If you get shivers down your spine in excitement like I do when you think of things like CVAT, GPT, Modified Endowment Contracts, and Section 7702, then I hope you are sitting down. If you are an insurance agent that sells (or wants to sell) accumulation focused policies like IUL and whole life (short pay or PUAs), then this article is for you.

The roughly 5,500 page, $2.3 trillion “Consolidated Appropriations Act of 2021” that was signed into law on December 27 had much more in it than $600 stimulus checks to say the least. From $600 stimulus checks for Americans to $15 million for “Democracy Programs” in Pakistan, the law has a lot of stuff in it that many of us will never know.

One area that you would be interested in is revisions to Section 7702 of the Internal Revenue Code. If you have been in the insurance business for some time, you are familiar with what this section does. Quite simply, Section 7702 was established in 1985 and defines the wonderful tax advantages of life insurance and, just as importantly, the rules that life insurance policies must follow to retain those tax benefits. These rules largely consist of limitations on how much money one could put into a life insurance policy relative to the death benefit. (By the way, anytime I have been told by the IRS that I cannot do something or can only do so much of something, it is probably a great thing to do!)

To forego the suspense, I will do this article a bit backwards and give you the punchline before going into the details. In short, effective January 1, 2021, policies can be funded at higher levels than before, depending on the client’s age. In some cases we are talking about seven-pay levels that are over two times higher, per dollar of death benefit, than before. So when you think of maximizing your IUL for cash accumulation and/or putting “paid up additions” on the whole life policy, this is great! However, don’t get too excited just yet because the carrier implementation process needs to happen.

Let us get into the details.

Back in the 1980s, right after the first universal life insurance policy was created (1979) by EF Hutton, one could cram a lot of cash into a life insurance policy. So much that it became obvious to Congress that the consumers were not using it as life insurance, but rather as an “investment.” Consider an exaggerated scenario of someone putting a $100,000 premium into a life insurance policy with a $100,000 death benefit. Clearly that hypothetical consumer is not concerned about the death benefit leverage, they are concerned with accumulating as much cash as possible while ultimately being able to take out that cash—plus interest—that is 100 percent tax free. Furthermore, that person would not be paying “cost of insurance charges” that should be the cover charge to enter the nightclub (remember those things?) of tax-free life insurance benefits.

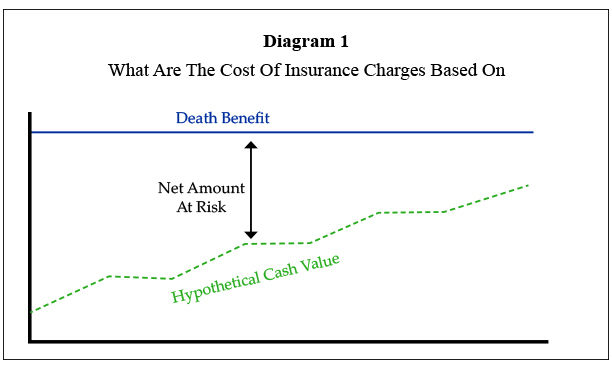

What do I mean in my last sentence by “not paying COI charges”? Well, if there is no “Net Amount at Risk” in a life policy, then there are no COI charges. Check out my training diagram (Diagram 1) that demonstrates what COI Charges are based on. This diagram is from www.retirement-academy.com.

What are the “cost of insurance charges” based on? They are based on not the death benefit, but the “Net Amount at Risk,” contrary to what many smart insurance folks may know.

In Diagram 1, think of how efficient of a tax-free “investment” a life insurance policy would be if you could get the Net Amount at Risk down to $0! This would be achieved by cramming a single premium in that equals the death benefit. Clearly, that scenario—although a bit of an exaggeration—was too good to last.

So, back in 1984, our friends in Congress said, “We cannot allow consumers to continue to have the wonderful life insurance tax benefits without paying the cover-charge of COI charges.” Thus, through DEFRA (Deficit Reduction Act of 1984) you had the establishment of two “tests” that defined life insurance. These tests were titled, the Cash Value Accumulation Test and Guideline Premium Test. This created Section 7702 of the Internal Revenue Code. DEFRA was the law and Section 7702 was what governed the law. Remember, Congress makes laws (DEFRA), and the IRS enforces the laws (The Internal Revenue Code Section 7702).

Even after DEFRA and the creation of these two “tests” that limited the amount of premium and cash value in the policy relative to the death benefit, consumers were still able to have “short pay” scenarios that felt too much like “investments” to Congress. So, in 1988 we saw a new section added to the internal revenue code via a new law signed by President Reagan. The new law was the “Technical and Miscellaneous Revenue Act of 1988 (TAMRA).” This new code section was Section 7702A. This created the “7-Pay Test.” If you fail the 7-Pay Test, the policy is a “Modified Endowment Contract,” which effectively takes life insurance taxation and turns it into annuity taxation.

The 7-Pay Test was a new and separate test that was layered on to the policies in addition to the CVAT Test and GPT Test. Many folks lump all these tests together as being “Modified Endowment Contract Testing.” That is false. GPT/CVAT and 7-Pay/MEC are separate sets of tests. GPT and CVAT define whether the policy is “life insurance” and the 7-Pay Test determines if the policy is a MEC.

What were the repercussions of a policy becoming a MEC? In all my training, I simplify it down to:

“Although the Modified Endowment Contract is still technically a life insurance policy, think of the taxation as almost the same as an annuity except the death benefit which is still tax-free. Last-In First-Out, pre-59.5 penalties, etc.”

Now, to discuss what changed January 1, 2021, let’s discuss the “MEC Calculation” that congress and their actuaries created in 1988.

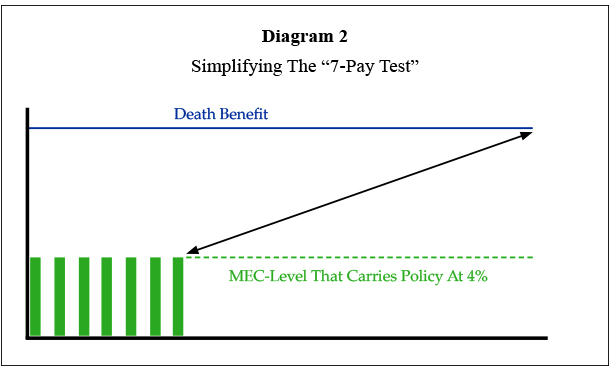

Diagram 2 is very simplified, but it is a good visualization of the MEC calculation. Basically, Congress said that for a certain life insurance death benefit to carry to maturity, what is the level of premiums paid over seven years that would accomplish that? The resulting level of premium that the calculation generates will be the “MEC Limit” for that policy. And, if you put more into the policy than this limit, just know that you have a MEC and are taxed as such.

Now, there are some assumptions in Congress’ calculation, right? The big assumption is the interest rate assumption that the premiums get credited on. This “Insurance Interest Rate” they assumed in 1988 and still did until 2021, was four percent. By the way, ever wonder why many whole life policies have guaranteed rates of four percent? To match the MEC calculation.

Here is what happened, effective January 1, 2021. After 35 years of dropping interest rates, Congress has finally adjusted the “Insurance Interest Rate” down to two percent for 2021 and a floating rate based on benchmarks for years thereafter. This was long overdue.

What is the impact of this lower rate? The MEC limit is increased by anywhere from 10 percent for older insureds to around 200 percent for younger insureds! In other words, if a policy would have had a MEC limit before of $10,000 per year, it would not be rare for us to now see that increase to $20,000, depending on the age of the client. Of course, this would be on new policies. I do however have questions about how carriers will treat “material changes” on already existing policies, but I digress.

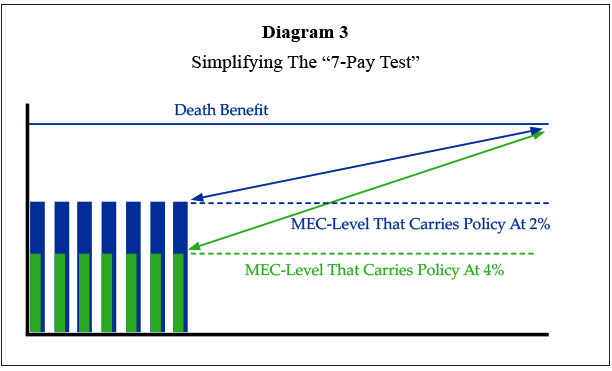

Check out Diagram 3 on why this new “Insurance Interest Rate” affects the MEC limit as we discussed.

The way that time value of money works is, if you are getting a lower interest rate (two percent instead of four percent) on your premiums, then there is more money needed to guarantee a later value. Remember, that “later value” that congress uses is the death benefit at “maturity.”

In Diagram 3, we overlaid the new MEC limit (blue) with the old (green). These bars are not meant to be proportionate to the changes. Rather, just a simplified visual. Clearly, at a two percent rate, there would be more premium required than the four percent rate. Thus, you have higher MEC limits now versus prior to 2021. Point of clarification: I am not saying that life insurance policies changed where you must put more money in because of the lower rate the IRS uses. I am saying that you will generally have the option to put in more premium, once the carriers enact these changes.

What is the benefit to the client of more premium going in? As discussed, compressed “Net Amount at Risk,” which means less COI charges. This was illustrated with my first diagram.

Note that although we are talking about one test (the MEC Test), the CVAT Corridor calculation and the GPT calculation are adjusting as well. I will not inflict anymore mental gymnastics by going into details on those, but they are affected in a similar fashion as the MEC calculation.

A Few Notable Impacts:

- Consumers will be able to put more money in per dollar of death benefit. Of course, there will be a transition period with carriers.

- Products in the IUL space and the whole life space will be adjusted by the carriers. I would bet that the whole life products see more drastic changes than IUL. This is not a bad thing though.

- Whole life policy reserving will become easier since the carriers will have more flexibility on the guaranteed interest rates they offer to the consumers. You may see required premiums increase and thus lower guaranteed interest rates on policies.

- Whole life dividends will become even more important than they currently are. At least relative to the “Guaranteed Columns” in the illustrations. I believe the gap between the “guaranteed columns” and the “non-guaranteed columns” will widen.

- I think there can be a negative to insurance carrier profitability as well. Carriers are getting very little profit today via “investment spreads” in this low interest rate environment. Much of their profit is coming from the COI charges in the policies. So, now that those COI charges and the “Net Amount at Risk” can compress further, it might be interesting to see what the carriers do.

- The big one that I have gotten a lot of questions on: Commissions will likely be negatively impacted. Why? Think of it this way: If a client is putting into a policy, say $10,000 per year, the minimum death benefit may be, say, 50 percent of what it would have been before. What does that lower death benefit do to your target commission? It reduces it. Or, if you are a whole life producer, what does that generally do to the proportion of “Paid Up Additions” relative to the base policy? It increases it. And you generally do not get paid the same on PUAs as you do the base policy.

- What I just discussed is on new business only. However, in the law from the 80s there is a new 7-Pay Test that happens if there is a “material change” in the policy. What does that mean for material changes going forward on already existing policies? I will let the carrier attorneys handle that one.

If you would like to see the five pages from the Consolidated Appropriations Act of 2021, you can email me at cgipple@cgfinancialgroupllc.com.