I recently saw somebody write about how we should not compare annuities to the four percent rule. Although I agree that there needs to be additional disclosures and education in the annuity part of the conversation, I disagree with not comparing the two.

Re-Anchor Clients in Reality, Not Fairy Dust

I believe that consumers tend to “anchor” their retirement income expectations on the wrong thing and therefore should be “re-anchored” in reality. For instance, consumers should be educated on the fact that William Bengen’s study in 1994 showed that in order to sustain a stock/bond retirement portfolio for 30+ years in retirement, the consumer should take out no more than four percent of their retirement account balance that first year in retirement, adjusted each year thereafter for inflation. Consumers should also be aware of the new updated studies that show “rules of thumb” of 2.3 to 2.8 percent. (Note: When using these comparisons versus annuities, it is important to discuss that annuities generally do not have “inflation adjustments” the four percent rule incorporates. More on that in a bit.)

This “re-anchoring” is important because many consumers know that the S&P 500 has gone up double digits on average for the last century and therefore overestimate what withdrawal rate they should utilize. They have seen the glorification of the stock and bond markets and have likely seen the mountain charts like the Ibbotson SBBI Chart. You know what charts I am referring to; those that show that the stock market has done double digit returns forever and that their $1 invested back when Adam met Eve would be worth enough to purchase their own private island today.

Thus, if a consumer has in their brain that stocks and bonds have always performed seven percent, eight percent, 10 percent, 12 percent, then they will tend to believe that their retirement withdrawal rate is beyond the four percent that the research shows. Even if a consumer has heard of the four percent withdrawal rule, they may have not had the math laid out for them yet that is specific to their situation. It is important to explain to those that love their stocks and bonds—as I do—that even though the S&P 500 could average 10 percent over the coming years, it does not mean they will not run out of money by taking only four percent of the retirement value from their stock and bond portfolios! How is this possible? Because of the sequence of returns risk that the stock portion can subject the client to and the low interest rates (still) that affect the bond portion. And because of these two risks a client should not overestimate what their portfolios can do as far as withdrawal rates. If you would like a graphic that helps you explain the sequence of returns risk to your clients, email me.

To demonstrate my points in the previous paragraphs, I want to cite a study by Charles Schwab. In their 2020 Modern Retirement Survey they asked 2,000 higher net worth pre-retirees and newly-retired retirees about how much money they had saved for retirement and also how much money they expected to take from their retirement portfolios. The answers from the participants were that they had $920,400 in retirement savings on average, that they planned on spending $135,100 per year from those portfolios on average, and that they were generally confident in those dollar amounts allowing them to live the retirement they would like.

I would argue that a 14.68 percent withdrawal rate ($135,100 divided By $920,400) defies any retirement research I have seen! Naturally, Schwab then points out that—contrary to these participants’ beliefs—a $920k portfolio will run out in only seven years (obviously not including interest/appreciation). Clearly, these consumers should have the math explained to them. Even if the consumers understand the new rules of thumb, they may be experiencing cognitive dissonance that should be addressed by the financial professional. By doing so, you will “re-anchor” their expectations to the new realities of 2.3 percent, 2.8 percent, or four percent withdrawal rates, which will set you up for the annuity conversation that we’ll discuss.

I am not suggesting an agent go into a big dissertation on these individual studies. I just believe that going over the simplified math—specific to the client’s portfolios—based on these new rules of thumb should be done in order to show the power of annuity GLWBs. Although generous, using the old four percent rule of thumb will suffice in explaining the annuity value proposition. By demonstrating this math to the clients, you will be re-anchoring their expectations to realistic numbers. And only then do I believe they will realize the true power of GLWB Riders.

The GLWB Conversation

Here is what my conversation looks like that I will walk our hypothetical client through:

Let’s say our 63-year-old has $100,000 in a stock and bond portfolio. I start by discussing how this 63-year-old may have the expectation that her $100k grows by five percent or so per year between now and retirement in two years. Well, based on her $110,000 (not including compounding) value at that point, what withdrawal should she take in her first year of retirement? This is where I discuss the four percent withdrawal rule, which usually surprises them because their anchoring is off. I also discuss the reasons for the withdrawal rate being only four percent. But then I will show her $100k growing to $110k in two years at retirement. If the client wants us to assume a 20 percent return over two years, fine! I will do that instead. The math still works.

By the end of the two years, her $100k has grown to $110k. That is when we figure the first-year withdrawal, which comes out to $4,400. Again, that $4,400 is supposed to increase with inflation, per the four percent rule.

That $4,400 is assuming everything goes correctly. That is, that she gets 10 percent appreciation between now and age 65, and also the four percent being indeed sustainable over her 30-year retirement.

That is when I will switch to the annuity. On one of the industry’s top annuities/GLWB riders right now, her $100,000 will generate a $7,800 payment starting two years from now, guaranteed. That payment will go on forever. This GLWB payment is 77 percent higher than what our four percent withdrawal rule will provide. And you don’t have the “hoping and praying” with the annuity. Usually at this point in the discussion, the responses are in three different areas:

- Seems too good to be true! How can the company do that? (This is a topic for another article.)

- What if everybody lives forever? Will the company go out of business? (Again, a topic for another article.)

- But what about inflation? The four percent rule includes inflation, and the annuity does not.

Let’s discuss.

Level Annuity Payment Versus Four Percent with Inflation

Although I believe we are being generous to the situation by using the four percent rule instead of the more updated and lower rules of thumb, it would be disingenuous to not explain the lack of inflation on the level payout GLWBs. (Note: There are some GLWBs that have increasing income, but let’s leave the conversation to level income for now.)

This objection about annuities not having inflation included, versus the four percent rule, is a reasonable objection as inflation adjustments can be crucial. As a matter of fact, the “inflation rule of 72” says that a 3.5 percent inflation rate—for example—will chop the purchasing power of a dollar in half in only 20.5 years (72/3.5=20.5 years). Meaning that $7,800 would only have the purchasing power of $3,900 in 20.5 years assuming 3.5 percent inflation.

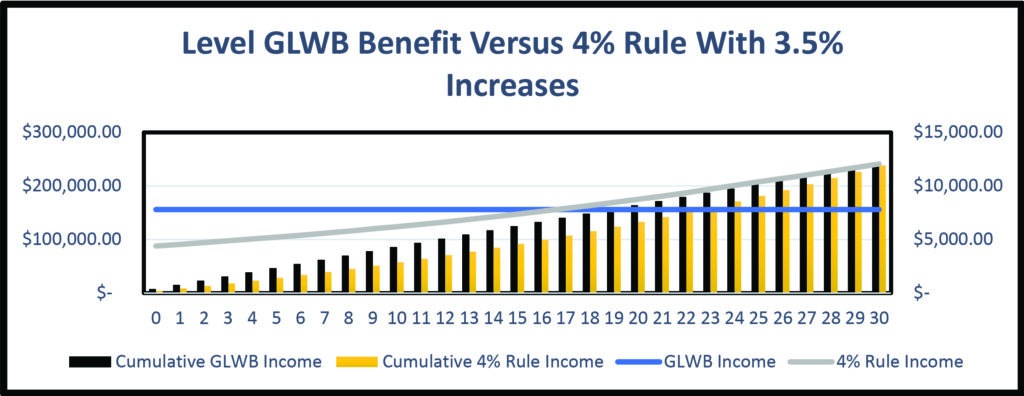

So then what provides the highest cumulative income, our GLWB or the four percent rule example? Above is a graph from a spreadsheet I created to show what provides more income—the $7,800 (GLWB) without inflation adjustments or the $4,400 (four percent rule) with inflation adjustments. (Note: For the inflation adjustments, I assumed 3.5 percent.)

As you can see above, the inflation adjusted four percent rule annual income crosses over to where it is more than the $7,800 in the 18th year. You can see the two lines crossing over. The dollar amounts represented by the lines are in the right axis.

More important however is, what is the cumulative income from each strategy over a period of 30 years? That is represented by the bars and the left axis labels. As you can see, the Cumulative GLWB Income (black bar) stays higher than our cumulative four percent rule all the way through the 30-year retirement. Furthermore, this does not incorporate “time value of money” of the amount of excess GLWB payments we got above and beyond the four percent rule. Technically, those excess dollars reinvested would equate to even more than what our “cumulative” black bar is showing.

Clearly, there are other scenarios that we could run that can benefit or degrade the story on either one of the two solutions. For instance, we could run the four percent rule assuming a much higher return than 10 percent over two years—for example 20 percent. In that case, the “cumulative withdrawals” on the four percent rule overtake the annuity in the 27th year. But then we could also apply the “time value of money” to the excess annuity payments. We could also use the 2.8 percent withdrawal rule. Or, one could add different inflation rates, etc.

In the end and with all of this said, the story should be that consumers need to anchor their expectations reasonably and also that annuities have a great place in many consumers’ portfolios with or without inflation.