Annuities have had three consecutive years of record-breaking sales throughout the country. Consumers are purchasing annuities like crazy… The annuity business is now almost a half a trillion dollar a year business! For consumers that are in the retirement red zone–as in 5 to 10 years before and after retirement–and cannot afford to lose their money due to the stock market but want more upside potential than things like CDs, annuities may be for them. Furthermore, for consumers that want to replicate the guaranteed lifetime income that their beloved pension plans and Social Security provides them, annuities may be for them.

However, even after these huge years for annuities and the fact that consumers that bought annuities are generally happy with them, there are often fear tactics that advisors will communicate to clients when it comes to annuities. The amount of harm done to consumers’ retirement readiness as a result of misinformed “advisors” stating that annuities are bad is beyond measure. There are a few reasons that you have a large group of advisors that will tell their clients that annuities are bad.

- Lack of understanding: Many times, the advisor will cite two different things to the consumers to state that annuities are bad. The first is “high fees.” These advisors once upon a time witnessed variable annuities that did indeed have extremely high fees. Twenty years ago, for example, it was not uncommon to find a variable annuity with total fees of 3% to 4 1/2%, which is crazy. However, the world has changed! Variable annuities are now just a minority share of the total annuity business. Now, many annuities have little to no fees. But again, these advisors fail to understand this because they have been living two decades in the past and they have failed to keep up with an extremely fast evolving industry.

Another area of the “misunderstanding” is where the advisor will tell the client that he/she “will lose all control of their money” once they start taking income payments. This is a common fear tactic and again, a result of the advisor living decades in the past. Once upon a time, the only way to get guaranteed lifetime income from an annuity was to “annuitize” the annuity value. This did indeed mean that the control of the money was essentially forfeited. It also meant that the death benefit to the beneficiaries could be limited, or nothing! However, times have changed, and the most prominent way that annuities generate guaranteed lifetime income today is through something called “Guaranteed Lifetime Withdrawal Benefits,” which is very much different than “annuitization.” For instance, with the guaranteed lifetime withdrawal benefits, the consumer is not forfeiting all their control. If they choose to stop the payments, they can. If they choose to cash out the annuity, they can. (Note: There can be surrender charges depending on the year he/she cashes out the annuity.) Also, with these benefits, if a consumer has triggered their lifetime income and only taken one payment, for example, but dies after only one income payment, the beneficiary gets the balance of their accumulation value! It is not like the company “keeps all of their money” if they die, which again is a common misconception.

- Gaslighting: For every one advisor that doesn’t understand annuities as I discussed above, there is an advisor that does understand annuities but will still cite the reasons above to stay away from annuities. Why would the advisor be disingenuous like this? Because advisors generally get paid on the assets that they manage. For example, there is one large company that almost invariably charges 1.35% on “assets under management.” Paradoxically, this is actually a remarkably high fee compared to the national average, but I digress. That means that if a consumer has $1 million with that company, then that advisor will be charging $13,500 every year. If you were to move $500,000 out of that company into an annuity, they would lose $6,750 per year. Naturally, these advisors do not like it when money leaves from under their umbrella!

- Rosy stock market numbers: Advisors will often cite that because they have a secret formula for the clients that will grow their portfolio by X percent, then by moving money into an annuity the consumer will be missing out on the opportunity for that huge growth. In economics we call this “opportunity cost.” That is, the lost opportunity by moving your money into an annuity in our example. Again, citing 10%, 12%, etc. returns is a tactic often used when the advisor does not want to lose the assets under management. Now, it is undeniable that the United States stock market has done well over the long run. Over the last 100 years large company stocks have averaged about 10% annually. However, you cannot apply that same “100 year” performance to your portfolio if you are in that “retirement red zone.” You don’t have 100 years! Over the long run, the market may do X, but over the short run it can do anything. Also, “averages” don’t matter when you are taking withdrawals because of sequence of returns risk!

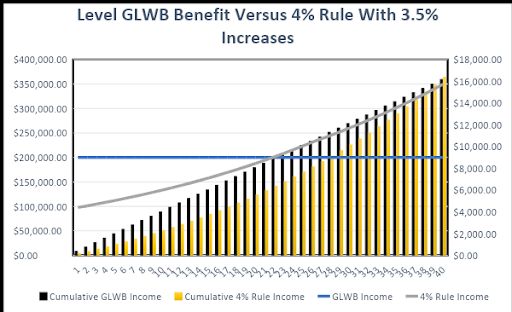

Furthermore, and most importantly, let’s play the advisor’s game and assume a rosy stock market. Even assuming a rosy stock market (to a certain extent), the income generated from an annuity oftentimes will eclipse the stock market alternative. When you plug an annuity with a guaranteed lifetime income stream into the same software that the advisors use to model your portfolio performance, you’ll find that many times the annuity enhances the amount of income that the consumer can take in retirement years. Again, even if we did assume that the stock market was going to perform excellent! How is this? Because the guaranteed annuity payments are so high that they oftentimes cannot be replicated by the stock market unless one assumes outrageous stock market performance.

How do I model out what I just said in the previous paragraph? By using “Monte Carlo simulations,” which is the same software that your advisor uses when he explains to you how by keeping your money in stocks and bonds that he will be able to generate X amount of income during your retirement years. If the advisor took the time or had the knowledge to incorporate an annuity into that same analysis, that advisor would be sold on annuities. But alas, annuities won’t provide him/her (the advisor) with a perpetual 1.35% income stream.

To sum this section up, be leery anytime an advisor says they can outperform what an annuity can do, especially if they are throwing out long-term “averages” on the stock market! And remember, by using the same Monte Carlo analysis that the “advisor” uses, we are often able to demonstrate how there is additional wealth that is generated by incorporating an annuity.

I will often hear from a client that there is another advisor throwing shade on my annuity idea. I take this personally. Not because I “need” to sell an annuity. I am at the stage in my career where any one sale will not change my life. I take it personally because the amount of harm done to consumers by being told that annuities are bad is beyond what we can measure. This is not good for our industry and most importantly, not good for retirees!

So, I will often volunteer for a three-way call with that advisor and the client. Facts, math, science, and numbers that I use are difficult to argue against! And my math science and numbers are widely accepted. Monte Carlo for instance. I know that once I get on a call with that “anti-annuity” advisor, there is no way that client will be led astray by that advisor who is desperate to not lose the assets. By the end of the call, 95% of the time the advisor concedes that the annuity scenario is a good strategy. I am not saying that annuities are for everybody or for 95% of the population. I am just saying that if I recommend one to a client, there are the facts, math, science, and numbers that indicate that for that specific client, annuities would benefit them.

Again, facts, math, science, and numbers do not lie and there is an exceptionally good chance that that advisor does not know the facts, math, science, and numbers like I do. Hence, his/her naivety around annuities. The advisor is entitled to their own opinions, but not their own facts, math, science, and numbers.

")