Variable universal life sales have declined at the start of 2023 to the tune of about 15 percent off the previous year. This can be expected as equity markets have turned volatile and a gradual increase in interest rates has made other products more appealing. Whole life, term, and IUL have seen marked increases, and the rush to sell IUL before the new actuarial guidelines were implemented in May was a big factor for IUL in the short term this year. The VUL market has continued to innovate, giving agents and customers increased flexibility and I suspect we would have seen a larger drop in VUL sales without these enhancements. As an example of this, many VUL carriers have integrated IUL sub-account options within the VUL chassis, allowing upside potential with downside risk protection. VUL is now a great alternative sale to IUL, which it had never been before, offering similar options with arguably more flexibility for customers. Other VUL carriers have created buffer strategies like what we have seen in the registered indexed-linked annuity or RILA marketplace. There has even been a new product launch into the fee-based VUL market, with the introduction of a new product geared towards the growing RIA market. All these aspects make VUL more attractive to a wider audience of financial professionals than before. Underwriting and processing times have also vastly improved for many carriers across the board, with one carrier offering a VUL product specifically geared towards efficiency and ease of issue, hoping to entice reps and advisors who normally shy away from insurance sales.

Let’s start with the innovation of RILA-like buffered strategies within VUL. Those in the industry refer to them as “buffer” strategies because they typically offer options that provide a certain percentage of market downside protection over a determined period. The client takes on calculated risk to the downside in exchange for more upside potential than they would get with traditional EIA/FIA or indexed strategies. The RILA segment has been the fastest-growing segment of the annuity marketplace with north of $10 billion in quarterly sales. Carriers such as Brighthouse, Lincoln, and Athene all have top RILA products. Due to the possibility of loss tied to the markets, this product is a registered product and agents are required to have a FINRA securities license to sell it, like VUL. Given the success of the RILA market, it is a natural evolution for these options to migrate into VUL products.

There are two carriers in the VUL space with these types of solutions: Prudential and Equitable. Prudential’s FlexGuard IVUL bridges the gap between the indexed and variable worlds, and they took it upon themselves to give this new product category a name: Indexed Variable Universal Life, or IVUL. There have been and will continue to be VUL products with traditional IUL sub-account options within them, which FlexGuard also has, but FlexGuard is a dedicated product with a focus on buffered strategies like what we see in RILA products. Equitable needs credit for the first “buffer-like” VUL option to market with their Market Stabilizer Option (MSO) years ago and they have made enhancements to it with their new MSO II option across their VUL products. So unlike Prudential that has created a separate product for this, Equitable has this available across their VUL products as a sub-account option among their robust traditional investment lineup. Given the current market volatility, FlexGuard IVUL or Equitable MSO II gives agents and consumers another tool to protect, or at least limit their downside risk. For added peace of mind, the FlexGuard product offers a range of no-lapse guarantees that can be ratcheted up from a standard five-year guarantee to an age 90 or age 120 guarantee with two available riders.

The real value of these strategies is controlling volatility. Why would one need or want to control volatility? Is it to minimize sequence of return risk for income withdrawals or fees? That could certainly be and makes sense. I would argue the major benefit to controlling volatility is to manage client expectations and protect them from their own emotions. Big swings in the market create emotional reactions that can potentially lead to financially damaging choices being made by customers. Significantly negative markets will impact cash values, especially as COI and other product fees are being charged, creating a double whammy. The buffer options allow a financial professional to frame client expectations with more certainty. Not to mention they still have the option to allocate portions of the cash value to traditional investment or fixed options depending on the situation. The value of this is hard to quantify, but ask any financial professional and they will say managing client expectations and emotions is their priority and the hardest part of their job.

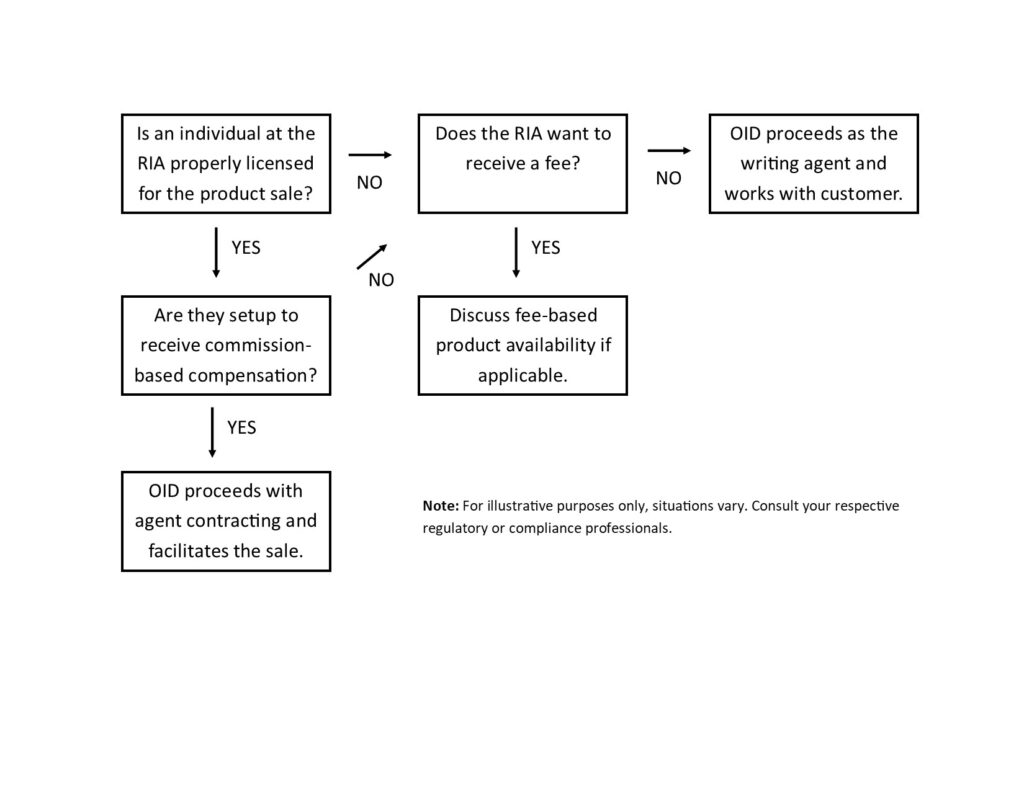

The VUL market has also attempted to appeal to two different types of markets, with two innovative products as of late. One being the growing RIA marketplace with an advisory VUL and another being the long list of financial professionals that don’t traditionally sell life insurance for a variety of reasons. The RIA market has grown by leaps and bounds with currently approximately 35,000 RIAs registered nationally, and over 14,000 registered with the SEC meaning they have over $100 million in assets under management. Nationwide has entered this market, previously only occupied by Ameritas and TIAA, with the launch of their Advisory VUL product to appeal to RIAs. It is a great option for investment advisors to receive a fee for managing the underlying investments along the lines of what they would normally charge for managing other types of accounts. They can write it themselves if properly licensed or utilize an outsourced insurance department (OID) from a BGA or IMO to serve as the writing agent. For those reps and advisors that don’t normally sell life insurance, Lincoln has launched a product called LifeGoals VUL that streamlines the underwriting and application process to a matter of hours, has no surrender charges with a single underwriting class, and features automated income along with a powerful overloan protection feature triggered when the client starts taking distributions. It is the traditional overfunded VUL design built for tax-favored growth and income distribution. The product features an asset-based compensation package of 60 basis points and is as close to “dropping a ticket” that the insurance industry has gotten to make it as transactional and simple as it can. The biggest challenge to the success of both products lies in the distribution model. How will these advisors hear of these solutions and what group will take this on for mass-market advisor education and implementation? Perhaps the responsibility lies with those BGAs and IMOs that have developed outsourced insurance departments (OIDs) to market to advisors. Or will another, more wholesale-orientated group or FinTech company take it on that perhaps sits outside the normal BGA model? Maybe it will turn carrier-direct for distribution like variable annuities. It is hard to say, and time will tell if either product finds significant traction.

With the enhancements we have seen in the VUL space, it is my opinion that VUL now provides some of the most flexible, enhanced options for customers and agents we have ever seen from both an accumulation and protection design viewpoint. With the continued stress that the IUL market has weathered from multiple efforts to curb dishonest illustration tactics, one would think it is only a matter of time, and perhaps lawsuits, for that market to merge into VUL under the fold of the registered product realm. The biggest barrier to entry for agents to offer VUL is obtaining securities licensing and being subject to broker-dealer oversight, which many will resist for as long as humanly possible. Regardless, VUL is going to continue to evolve to become even more attractive, more versatile to a point where it will be very difficult from an opportunity cost perspective to ignore.