Recap: In last month’s column I discussed the two opposite ends of the spectrum when it comes to funding a life insurance policy, specifically indexed universal life insurance. Those opposite ends are, the death benefit focused side and the cash accumulation side. I also discussed how “overfunding/max funding” works from a mechanical standpoint in reducing COI charges. To summarize in an over simplistic way, we want the cash value and death benefit lines as close to together as possible if we are going for maximum accumulation! If you would like a copy of last month’s column, email me and I will send it to you.

I ended last month’s column with a “teaser” on a question that tripped up my agent in his sales presentation to his client Brian. By the way, I am not picking on this agent in particular because this is a common issue I address with many agents as I help with the more “advanced” case designs. What was the question that the client had that created confusion for my agent? Here is the question from his client that tripped up my agent which seems very basic on the surface: “If I want a higher death benefit than the ‘minimum death benefit’ on this product, can I go with a higher death benefit?”

Of course, the simple answer is, yes! But is that the best answer? Although the “minimum non-MEC death benefit” for our healthy 45-year old is $231,000 when he is funding it at $10,000 annually, the agent can illustrate a higher death benefit than that “minimum”—up to a certain level of course. However, if you really understand the mechanics of cash value life insurance, you know there should be much more analysis involved than just jacking up the death benefit in the IUL illustration and calling it good.

Generalization or Specialization?

The client, Brian, was wondering if he can get an additional $100k of death benefit on top of the $231k within the same product. He wanted to see if he could get this additional coverage for 20 years. Again, the answer is yes, he can do this, but is that the right way to go? Afterall, what started out as a case focused largely on accumulation has now morphed into an accumulation and death benefit focused policy. What is the intent of the product—accumulation or death benefit? Can you buy a golf club that makes a good putter and a driver at the same time? Or, do you need to separate out products? When looking at cash value life insurance, should products satisfy general objectives or are the products more specialized? Let’s discuss my view on this.

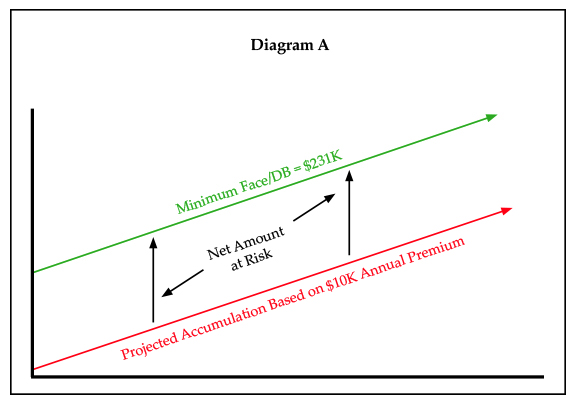

Following are two diagrams: The purpose of these simple diagrams is to demonstrate the relationship between the $10k premium going in, the two different death benefits over time and also the “Net Amount at Risk.” Again, in both diagrams we chose the “Increasing Death Benefit” in the early years for reasons I explained in last month’s column.

In Diagram A is a graphic of our first 20 years or so in the policy without the additional $100,000 in death benefit included. Per the illustration, based on $10,000 per year in premiums, the minimum “non-MEC death benefit” is $231,000. As we have already discussed last month, the difference between the two lines is the “Net Amount at Risk” that determines the COI charges.

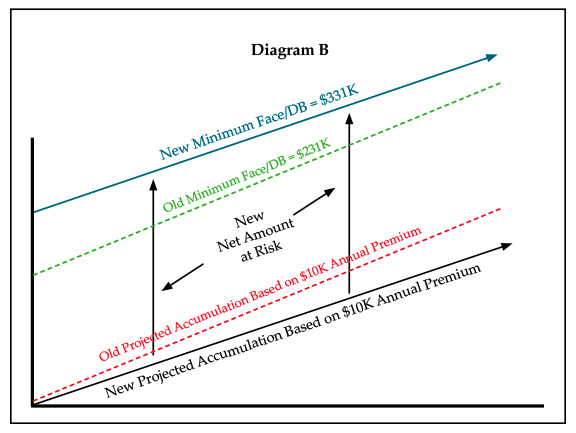

Now, because IUL is a “flexible premium” product, we can choose to have the face amount at $331k instead of the $221k that was the minimum death benefit. Afterall, our client needs that additional $100,000 of coverage for 20 years. Without digging into the numbers year by year, and instead keeping this conceptual, let’s overlay the “new” scenario of Brian funding at the same $10k per year but now moving this IUL’s death benefit up to $331,000. See Diagram B.

As you can see in Diagram B, the old scenario is represented by the dashed lines. I also included the new $331k face amount (in blue) and also the new projected cash accumulation value (in black). Notice how the cash accumulation is not as steep as the previous dashed accumulation (in red). That is because of the additional expense drag that is incorporated into Diagram B which is composed of:

- Higher cost of insurance charges which is based on the higher “Net Amount at Risk”

- Higher per thousand charges which is based on the higher face amount

If you have read any of my past IUL analysis, you would recognize the two expenses above as being two of “The Big Three” of expenses that I discuss frequently. The third being Premium Loads, which is a function of the premium going into the policy. Note: I have since changed it to “The Big Four” now that many companies have asset-based charges.

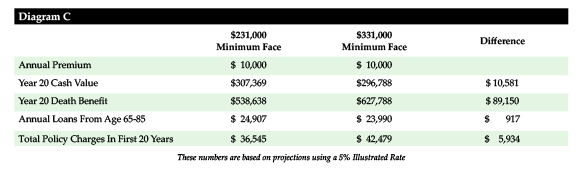

In the assumptions in Diagram C I used a very reasonable five percent illustrated rate, instead of the 6.9 percent that I could have used as the max. The only thing that illustrating a higher rate would do is to prove my point even further.

As you can see, by having a death benefit of $100k beyond the “Minimum Non-MEC” that the IRS would allow, you are watering down the cash value performance of the policy because of the higher expenses. By adding the $100k death benefit, one is watering down the Year 20 Cash Value by $10,581 and the annual loans by almost $1,000. Most importantly, how much in additional charges would Brian have in the $331k policy versus the $221k policy? $5,934 over the 20 years–or an average of $297 per year.

So, What Is My Suggestion?

Am I suggesting we leave Brian without the $100,000 additional death benefit? Of course not. To me it is a question of, “What would be the cost of $100,000 of coverage for 20 years from a source outside of this IUL policy?” Then we would compare that cost to the $5,934 that it would cost if we used the IUL for that additional $100k coverage.

Utilizing the same health class as the above IUL, the best 20-year term price for Brian on $100,000 in coverage would only be $175 per year, cheaper than the $297 per year embedded in the IUL pricing. Furthermore, the 20-year term premium/expenses/charges are 100 percent guaranteed whereas the IUL can adjust. Now, needs can change, so I would suggest a term policy with great conversion privileges, as this particular term has.

What I am suggesting is that with cash value policies in general—not just IUL—that many times these policies are “specialists” in either cash accumulation or death benefit. It is rare if not nonexistent where there is a product at the top of the industry for death benefit leverage and also cash value potential.

What I ultimately suggested to my agent was to offer both products—the max funded $231k face IUL and also the term policy. He sold them both!

Note: I also looked at the Term Blending Rider on the IUL which was fairly expensive. Term blending riders are great for when the client wants to fund an IUL but has varying premiums that he/she will put in over time. Term blending is a great “place holder” for death benefit that can be converted to the permanent base coverage later on. Inquire if you are interested in learning more about term blending.

In Summation

Now, by Brian paying the premium of $10,000 per year into the IUL and $175 per year into the term, he is paying $10,175 in total premiums. I could show you the math of including all of that into the IUL, but the end conclusion will not change by adding $175 per year to the premium.

Much of what I wrote here is fairly brief because I wanted to keep this simple, accurate and conceptual. For instance, I could have discussed “term blending riders” that many IULs offer, but that would not have changed the conclusion. Furthermore, I did not incorporate time value of money to discount back the COI charges into today’s dollars, etc. I have done those mental gymnastics outside of this paper and I have always come to the same conclusion–that it is always best to try to “max fund” accumulation IUL whenever you use it, and buy the death benefit leverage from a death benefit focused product separately. In other words, my belief is, specialization is important!

It is best to use a Ferrari for racing and an RV for camping instead of trying to use one of those vehicles for both activities.