I have a lot of people asking me about LTCI solutions, but they tell me it sounds too expensive. What can I do to help them get a plan that meets both their needs and their budget? —Affordable in Arkansas

Dear Affordable,

Most long term care agents will answer this way: “If you think LTCI is too expensive, you should see the cost of not having LTCI!” Then the agent will show the prospect the cost of care in their area, and the costs might be truly scary. In fact, so scary that the prospect runs away without a plan!

This is the traditional needs analysis. Needs analysis is an important part of long term care planning, but it may not always be best to discuss at the beginning of the conversation. Admittedly, this can work for skilled agents with certain prospects who see LTCI as a luxury. However, far too often, it results in the prospect deciding not to purchase a LTCI plan once they see the price tag.

Closely related to needs analysis is the defined benefits approach. Agents commonly select pre-determined benefits and ask for one-size-fits-all quotes. This approach also frequently results in clients passing up coverage altogether.

Many agents tell me they despise it when their prospects demand quotes early on in the conversation before they have assessed needs and considered benefits. Here is an alternative approach. Agree with your prospect and embrace these questions! These questions can be a door opener to show how affordable LTCI can be, to ask about funding sources, and allow you to share insurance tax advantages.

This conversation often leads to funding analysis. The idea is to first help your client identify which assets or income are ideal for them to use to pay for insurance protection. This can establish an initial target price point, payment period option (single pay, multi-pay, or lifetime-pay), and can be useful to identify funding sources with tax advantages. Funding analysis can be effective as evidenced by life insurance plans with long term care riders that commonly use an asset-based funding source to great success. You can use funding analysis for any insurance plan.

The funding analysis may be so effective that later in the conversation, when cost of care is discussed, you will find your client asking to buy more coverage. At this stage they better understand the value proposition of the insurance plan.

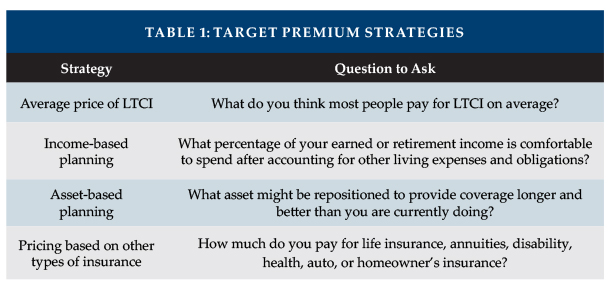

Closely related to funding analysis is the defined contribution or target premium approach. This is a method where you determine how much money will be put into the plan and choose the plan that maximizes benefits based on a price target.

An example of this strategy is to start with a percentage of income that will be used to fund the insurance plan. This is similar to the approach used in the 401(k) market to identify a percentage of income to take out of the paycheck for a defined contribution plan.

Many agents and websites employ a “good, better, best” methodology to allow the prospect to choose the right starting price for them. This is a combination of the defined benefits approach with three pricing options. Many prospects will choose the middle option. Often this will result in a price that most clients choose on average.

The Target Premium and Funding Approach in Practice

The importance of the funding approach hit home recently. I was having brunch with a good friend, Steve. He is a very successful 62-year-old business executive. As a life-long bachelor, he is winding down his career and contemplating his travel plans in retirement. We got to talking about my long term care business. I told him that everyone needs a long term care plan whether or not insurance is used as the solution.

Marc—“What’s your long term care plan?”

Steve—“I’ll self-insure. I’m really healthy and can’t picture needing it. The insurance companies are trying to make money off of me, and if they don’t they’ll just raise my rates.”

Did I mention that Steve is not a fan of insurance?

Marc—“You might consider buying a really small policy. There are core high-end features built into even small plans, and, when you consider the costs involved, the insurance company won’t be making much money. There are plans today where you can prepay the premiums and limit the risk of rate increases.”

Steve—“Tell me more.”

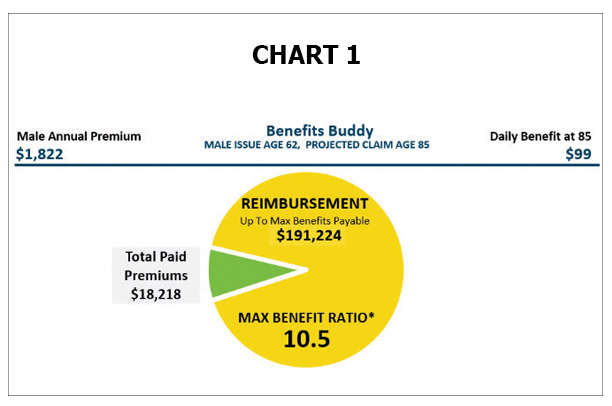

Steve’s an analytical type, so I drew up a plan to demonstrate the LTCI value proposition (Chart 1). We discussed both traditional and Hybrid alternatives. The plan he preferred most looked like this:

The plan cost only $1,822 per year and would be paid up in 10 years! At that point no more premiums would be due and the insurance company couldn’t raise his rates or reduce his benefits.

At age 85, this plan could provide just under $200,000 of benefits paid out at about $100/day should he need long term care services for several years. Not a high-end plan, but he could self-fund the rest as he planned to do anyway. This is a good foundational plan for the care he might need in the future.

The value proposition is that the insurance plan might provide a maximum of 10.5 times tax-free benefits compared to the total premiums paid, which significantly exceeded the multiple he could get from self-funding over the same horizon.

I could see the wheels turning as Steve began to assess the financial tradeoffs.

The Triple Tax Advantage of HSAs for LTCI

Steve spent most of his career as one of the country’s foremost tax experts in his field. So, we began to dig a little deeper.

Marc—“Let’s discuss some funding options for this plan. Do you own an HSA?”

Many tax experts aren’t aware that you can fund LTCI premiums using an HSA up to an annual limit. HSAs have soared in popularity because of the ACA and growth of high deductible health care plans. HSAs have grown 10-fold since 2008 with about $51 billion of assets as of 2018.1

Steve—“In fact I do have an HSA that is accumulating a lot of money.”

It can make a lot of sense to fund LTCI from an HSA. HSAs can be left to a spouse at death but otherwise generally get taxed if the remaining amount is left to the estate.

Steve was able to take his original tax-deductible contribution into the HSA, which had grown tax free, and then withdraw the money, tax free, to pay for his LTCI premiums. This so called “triple tax advantage” could be parlayed into significantly more LTCI benefits that would also be received tax free.

We discussed the cost of care in his area today and the potential cost of care in the future. For home health care the average cost might be three times higher than this plan, and facility care costs are even higher.

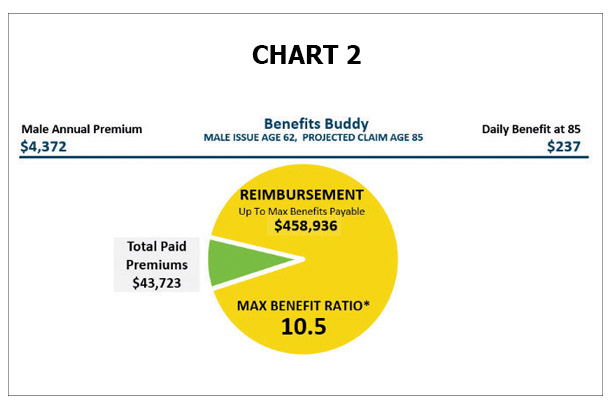

Chart 2 shows the plan that Steve finalized:

Steve decided to more than double the LTCI premium initially quoted to maximize his HSA withdrawals. He will most likely continue to fund the premiums out of his HSA over the next nine years and have a greater amount of protection than his self-funded plan alone.

If you have married clients, not only can they benefit from joint policies and spousal discounts, but they may also be able to use one spouse’s HSA to fund both of their LTCI plans!

Inside the Numbers

I researched the average stand-alone LTCI purchase price based on data from annual industry surveys. Looking at the period starting in 2004 through 2018, I realized something extraordinary. The average purchase premium hasn’t really changed in the last 15 years.2 Average industry premiums have nearly tracked inflation:

- For stand-alone LTCI, the average new policy price is about $2,500 per person.

- For life insurance hybrid plans that include long term care or chronic illness riders, the average is about $6,400 per person as a recurring premium and $91,000 as a single premium.

The Bottom Line

Many people will use LTCI solutions to partially or fully fund plans once they are convinced that it is affordable and offers value. Addressing funding and price early in the conversation can reduce fear for your client. They know what to expect and it builds more trust.

You may feel like you are helping your prospect by showing the cost of care early in the conversation, but it could be a disservice if they were to walk away without any plan at all. Once funding and price are on the table, it further helps improve the agent-client relationship. Your prospect knows that you have their best interest at heart because of a mutual objective: To help provide them the most beneficial plan possible for their budget.

Reference:

- https://www.morningstar.com/blog/2018/11/12/top-hsa-providers.html

- If this sounds counterintuitive, consider that the most common benefit purchased today is a three year benefit period with three percent compound inflation protection. 15 years ago, the most common benefit was lifetime coverage with five percent compound inflation.