There are a few annuity and life insurance social media groups in which I am a “group expert.” These social media chat groups are closed groups that are only available to financial professionals where they can ask questions and comment on ideas and strategies that are working for them. It is also a forum for which other financial professionals can respond to the feedback and strategies communicated.

Some of these groups have thousands of financial professionals in them and are wonderful resources, not just for the agents but also for me as an independent marketing organization. These forums not only allow me to contribute but also allow me to learn what is on the minds of the agents.

With the large quantity of financial professionals in these groups and also the ease of those financial professionals to just type up a message and let it fly, it can serve as unfiltered insight into what is working, what is not working, misperceptions, etc. When I say it is “unfiltered” that is because it is extremely easy for some people to speak their mind when they are sitting behind a computer. If you have ever spent any time at all on a social media platform, you know what I am talking about. Unfortunately, sometimes the conversation goes something like the below. Pardon the satire but I’m sure you understand:

Person trying to help: “I think oranges are a great tasting fruit because…”

Person that knows nothing about the conversation topic: “Are you kidding! Apples are horrible! I would never recommend them to my clients. Make sure your E and O is updated.”

Person trying to help: “I am talking about how oranges are great tasting fruits, not apples.”

Person that knows nothing about the conversation topic: “Who would ever recommend apples to clients? Plus, they are not fruits, they are vegetables. That is stupid. My Brazilian Butternut Cantaloupe is ten times the vegetable that your apple is.”

Person trying to help: “I’m talking about oranges and fruit, not apples and vegetables!”

Person that knows nothing about the conversation topic: “I see, so now you’re trying to change the topic huh?”

And before you know it, the strategy that you wanted to share about your oranges has gone the way of the dinosaur, kind of like my point to this column, as I have digressed.

What is my point? My point is that I see a lot of glaring misperceptions that are often laid out very publicly and obviously, although a little more nuanced than apples versus oranges. Much of those nuances have to do with the complicated world of long term care hybrid products. So, why not address some of those examples where I have seen rampant confusion. By the way, although I poke fun in my social media example above, much of the confusion around hybrid products is warranted as the industry has gotten very commingled and more complicated. But don’t take “complicated” as not exciting, because the long term care hybrid world is indeed extremely exciting and lucrative if you know what you are doing.

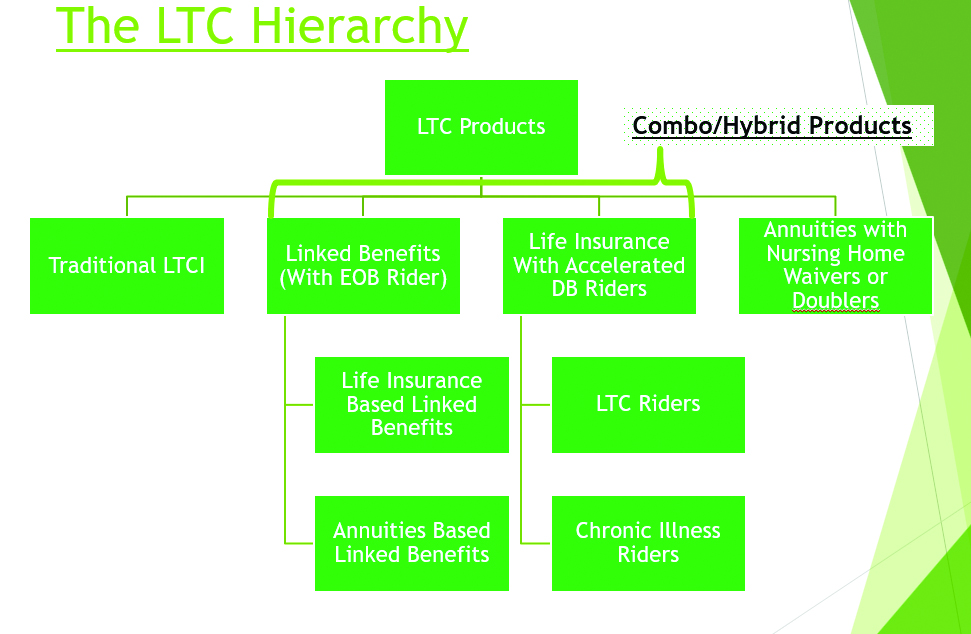

Not Many Understand The Entire Universe Of Long Term Care Products

If you are a visual person like me, a slide from one of my agent training decks will help us visualize the universe of long term care products. This may not be the “entire universe,” but it is close!

The slide shows that the universe can be broken into three different “worlds.” Although there are exceptions, what I tried to do was to arrange the chart to demonstrate the products with the most long term care leverage on the left, with the leverage dropping as you move to the right. Of course, when we get into single pay scenarios (life and annuity) it gets a little more complicated however.

Starting from the left, you have the granddaddy of them all, traditional stand-alone long term care. To oversimplify, this works like health insurance. Again, it will generally provide the most long term care leverage, per dollar of premium.

Secondly, you have the “world” that represents a large majority of the entire universe today—as measured by industry wide cases sold. These are the combination/hybrid products. These are annuities or life insurance with a long term care benefit attached in the form of a “rider.” Within this world you have several variations of these combo/hybrid products. We will come back to this because this is where much of the confusion lies—and thus opportunity.

Third, you have annuities that have waivers of surrender charges for nursing home confinement or “doublers” on the GLWB payouts. The long term care protection afforded by these products are usually a distant need relative to the other benefits these annuities possess. The long term care benefits on these generally have no underwriting.

“Combination Products” Is Not Synonymous To “Linked Benefit Products”

As you can see from the graphic, the “Combo/Hybrid” world is separated into two different continents, the Linked Benefit continent, and the Accelerated Death Benefit continent. Let’s start with the accelerated death benefit products.

Accelerated Death Benefit Products: These are usually life insurance-based products where the death benefit (and no more than the death benefit) can be accelerated for the purposes of a long term care event or a chronic illness. When I present this product, I like to point out that the life insurance of the old days typically had one “trigger” in order to access the death benefit—death. Well, today’s life insurance is life insurance, not death insurance.

Accelerated Death Benefit Riders are where the insured can actually get relief out of the product during their lifetimes in the event of a chronic illness or a long term care event. Thus, the two prominent rider types offered within this category are “chronic illness riders” and “long term care riders.” Once upon a time chronic illness riders required a permanent condition, which made true long term care riders generally more attractive than the chronic illness riders. Since NAIC Model Reg changes in 2014, this condition of permanence is no longer the case for the most part. Therefore, the differences between long term care riders and chronic illness riders are very slim.

Linked Benefit Products: Again, linked benefit products are a subcategory of the broader “combination product/hybrid” world. People tend to think “combo products” are “linked benefit” products and vice versa. Not so! One is a sub-component of the other.

These products are usually life insurance products where there is a long term care “pool” that is created that can be multiples of the death benefit provided by the underlying life insurance product. Of course, the additional long term care pool would come at an extra cost and possibly additional underwriting relative to just an “acceleration” product.

A linked benefit life insurance product might give two to three times the death benefit in the form of a long term care pool. The long term care benefits that go beyond the total death benefit are through the use of a “continuation of benefits” or “extension of benefits” rider. Thus, the COB/EOB is the primary difference between the linked benefit category and the accelerated death benefit category.

Real Life Numbers (Company Name Omitted): The client is a healthy 55-year-old female. She does a single pay of $100,000 in premium into XYZ Linked Benefit life product. The death benefit is $152,000 and the long term care pool is $456,000. (Note: Benefit periods, etc. I won’t go into here.) When the client goes on claim, the $152,000 that is the death benefit is used up first as an “acceleration of death benefit.” Once that is depleted, the client moves into the second phase, the continuation/extension of benefits. Again, it is that second phase that separates the linked benefits from the rest of the combo/hybrid world.

As noted in last month’s column, one of my favorite products is actually a “linked benefit” annuity product that triples the clients premium for purposes of long term care, with almost no underwriting! That is the box on the lower left side of my graphic. Think “Live, Die, or Quit.” If the client lives and needs care, he/she gets three times the contract value. If he/she dies, the bene gets the contract value, which is what the client put in plus growth (usually). If he/she wants to “quit,” they get the contract value—or surrender value if within the surrender period.

Chronic Illness Riders Are Generally Not FREE!

The most common misperception that I see is the notion that chronic illness riders on life insurance are free. Unless there is one in some corner of the industry that I have never seen, I will say they are not free. You either pay for them upfront via an additional premium (morbidity charge) or the client pays on the backend when they elect the chronic illness payout. There is also a third—a lien structure—that I won’t go into here.

The most common chronic illness structure is the “backend,” otherwise known as the “discounted death benefit” structure. To be clear, there is no cost on this rider if the client never uses it—which is one of the reasons to like this type of rider. However, if the client uses it, the ultimate cash in hand to the client is less than what the death benefit was actually reduced by. The difference between those two numbers is effectively the cost to the client and the beneficiaries. Example: Client goes on chronic illness claim and the death benefit is reduced by $100,000. How much cash might the client get in hand? Maybe $80,000. Hence, the $20,000 difference between the death benefit reduction and what was received can be considered the “cost.”

With the discounted death benefit design, the amount that a client ultimately gets is usually not known until claim. That is because the calculation is usually the death benefit discounted back to the date of claim by a discount interest rate that is not known until the actual claim. Again, however, if the client never goes on claim they never paid a penny for the rider. It is a great rider, but it is important to note that it is not always “free.”

One of my favorites is an “upfront” rider that does have the additional charge to the client as they pay their premium. Why do I like this one? Because the client knows exactly what they will get when it comes time to claim. There is generally not a discount on the death benefit on these types of riders. You either pay upfront, or you pay on the backend. With this rider, you can point to the death benefit on the ledger and tell your clients that whether in life or after death, somebody will indeed get that value. Of course, as long as they pay the premium!

Summary

There is a lot to know about the long term care Universe. We did not even get into reimbursement versus indemnification, 101g versus 7702b, per diem limits and taxation, etc. One thing I learned a long time ago is that there is no life, annuity, or long term care option that is “the best.” It is client specific. A benefit that is “the best” for one client, may be too expensive for another. Said another way, with these products there is always a counterbalance that makes the task of finding “the best” not so simple.

I am going to eat my orange now.