What Instant Issue Is, Isn’t, And Why Your Clients Want It Now

From instant meals to instant messages; from on-demand food delivery to on-demand movie streaming, it’s clear: We live in a world where nearly everything we could want appears at the touch of our fingertips. This applies not just to our creature comforts, but to the way we do business as well.

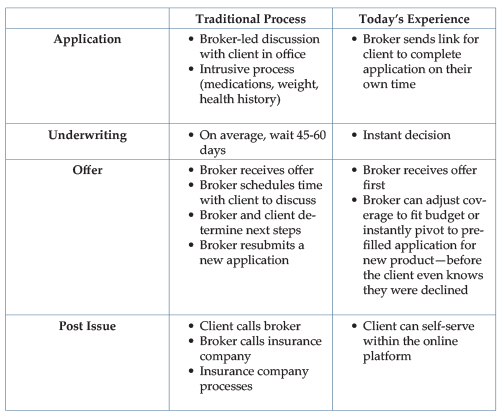

Today’s consumers have become accustomed to, and fully expect, solutions that offer simplicity, speed and seamlessness. There was a time in the not-too-distant past where when we wanted or needed something, we went to a store or consulted with someone at an office. Then came online shopping, where the convenience of home delivery changed everything, and Zoom opened up a whole new virtual experience for service providers such as physicians, therapists, financial advisors, and more. For brokers, working with instant decision/instant issue carriers is somewhat like placing your grocery order and choosing whether you want it delivered to your home or, if it’s more convenient for you, to choose curbside pick-up. Your customer is still ordering the same items, but how they obtain them is the variable factor.

It’s no wonder, then, that almost half of all U.S. adults say they are more willing to purchase a life insurance policy via simplified underwriting than traditional underwriting due to the convenience, no need for medical exams, and transparency when it comes to premiums. In recent years, options such as instant issue life insurance policies have grown in popularity as more digital-first providers emerge to meet consumers where they are to help bridge the coverage gap for the 48 percent of Americans who do not yet own life insurance.

Whether an applicant is approved or not, instant issue policies may sound like a great fit for today’s digital natives—“instant” is the name of the game!—but what are they, really? Read on to bolster your knowledge of what instant issue life insurance is (and, perhaps more importantly, what it’s not).

Quiz: How Much Do You Actually Know About Instant Issue Life Insurance?

But first, a quiz. To test your instant issue savvy, review these statements and determine whether they are true or false.

- All instant issue policies are the same.

- Anyone can apply for and receive instant issue life insurance.

- Instant issue life insurance offers the same level of coverage as traditional policies.

- Instant issue policies are always more expensive.

- No-exam life insurance is just “instant issue” by another name.

If you answered “false” to all of the above, you are correct! When it comes to instant issue policies, like most things in our industry, there is a bit more nuance behind the magic.

The Ins and Outs of Instant Issue

In a nutshell, instant issue life insurance refers to a policy that expedites underwriting, providing rapid approval and coverage without the need for extensive medical exams. It’s designed for quick and straightforward applications, making it a convenient option for clients seeking smaller coverage amounts promptly. While policies and terms vary by carrier, most instant issue options have a few key features in common:

- Client Convenience: Instant issue insurance caters to clients who prioritize a rapid application experience.

- No Medical Exams: Instant issue policies typically do not require medical examinations, reducing potential barriers to purchasing.

- Simplified Applications and Streamlined Underwriting: Applicants complete health questionnaires to expedite underwriting and approval time compared to traditional policies.

- Immediate Coverage with Immediate Effect: Clients gain access to coverage almost instantly upon approval.

Instant issue policies may be worth exploring for your clients—including the 47 percent of U.S. adults who say they would consider a simplified underwriting process simply for the benefit of avoiding face-to-face interactions to make the policy purchase. As the life insurance industry continues to modernize, there is great opportunity for brokers to leverage digital and tech solutions to not only delight clients, but also to reallocate time toward value-added activities such as prospecting, relationship management and more. As always, it’s important to remember that these tools are not meant to (and could never truly) replace the integral role of brokers, but rather to help boost productivity and cut through the red tape of the traditional purchasing process.

Reference:

- The Life Insurance Consumer Report Study 2023, Insurist.

- 2023 Insurance Barometer Study, LIMRA and Life Happens.

- The Life Insurance Consumer Report Study 2023, Insurist.