing so, they can oftentimes get more interest on their money, more death benefit, and/or use the power of leverage when it comes to long term care buying power. Their money is now working for them instead of being lazy! Allow me to explain.

The chart assumes a single premium moving into each of our three products. There are no more premiums that our consumer needs to pay in this scenario. This is the simplest scenario to look at when differentiating products because it easily shows the long term care leverage per dollar of premium, the death benefit leverage per dollar of premium, and the liquidity per dollar of premium. I could have also made a chart with “ongoing premiums,” because not everybody has $100,000 laying around and may prefer to spread the premiums out. However the overall story on the long term care leverage and death benefit leverage would also apply to the ongoing pay scenarios, just to a different extent. (Ongoing premium example, the same benefit on a traditional LTCI policy that is paid for life would only be around $5,000 per year, versus a lump sum of $100,000.)

It is important to point out some details before jumping into the chart. The annuity is very rigid in that it has limited options in benefit periods. This product triples the consumer’s money for purposes of the total lifetime long term care pool. Again, the money is working immediately! Now, if one needs care, they cannot take the $300,000 (triple of our $100k) out all at once. It has to be spread over 72 months. In other words, the benefit period is 72 months, which makes the maximum monthly long term care benefit $4,167 ($300,000 divided by 72). For these long term care annuities, this 72-month benefit period is a common design although there are some annuity offerings where you can choose other benefit periods. My point is, although the traditional LTCI and the life/long term care hybrid can have shorter benefit periods—which means higher monthly maximums—I illustrated all of these products to have a 72-month benefit period. I wanted to keep it as “apples to apples” as possible. I also kept it simple without choosing inflation options on the benefit.

Who Wins in What Scenario?

- Traditional LTCI: Traditional long term care insurance has the most long term care leverage of any of these products, as represented by the green highlight. This product will give our 60-year-old female a benefit pool of almost $600k and a monthly benefit of $8,220. If it is purely long term care leverage without regard to other bells and whistles, traditional LTCI wins. Now, although there are sometimes return of premium options on traditional LTCI that can potentially give a beneficiary a death benefit, I did not illustrate it here because I wanted to demonstrate the significant long term care leverage that traditional LTCI can provide. That leverage gets watered down when you add the ROP. The “Live” scenario is where LTCI shines! Also, traditional LTCI is very modular as far as various benefit periods, inflation options, shared care, etc. Again, let’s keep this bearable!

- Life/LTC Hybrid: Because this is whole life insurance at its foundation, you can guess that the “Die” scenario is where this generally beats the other two options. The death benefit is the highest at $179,122 for our 60-year-old female. It also provides cash value that grows on a guaranteed basis. As you can see, the cash value is only $75,952 in year one, but it grows throughout the life of the contract (assuming no withdrawals or claims). If she “Quits” the policy in year 15, although not advised, she would get back $111,699. This particular policy pays benefits on an indemnification basis versus reimbursement but, again, let’s not go there for now.

- Annuity/LTC Hybrid: Because this is on an annuity foundation, the consumer’s money has the ability to grow, even after the monthly long term care charges. Thus, this product generally wins the “Quit” scenario. This annuity pays an interest rate of 4.5 percent (as of this writing) in year one and can adjust thereafter. If she “quits” in year one, she can get out $95,015 after surrender charges. (Note: This product is a nine-year product.) If she “quits” in year 15, she can get back $162,217, assuming the 4.5 percent remained constant up to that point and no withdrawals or claims were paid. The “Die” scenario is very good as well as her beneficiaries will get back the accumulation value that is free of surrender charges at any point in time should she pass away. This policy has the lightest underwriting of any of them, but again…

As you can see, there are various reasons for various consumers to choose any one of the products. Not any one is “the best” until the financial professional knows what the consumer is looking for.