Combination life insurance (life insurance with long term care insurance features) continues to grow and evolve.

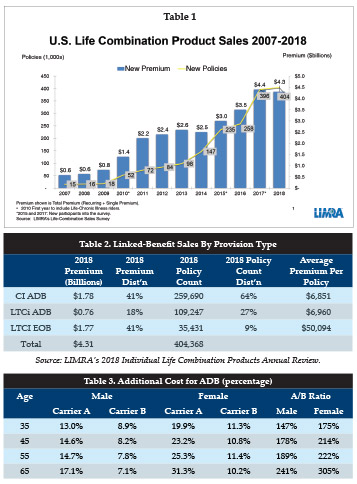

Table 1 (from LIMRA) shows the number of combination life insurance policies and related new premium from 2007-2018. It excludes work-site sales and combination annuities. Two percent more combination life insurance policies were sold in 2018 than in 2017. Premium dropped two percent, but that’s misleading as will be discussed.

Table 2 shows the distribution of those combination life policies in 2018. As will be discussed later, “CI” means “chronic illness” as opposed to “LTCI” which means “long term care insurance” and “ADB” means “accelerated death benefit” only as opposed to “EOB” which means that an “extension of benefit” is available as well as an ADB.

There are many ways the combination market can be divided, one of the most significant ones being in terms of coverage provided (risk borne by insurers). As Table 2 shows, only nine percent of 2018 combination policies were sold on products that permitted more than the death benefit to be used, if a need for long term care (LTC) occurs, by offering an EOB feature. More than 90 percent of the policies were sold on products which offered only an accelerated death benefit (ADB) for LTC.

Product differences explain some of the price variations between insurers shown below. Insurers may differ in their assumptions of LTC incidence and in their assumptions regarding how often insureds choose to access their ADB when they do need LTC. Different lapse assumptions or ADB election assumptions based on market can have a significant impact. Also, insurers may differ as to whether they assume that an LTC feature improves product persistency and how such persistency improvement is reflected in pricing. ADBs and EOBs can generate different capital requirements for various insurers based on their mix of business, and insurers vary in how they allocate expenses to “riders” (for example, optional features that add additional cost). Underwriting requirements or classification can make a difference (there are definitely distinctions of that type below), because a healthier class should have a lower mortality premium but may have a higher LTCI premium because more survive to ages of LTC incidence. Differences in pricing techniques (particularly for newer features) might cause inadvertent differences.

Accelerated Death Benefit (ADB)

ADBs are an inexpensive way for insurers to help consumers cover LTC costs, by giving them the flexibility to use their ADB, if they wish, when LTC is needed. The insurer does not pay out more money; instead the insurer simply pays it out earlier (a loss of investment income). If a lot of the death benefit is paid out as an ADB benefit, it seems likely that the insured would have died fairly soon thereafter; a short period of foregone interest involves low cost. If little was advanced, the foregone interest on that advanced money is low. Furthermore, the cost is low to the degree that people save their death benefit for their beneficiaries, using the ADB as a last resort.

Comparing only two carriers, I found significant difference in the cost of adding an ADB provision as shown in Table 3.

ADB costs more (in dollars) for females than for males because females are more likely to need LTC (hence to use ADB), are likely to need LTC longer (hence are likely to use more of their ADB) and are more likely to continue to live after the full ADB has been advanced (which means more loss of interest from advancing the death benefit). The gender difference in percentage add-ons for ADB is even larger, because the female’s life premiums (denominator) are lower.

It is interesting that the percentage add-ons for ADB differ so much by insurer. One insurer’s percentage add-on increases as age increases, whereas the other insurer’s add-on generally decreases as age increases. At the end of the previous section, I explained some of the factors that can impact pricing.

Extension of Benefits (EOB)

Extension of benefits (EOB) provisions continue to pay benefits after the death benefit has been used up (and often provide a residual death benefit). Thus, the insurer takes a much more meaningful LTC risk, rather than simply lost investment income.

From a consumer’s perspective, a life insurance policy with an extension of benefits provision is a better way to “self-insure.” The consumer “self-insures” the first two or three years of LTC with their beneficiary’s death benefit, as that death benefit is used to pay for LTC. After the death benefit is used up, the consumer has an inexpensive partial stop-loss or catastrophe type of coverage because the self-insurance portion represents a two-year or three-year elimination period before true LTCI risk transfer occurs.

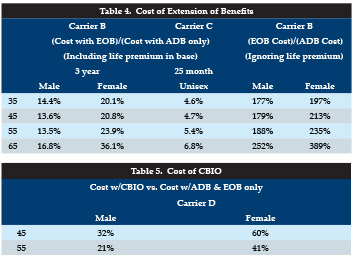

Table 4 (see page 22) shows that EOB provisions add more cost than ADB provisions, even though they are much less likely to be used, particularly by males. Of course, that’s because the EOB is a marginal additional cost for the insurer, rather than only paying cost earlier.

The four leftmost columns in Table 4 show the percentage additional cost of adding EOB to a life insurance policy that already includes ADB. The Carrier C product is a work-site product with unisex pricing. Because it has a shorter extension of benefit period (25 months compared to 3 years) and because the extension starts a bit later (after 25 months compared to after 24 months), I would expect the EOB cost add-on to be lower for Carrier C than for Carrier B. Some possible explanations for Table 4 differences were mentioned earlier.

The rightmost two columns are different, showing the ratio of the extra premium to add EOB to a policy to the extra premium to add ADB to a policy. Not surprisingly, the additional cost of the EOB compared to the ADB is smaller for men than for women, because few men outlive the ADB benefit. The ratio increases with issue age because more older buyers will have coverage in their 80s.

A longer EOB would cost more; a shorter EOB would cost less.

Insurance products which offer only an ADB typically have no discounts for married people, whereas products with EOBs often discount prices for married people (for example, 10 percent). Stand-alone LTCI policies typically have the largest discounts for couples but require that both buy.

Compound Benefit Increases (CBIO)

Compound benefit increase features (CBIO; the maximum monthly benefit and potential lifetime benefit compound) add more cost than either ADB or EOB. When ADB is exercised, most (perhaps all) insurers subtract only the base benefit (not the portion attributable to compounding) from the death benefit.*

Whereas the ADB does not create additional benefits (solely paying an ultimate benefit earlier) and the EOB creates additional benefits but not until after the ADB is used up, the CBIO feature creates additional marginal benefits as soon as the insured goes on claim. Therefore, it can cost many multiples of the cost of ADB, depending on the compounding percentage and on the benefit period, etc.

Table 5 shows the cost of adding CBIO to a five-year benefit period linked-benefit product.

The percentages in Table 5 are applied to a bigger base than the percentages in Table 4 as the Table 5 denominators include the cost of the EOB feature.

*Insurers differ in how they handle benefits that are less than the maximum. Consider a base benefit of $3000/month which has grown to $6000/month. If a policyholder uses only $3000 in a month, one insurer may deduct that full $3000 payment from the death benefit, while another might consider the $3000 payment to be half base and half compounding thereby reducing the death benefit by only $1500.

Single Premium vs. Recurring Premium

Tables 1 and 2 combine single premium sales and recurring premium sales, thereby obscuring some significant differences. LIMRA shared some data with me, permitting me to determine the distributions mentioned below.

ADB sales are most commonly made to satisfy a life insurance need. The ADB feature may be automatically included because of the insurer’s product design or may be added at the suggestion of the financial advisor. Fewer than two percent of ADB policies are paid for with a single premium.

On the other hand, when EOB policies were first created, they 100 percent were sold with single premiums. The concept was to move “lazy assets” (low-yielding assets) to an EOB policy to leverage the investment for LTCI purposes. In these sales, the primary motivation was generally LTCI, the life insurance component being attractive to avoid “use it or lose it.”

However, as inforce stand-alone LTCI policies started having large price increases, and large price increases applied to new stand-alone LTCI sales also, the EOB carriers recognized an opportunity to grow by making their product available on a recurring premium basis. Originally the expansion was limited to 10 premium years at most, but in 2018 we continue to see more lifetime-pay products becoming available. In 2018, 57 percent of the EOB sales were single premiums compared to fewer than two percent of the ADB sales.

All other things being equal, I would expect EOB policies to have higher premiums because they add on an additional LTCI benefit. However, in 2018 and 2017, ADB average single premiums were roughly 50 percent larger than EOB single premiums. Perhaps the ADB single premium cases had larger death benefits, were sold at higher ages, or were more often rated due to health conditions.

On the other hand, the average recurring premium on EOB policies was more than twice the average recurring premium on ADB policies. Besides the additional cost of EOB (and sometimes CBIO), this difference might reflect that a higher percentage of ADB policies have premiums scheduled to be paid a very long time as opposed to 10 years or less.

Single premiums accounted for 61 percent of LIMRA’s reported new 2017 premium, but only 58 percent of new 2018 premium. Correspondingly, the market share of recurring premium increased. Thus the “drop” in 2018 premium seems to be balanced by an increase in future premiums. A decrease in average issue age, which seems likely with the shift toward recurring premiums, could increase the present value of future premiums.

Section 7702(b) vs. Section 101(g)

Another way that combination policies can be distinguished from one another is by which provision of the legal code applies to them. Section 7702(b) policies have LTCI benefits that can legally be called “long term care insurance” and must satisfy all the LTCI legal requirements. Most ADB policies have chronic illness provisions, which comply with Section 101(g) which permits incidental coverages to be added to life insurance policies if they do not exceed 10 percent of the value of policy benefits.

Financial advisors (FAs) are not allowed to refer to Section 101(g) policies as “long term care insurance.” I believe that puts FAs in a very tough spot. Section 101(g) provisions can be more favorable than Section 7702(b) provisions because Section 101(g) provisions are more likely to pay the full LTC benefit regardless of the cost incurred, rather than limiting the benefit to reimburse the amount of LTC cost incurred. They may satisfy requirements for Section 7702(b) policies and any such requirements they don’t satisfy may be less important to the consumer than the advantages Section 101(g) provisions may have. Rather than forbidding them to be called “LTCI,” it might be better to require that the insurer disclose any LTCI requirements which they violate.

The Deficit Reduction Act (DRA, 2006) required certification (training) to sell LTCI policies which qualified for the State LTC Partnership programs. The NAIC’s recommended wording (to implement DRA) required certification for all LTCI policies whether the policies qualify for Partnership programs or not. I prefer the NAIC wording so that all (at least all stand-alone) LTCI consumers can have access to Partnership policies.

Some states adopted the NAIC wording, while others adopted wording straight from the DRA. In states which have adopted either the DRA wording or the NAIC wording, most (if not all) insurers selling stand-alone LTCI have uniformly required certification regardless of whether a policy is Partnership-qualified or not. Insurers selling combination policies (including linked-benefit policies), on the other hand, have generally not required certification in states with DRA wording.

Evolution

Sales are shifting from stand-alone long term care insurance toward combination products, but not as much as many industry watchers think. In 2018, 56,288 stand-alone LTCI policies were sold1 vs. 35,431 EOB linked-benefit policies. The huge “wave” of combination policies consists of ADB-only policies.

Although approximately 60 percent more stand-alone LTCI policies were sold than EOB policies, the EOB market produced ten times as much new premium as the stand-alone LTCI market ($1.78 billion vs. only $0.172 billion1). To judge relative stand-alone and combination LTC sales based on premium is misleading because:

- The inclusion of life insurance generates a higher premium, not attributable to LTC risk.

- The prevalence of single-premium and limited-pay (e.g., 10-year-pay) sales in the EOB market tilts the comparison. One dollar of recurring premium sales is worth a lot more than one dollar of single premium sales.

I mentioned previously the shift from single premium EOB policies to recurring premium EOB policies. The availability of recurring premiums has opened the market to younger and less affluent buyers. Unfortunately, we don’t have data to demonstrate those trends.

In order to sweeten the death benefit and LTCI benefit value propositions, EOB policies have reduced their “money-back” guarantees. Whereas consumers were previously guaranteed that they could get their money back at any time, now many policies are sold with cash values equal to 80 percent of premiums paid.

A third evolution for EOB policies has been that they are now more often sold with CBIO than in the past, as they are seen as an alternative to stand-alone LTCI, but that trend might temper as the price for CBIO might increase for new sales.

With CBIO seemingly more common on linked-benefit products than in the past, and fewer CBIO sales on stand-alone policies than in the past, and with shorter benefit periods being more common on stand-alone policies than in the past, the total amount of new LTCI risk transfer seems to be shifting toward linked-benefit policies.

ADB and linked-benefit policies are also extending into the work-site market, with some linked-benefit policies on a Section 101(g) chassis. Guaranteed-issue stand-alone LTCI has disappeared but guaranteed-issue coverage is available with work-site linked-benefit products.

For younger-age employees, combination products have greater appeal than stand-alone LTCI because life insurance is important to their young families. At those younger ages the cost of ADB and EOB is reduced because the premium-paying period is long and because a lot of coverages will no longer be inforce when the young employee reaches 80 or more years old.

A potential concern in the work-site market is that buyers (especially young buyers) might think they have more LTC protection than will be the case when they need care. The lack of CBIO, possibly exacerbated by a small death benefit, may limit ultimate purchasing power for LTC services.

As the work-site market for combination products grows, if work-site policies are included in the data we’ll see more sales at younger ages and more recurring premium.

Other than in the work-site, underwriting seems to be narrowing between stand-alone LTCI and linked-benefit policies. However, linked-benefit policies are more likely to be underwritten on an “accept-reject” basis with fewer attending physician reports. “Accept-reject” underwriting generally allows a few more policies to be issued, but sometimes a deeper underwriting dive allows a policy to be issued that wouldn’t pass “accept-reject” analysis. Because of the limited risk in ADB-only policies, LTC underwriting is less important for them.

Combination policies are less likely than stand-alone policies to limit benefits to the cost of actual LTC expenses. Not only is such a “cash” or “indemnity” policy more attractive, but it is also easier to explain, which is important in the work-site.

Generally, the public is more confident of premium stability in the linked-benefit product. However, the large price increases on older inforce stand-alone LTCI policies have led to pricing and regulatory changes which greatly reduce the risk of large price increases on stand-alone LTCI policies issued today.

A new development in 2019 is that at least two EOB policies now have separate premiums for the ADB portion of the LTCI benefit as well as for the EOB and CBIO portions. The result is that all three of those premiums (ADB, EOB and CBIO) can be tax-favored as LTCI for Section 7702(b)-type policies. Without a CBIO feature, the portion of the entire policy premium which is tax-deductible may be in the 18 percent to 20 percent range for men and the 25 percent to 33 percent range for women. When CBIO is added, the tax-deductible percentage of premium can increase to 43 percent to 57 percent for males and 58 percent to 66 percent for females.

Other recent innovations include:

- Marketing a stand-alone LTCI policy with a return of premium benefit option and cash value option to compete against linked-benefit products.

- Designing a linked-benefit product with a seven-year LTCI benefit period where the death benefit gets spread over two years. At least most (if not all) previous seven-year benefit periods had death benefits spread over three years, which required 50 percent more death benefit to get the same monthly LTCI benefit. The new design provides more LTCI benefit but less death benefit for the same premium.

- New approaches exist to help clients decide whether to purchase stand-alone or linked-benefit products, but that discussion is beyond the scope of this article.

- The ability to do §1035 exchanges and/or to use qualified assets to fund LTC insurance has increased. From my perspective, this is a market which financial advisors have barely scraped. There are wonderful things they can do for clients who have large gains in life insurance contracts or annuities.

Going forward:

- The pricing and underwriting differences cited herein seem likely to narrow.

- Conversion to Principles-Based Reserves and a new mortality table may increase the cost of linked-benefit products.

- If/when interest rates rise, new combination products may have stronger LTCI benefits.

- Increasing interest rates and Principles-Based Reserves might also result in fewer linked-benefit policies being fully guaranteed than is the case today.

- §1035 transfers from non-qualified annuities open the possibility for gains to never be taxed. Gary Forman, SVP of Long Term Care Associates, suggested that the Federal government might decide to provide a tax incentive to use qualified funds to purchase LTC protection.

- Viatical settlements (of existing life insurance policies which lack ADBs) seem to be increasingly used to pay for LTC. Might those insurers start competing with the viaticals to avoid policy surrender? It wouldn’t hurt to ask an insurer without an ADB whether they would be willing to negotiate.

- A new Shoppers’ Guide was adopted by the NAIC in April and is available at https://www.naic.org/prod_serv/LTC-LP-19.pdf. It discusses combination products much more than its predecessor. I was involved in designing the new Shoppers’ Guide and respect the attention the regulators paid to these issues and their interest in learning what the industry thinks of the new Shoppers’ Guide and how the industry uses the guide (any differently than the previous one?). I would be happy to be a conduit for any comments readers might have (claude.thau@gmail.com).

Terminology has also evolved

The insurance industry has used many names to describe these types of policies, but wording is consolidating and may consolidate more.

“Linked-benefit” is used by LIMRA and herein solely for products which might pay LTC benefits greater than the death benefit (i.e., an extension of benefits is available), regardless of whether the EOB is purchased or not. One advantage of this nomenclature is that “linked-benefit” is unique, which reduces confusion. Another is that it distinguishes from products which offer only ADB.

“Combination” (or “combo”) is used by LIMRA and herein to include both ADB policies and EOB (“linked-benefit”) policies. One way to remember the terminology is to think of “Combo” totals as “combining” ADB and EOB.

“Hybrid” has been used a lot in the industry but is often associated with cars today. To avoid confusion, it is preferable that we avoid using different terms for the same feature.

“Asset-based” or “Savings-based” is relevant when clients are moving assets to purchase a single premium combination product. With the great expansion of recurring-premium linked-benefit sales, these terms seem less relevant.

Reference:

- 2019 Milliman Long Term Care Insurance Survey, Broker World magazine, July 2019, page 30.