(Part One Of Two)

If You Aim Small, You Miss Small.

A hobby I inherited from my father is shooting precision rifles and handguns. It would be safe to say it’s due to my father that I often find myself looking deeper into different rifles and handguns via the likes of The Fire Arm Blog and the likes. He deeply rooted the passion in me long before I realized. Decades ago, when my brother and I were learning to shoot, my dad would tell us, “If you aim small, you will miss small. Don’t aim at the bullseye, rather zoom in and aim at the little tiny area in the center of the bullseye. If you miss that little tiny area within the bullseye, then you will probably still be within the bullseye.” This wisdom was not only great shooting advice, but it has also proven to be great career advice.

How is this great career advice? Some of the best salespeople I have ever worked with, worked for, or lead, tend to “zoom in” and understand the details around the way things work versus just being “generalists.” These salespeople have a never-ending curiosity. These salespeople are students of the business. These salespeople have a thirst for understanding the technicalities that may make others balk. The best are not above learning the details.

When one has a very “general” view of something it leaves a lot of room for inaccuracies and misperceptions. Thus, in today’s complicated world of finance, being a subject matter expert will warrant a premium over the generalists. Plus, the world is full of generalists so why not stand out?

You have likely heard the cliché, To be clear, I am not suggesting that in order to separate yourself you need to explain “how the watch is built.” Rather, that you at least understand the details so you can explain the general idea in a succinct fashion. As Albert Einstein said, “If you can’t explain it simply, you don’t understand it well enough.” This speaks to my emphasis on simplification, behavioral finance, and right brained storytelling which I have written about several times. The best sales people I have worked with don’t communicate how the watch is built, yet they do understand how it is built-which in turn helps them communicate the message. This series of two columns (March and April) is very much in that vein.

The Proliferation of IUL and Misperceptions

Over the last 10 years the sales of IUL have gone from $100 – $150 million per quarter to around $500 million per quarter. IUL is now a $2 billion business and represents over 20 percent of individual life insurance sales. With the rapid rise of IUL since its birth in 1997 there have been a lot of new entrants (carriers, distributors and agents) into the market. A lack of understanding and host of misperceptions come with new adoption of any proliferating product that can be considered complex. And heaven knows, IUL has been no exception. However, if you-the agent, distributor, or wholesaler-can “zoom in” and understand how these products are created, then you will better know how to explain and make sense of the areas of confusion and correct misperceptions. A few examples of confusion and misperceptions around these products are:

- “How can IUL give up to X percent if the market goes up, but if the market goes down you don’t get negatives? Seems too good to be true.”

- “If the client is invested in the S&P 500, why are there no negative returns when the market drops?” (Note: The client is not “invested” in the S&P 500!)

- “How are caps on IUL so much higher than indexed annuities? Are the IUL companies playing games with caps?”

- “Why have caps decreased recently with the market at all-time highs?”

The above are just a few examples of frequent questions I get from agents and distributors on IUL and indexed annuities. By the end of this series you will be able to answer them all, and then some.

(Note: Even though this column series is predominately about IUL, by reading this you will also understand how indexed annuities are created and priced. Indexing is indexing.)

Current Assumption UL

Chart 1 shows a hypothetical scenario using a hypothetical product:

To start, let’s create a basis for comparison using traditional fixed UL, also known as current assumption UL. The major difference between current assumption universal life insurance and IUL is what the carrier does with the interest that is spun off from the general account. Below you will see that with fixed UL the carrier quite simply takes the client’s net premium-$10,000 in this example-and invests that premium into the carrier’s “general account.” The general account in our example below is yielding 4.5 percent. This yield of 4.5 percent is generated from the assets in the general account that is largely high-grade corporate bonds. (More on general account composition in April’s column.)

In an effort to keep this as simple as possible, I did not take into consideration the carrier taking a “spread” off the 4.5 percent. In reality, the carrier might take, say, 50 basis points per year for their profit and pass through the remaining four percent to the consumer. Also remember that carriers have other sources of revenue within universal life insurance that do not exist with annuities. These additional revenue sources make life insurance carriers less reliant on the “yield spread” than annuity companies. I call these other sources of revenue the “Big Three” of UL/IUL expenses.

The Big Three of UL/IUL Expenses

Following are the most common expenses within UL/IUL. Depending on the product there can be others, like asset charges and policy charges, but the below are the most prominent:

- Premium Loads: This is an expense deducted off the top of each premium payment going into the policy. Common premium loads are five to 10 percent of premium. The difference between the gross premium and net premium is the deduction of the premium load. To generalize, these are largely used to offset the carriers’ acquisition charges.

- Per Thousand/Per Unit Charges: These charges are a factor based off the size of the death benefit/face amount and are usually deducted from the cash value monthly. These charges are largely used to offset administrative expenses the company incurs. For instance, the people in the home office processing the premium payments, loans, etc., cost money!

- Cost of Insurance (COI) Charges: These are the mortality charges that are based on the difference between the policy’s cash value and death benefit. This difference is called the “net amount at risk.” This expense is also usually deducted from the cash value monthly. The great thing about the COI charges is that they can be tweaked and minimized somewhat by optimizing the death benefit structure. For instance, an Option 2 death benefit switching to Option 1 death benefit generally minimizes the net amount at risk, which in turn minimizes the COI charges.

For the life insurance novice the above charges may seem exorbitant and complex, which may be a turn off with UL/IUL. However, it is important to remember that whether it is UL, IUL, or whole life, these expenses exist for the insurance carrier and it is just a matter of what calculation the carrier uses to pass some of those expenses on to the consumer. For example, with participating whole life insurance the carrier generally charges the client a much larger premium per dollar of death benefit relative to UL/IUL. However, that “overcharging” is then refunded back to the client at the end of the year in the form of a dividend. The actual dividend amount is determined after the carrier does the calculation of what their true experience was with investment earnings, expense management, and mortality. In short, both whole life and UL/IUL are great products-just using different methods.

1995: Necessity is the Mother of Invention

The annuity business is where indexed products were conceived. In 1995 there was a state of confusion for investors regarding where they could put their money that would give them a reasonable, safe return. This is because bank CD rates had been drastically falling for almost a decade and a half, the stock market finished 1994 on a down note, and last and most interesting, 1994 was the year of what Fortune Magazine called “the great bond massacre.” This was the year where bonds and bond funds were decimated. Effectively, in 1995 there was the perception that there was nowhere to go where a consumer could get a decent “safe” return any longer. Interest rates were poor, the stock market disappointed the year before, and the bond market was devastated.

Because necessity is the mother of invention, a company called Keyport created the first indexed annuity, “The Key Index” in 1995. Two years later the life industry followed with the first IUL.

Indexed Products and

I recently purchased a Nintendo Classic to demonstrate to my 11-year-old and eight-year-old what fun it was to grow up in the 80’s. This is a system that pays homage to the game system that many of us grew up with. It is preloaded with thirty games from the 1980s and uses the same wired controllers and horrible graphics. Nintendo did a great job keeping that retro feel that I remember so well. My kids were not near as impressed as I was however.

One of the games that I always played that is also loaded on this system is called “Excitebike.” This is a dirt bike racing game where you jump terraces and maneuver from lane to lane in order to avoid the mudholes that slow you down. If you hit a mudhole and your competitors don’t, they will blow by you. There are also sparsely placed turbo strips that, if you react fast enough to swerve into that lane and cross over those strips, you get a turbo boost and blow by your competitors. You must be careful though, because once you hit those turbo strips it becomes harder to swerve to avoid the mudholes because you are moving fast.

The Excitebike experience is analogous to UL versus IUL. If a consumer chooses to just chug along at a constant speed and not hit any “turbo strips,” then the previously mentioned UL is probably for them. They will never hit the “turbo strip” that can give them say 10 percent, but they will also never hit the “mudhole” and get less than the three, four or 4.5 percent interest credit that the current assumption UL guarantees. (Note: With current assumption UL the 4.5 percent can usually be increased or decreased annually, similar to the annual declared rate fixed annuities.)

As mentioned, many consumers over the last two decades have opted for the tradeoff that IUL provides. Many have opted for this ability to hit the turbo strip that gives the potential for an interest credit beyond three, four or 4.5 percent while at the same time the potential of hitting a mudhole. Of course, the “mudhole” is the zero percent interest (minus expenses) if the market is flat or down. However, zero percent beats a minus-40 percent should we hit another market crisis. Without going into past performance, this tradeoff has proven to work out quite well for consumers since IUL’s inception in 1997.

What is the turbo strip? The turbo strip is the call option strategy that allows the policies to perform better should the market perform. Allow me to explain.

IUL: Trading a Fixed Rate for More Potential Upside

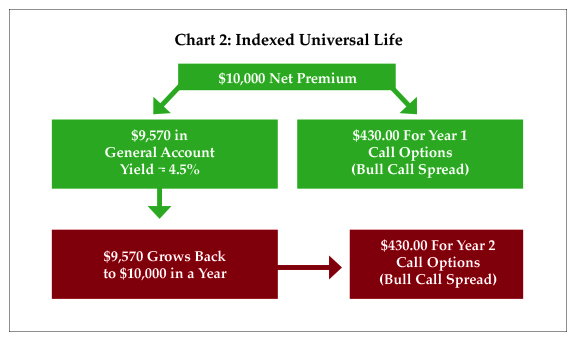

Chart 2 is a hypothetical scenario using a hypothetical product.

Again, with UL the general account yield is simply passed through to the client, with maybe a spread deducted as well as the “Big Three” of expenses. With IUL our general account yield is being steered in another direction-to purchase a call option strategy.

Remember our general account yield was 4.5 percent? Here is the calculation that is generally used with IUL. If a client’s net premium (after premium loads) is $10,000, then what dollar amount must go into the general account so that after it earns 4.5 percent for that year it will equal the $10,000 at the end of year one? We want the $10,000 to be there by the end of year one because that is the safety that these non- securities products promise.

As you can see in chart 2, the dollar amount needed is $9,570 ($10,000/1.045) that will grow back to $10,000 by the end of year one. What does the company then do with the remaining $430 ($10,000 – $9,570) in our example? This is where the company “redirects” that $430 to an investment bank to purchase the “turbo strip.” The turbo strip is the call option strategy that is usually referred to as a “bull call spread.” (More on the “bull call spread” in April.)

So, a current assumption UL effectively invests all the net premium into the general account which only generates a fixed interest rate. Conversely, the IUL example shows the $430 being chipped off to purchase a “bull call spread” to give the IUL a link to the market index. With IUL the $9,570 grows back to $10,000 every year which provides the baseline guarantee while the $430 provides the potential upside (the turbo strip) that can give the client additional interest on top of the guarantee. Each and every year the process is repeated as you can see with the red box that represent year two.

Imagine, in the example, that the general account yield was seven percent, as it was once upon a time many years ago. That would only require $9,346 ($10,000/1.07) to go into the general account to regenerate the $10,000 by the end of the year. This would leave a whopping $654 for the options budget. More options budget equals higher caps, as we will discuss. The point is, the decreasing interest rate environment we have been in for 37 years is why caps have decreased. Because less of the client’s net premium is left over to buy the “turbo strip.”

The tradeoff versus current assumption UL is the opportunity cost. That is, the $430 call option budget could prove to be useless over a year’s period if the market does not perform. At that point in time the options would expire worthless. Conversely, with a current assumption UL, one is at least guaranteed some level of interest-4.5 percent for example. Remember my “mudhole” analogy with Excitebike? The mudhole is hit with IUL when the 4.3 percent expires worthless because the market did not increase.

Part Two (April’s column) will expand on the bull call spread-the buying and selling of call options. We will also discuss the composition of insurance companies’ general accounts and the product impacts of the persistent low interest rates.